High Inflation is coming

Clearly we have reach a point where everyone feels inflation is impacting their day to day life. For the past 20 years people enjoyed relatively low inflation and prices are generally stable. Going forward I think we may face a different type of inflation more similar to other periods in past history.

Where did inflation came from no longer matters but how expectation of it will increasingly strengthen its power and resolve.

Think about it, do you expect prices to increase more next year than last year? If you are property buyer do you expect property prices to come down while building cost keeps rising? If you are a business owner will you project your cost to be up or down next year and the years that follows? These expectations if left unchecked will sooner or later turn inflation into a Godzilla typed monster that will destroy economies.

So with inflation central banks hands are tied and they no longer can use monetary stimulus to support the economy. In fact the generally accepted solution to tame inflation is to raise interest rates. The impact of rising interest rates will thus have a very key impact on all financial assets.

The long government bond rate which is also known as the risk free rate is a key dictator in the pricing of financial assets. Investors demands a certain amount of trade off for taking additional risk. It is a no brainer for an investor if the risk free rate is 10% versus choosing to invest in a business that returns 10%.

Now even if you are in your 50s, you probably haven seen risk free rates anywhere near 10%. So you really have to ask yourself what is the probability of it happening. The CPF ordinary account pays 6.5% interest from 1974 – 1985.

The CPF special account a rate setting mechanism peg to the 10 year Singapore Government Bond is now at 3.7%. This is very much within touching distance of the 4% floor for the special account. The likelihood of surpassing 4% is now very real. Now let’s assume the special account pays 5% interest, an investor should no longer be happy with investing in a REIT that give a 5% yield. Maybe an 7% yield may be more appropriate.

All else been the same, REITs will need to go down in price such that it gives a 7% yield with the same payout. This can happen very quickly as interest rate can change at an instant. This can also be said of companies that investor expect higher returns such as to compensate for the higher risk free rate.

We are currently seeing the scenario playing out in the US market as expectations of further rate hike fuels Price Earnings multiple compression. This is all happening during a time where many companies earnings remain very strong. Businesses that have any slight slow down droped like a rock like Netflix, Paypal, Walmart and many more.

Currently I see the economies at a crossroad. One scenario whereby inflation can be contain fairly quickly with aggressive rate hike to normalised interest rates of 3% -5%. This would mean more pain this year but things shall stabilise going into 2023

The other scenario points to inflation runs further ahead and rates increases plays catch up. In this case interest rate could soar to 10% and we get a market crash that is somewhat like the 99 Dotcom bubble crash. Investors should thus be prepared for both cases. Historically the assets that have done well during times of inflation includes, commodities, real estate and gold. Companies with real moats and pricing power will weather the storm better.

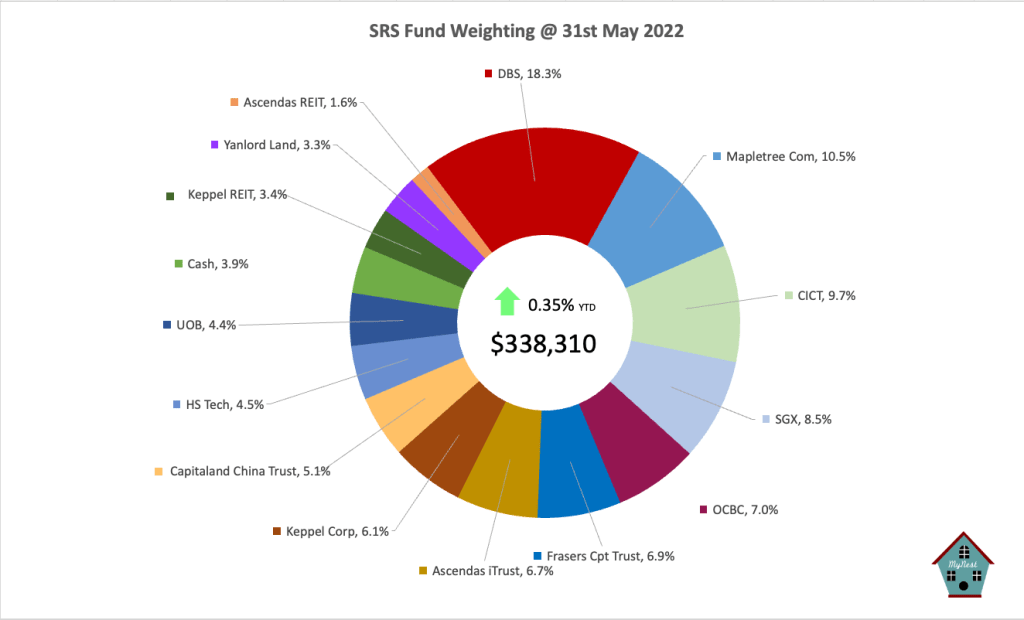

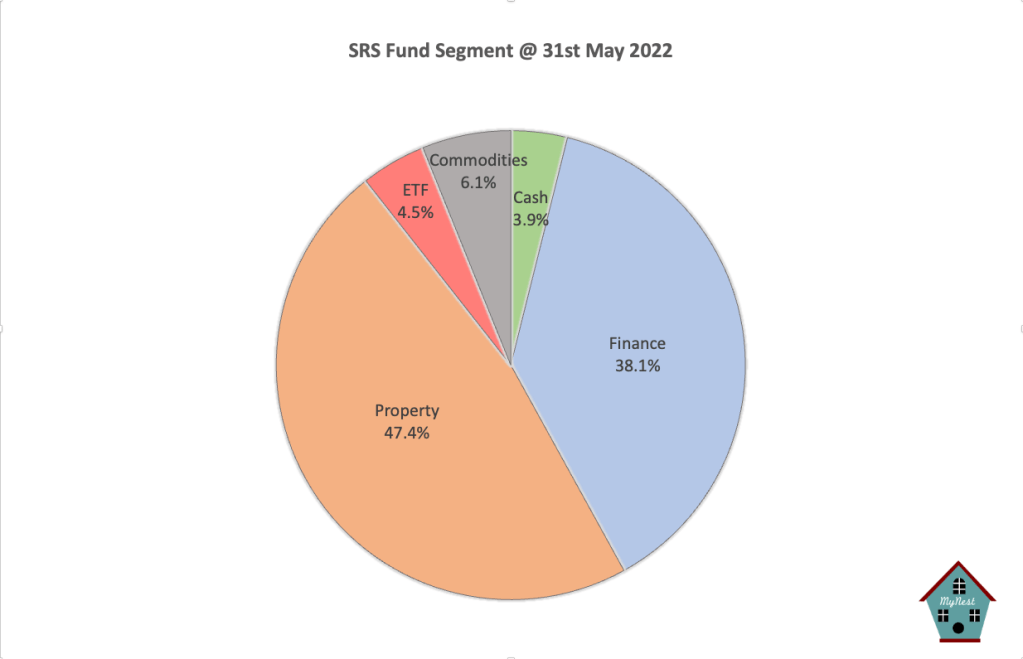

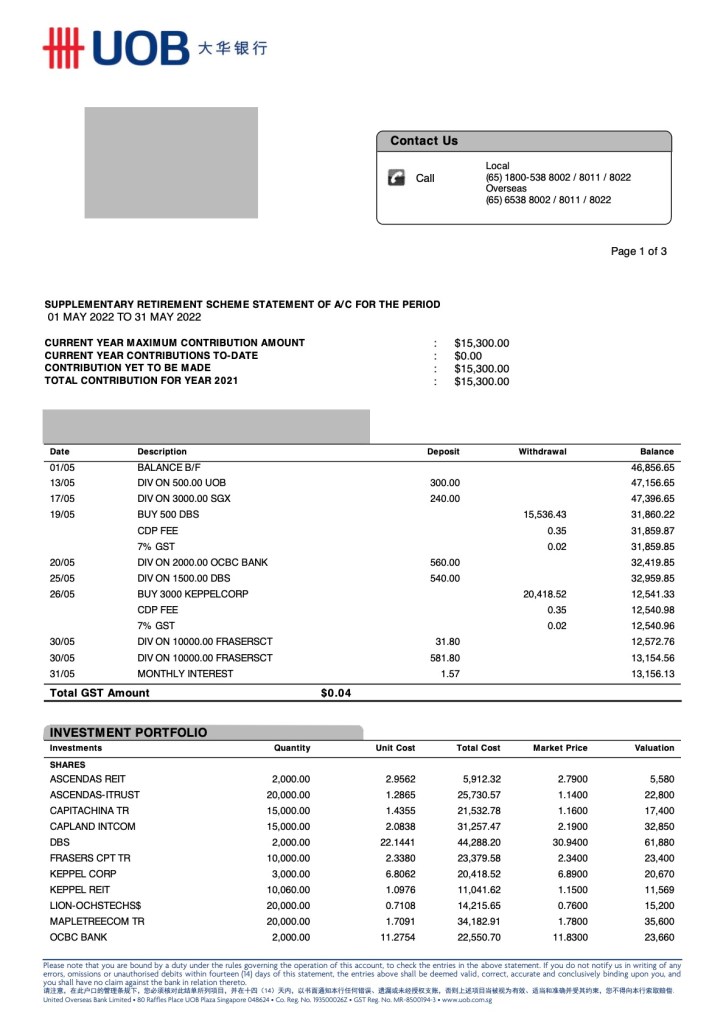

As such to position the SRS Fund for in a high inflationary environment I have begin to invest the excess cash in the fund into commodity typed play. In the month of May I have put up 6% of the fund to initiate a position in Keppel Corp which consist of an oil and gas component and a real estate component.

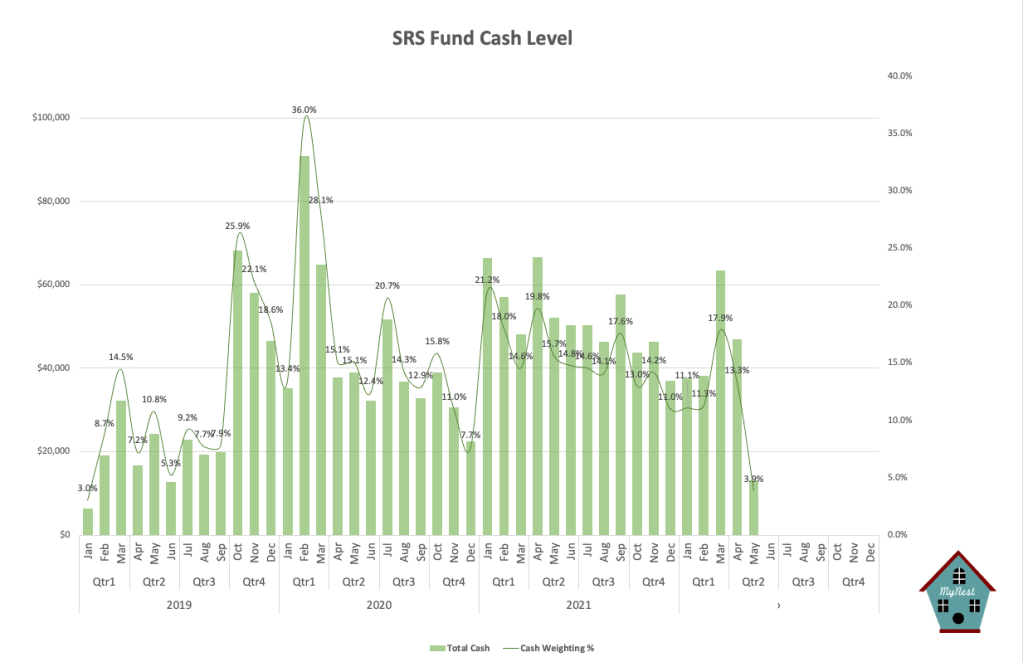

The SRS Fund remains slightly in the green year to date despite the fall in the general market in the month of May. This is mainly thanks to the dividend collected to cushion the fall in price of the many companies in the portfolio.

I am still fairly positive for the SRS fund to do well come end of the year as Singapore’s reopening and the gradual relaxation of the Chinese economy should provide some support against the strong inflationary headwind.

LATEST POSTS

-

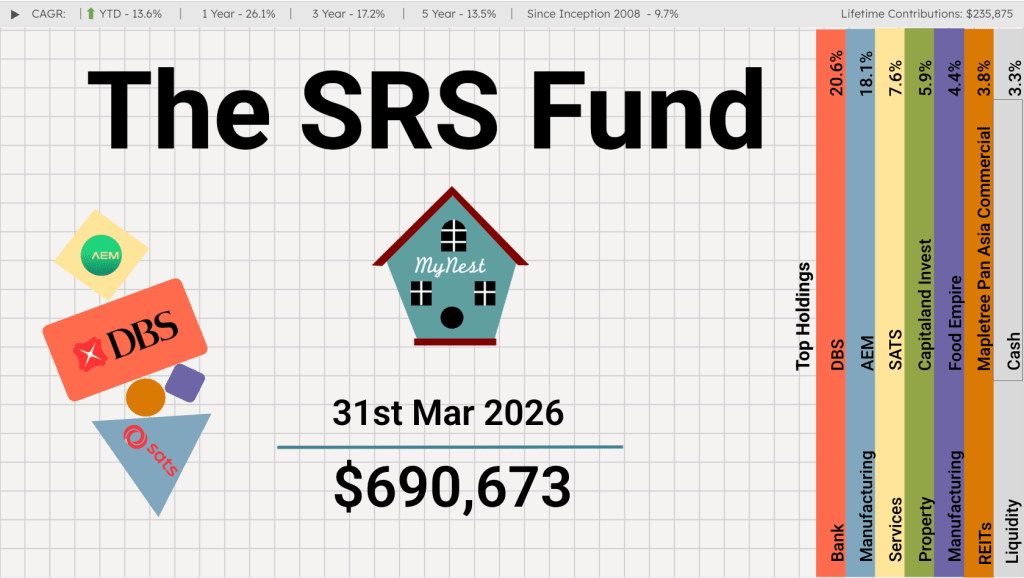

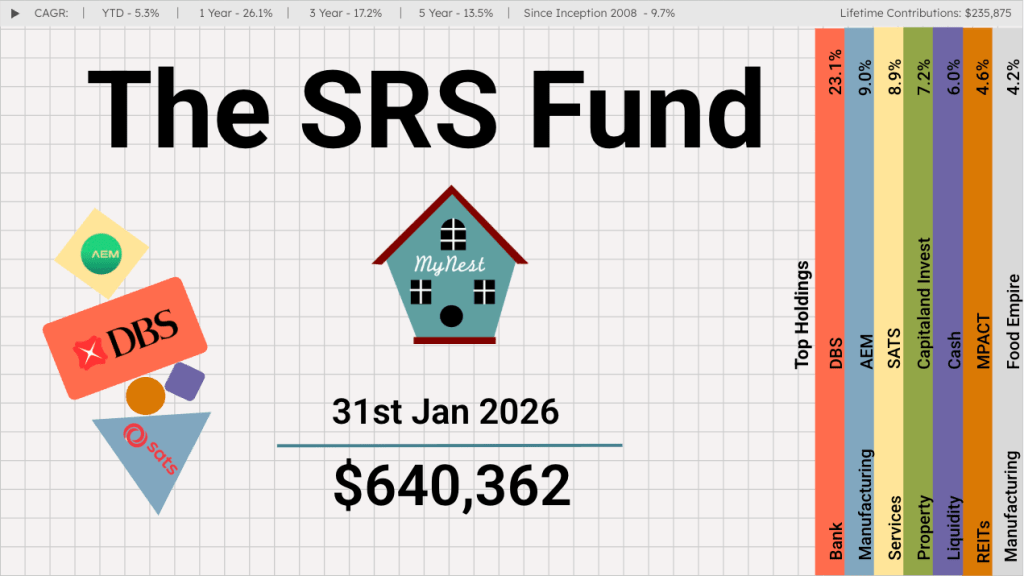

The SRS Fund Mar 2026

It is an enduring market reality that a concentrated minority of holdings drives the vast majority of returns. For years, DBS (currently the largest individual holding at 20.6%) has served as the compounding engine of the SRS Fund.

-

MyNest US Fund Mar 26

March shattered any lingering market complacency, pivoting sharply from the localized damage of the “SaaS-pocalypse” to a systemic shock driven by the war in Iran.

-

The SRS Fund Feb 2026

The Singapore Budget 2026 has set a robust backdrop for local investors. For the third consecutive year, the government is operating from a position of immense “dry powder,” with an overall fiscal surplus of $8.5 billion projected for FY2026.

-

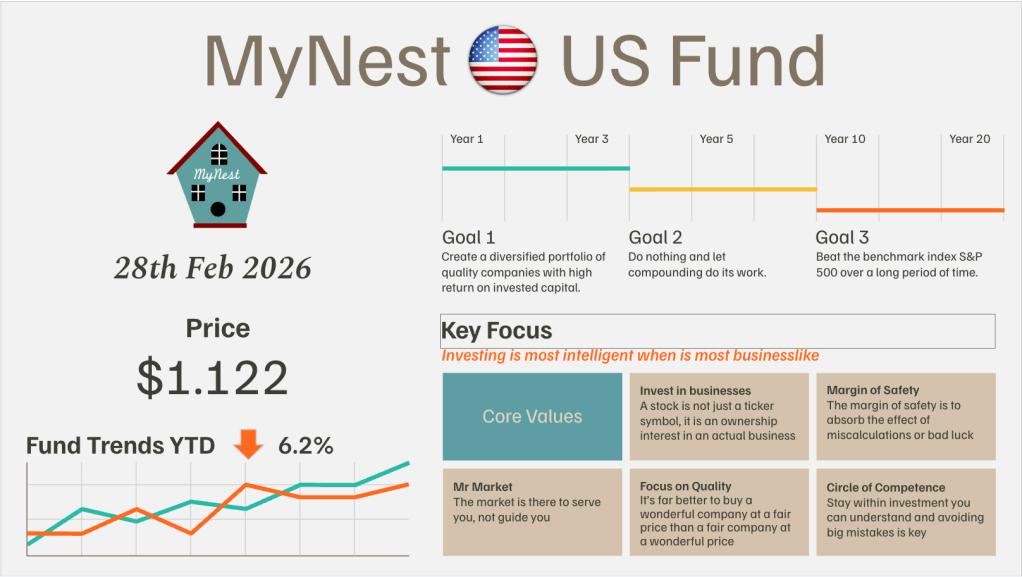

MyNest US Fund Feb 26

February 2026 proved to be one of the most challenging months for our fund since its inception. A wave of “AI anxiety” swept through the Software-as-a-Service (SaaS) sector

-

The SRS Fund Jan 2026

After a blockbuster 2025 that saw GDP growth hit a surprise 4.8%, the first month of 2026 has proven that the momentum is far from a fluke. Between record-breaking stock market performance and massive industrial investments, the “Little Red Dot” is making a very big noise.

-

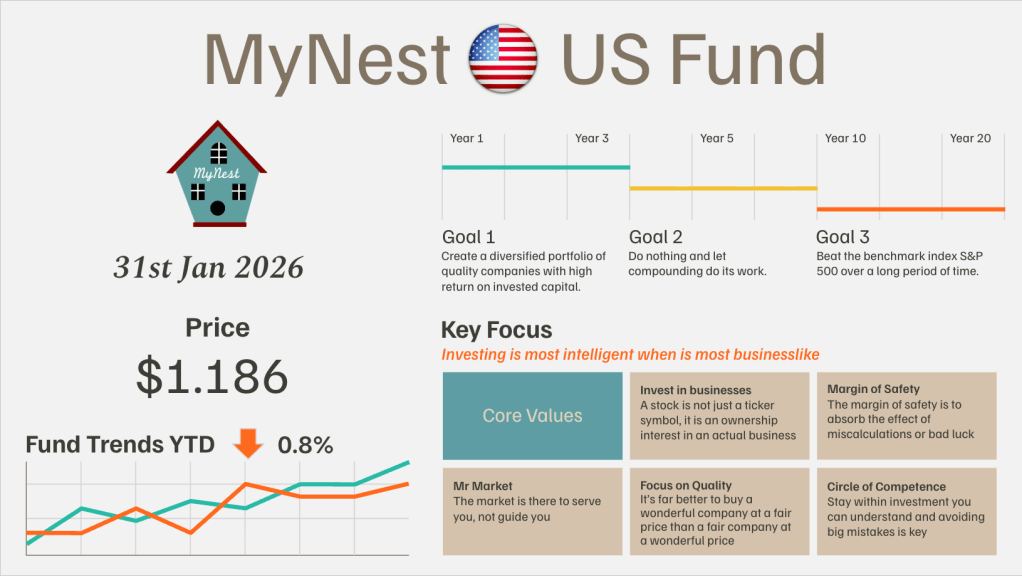

MyNest US Fund Jan 26

I have a confession to make. After reading Chip War at the end of 2022, I fully grasped the strategic importance of TSMC and ASML in the global semiconductor supply chain.