Dear Investors,

I have a confession to make.

After reading Chip War at the end of 2022, I fully grasped the strategic importance of TSMC and ASML in the global semiconductor supply chain. I recognized them as the gatekeepers of the high-end silicon required for the artificial intelligence build cycle.

However, I failed to anticipate the sheer scale of the demand that followed. As Large Language Models (LLMs) scaled, the requirement for advanced logic reached unprecedented levels. While our decision to avoid TSMC was a deliberate choice based on their intensive capital expenditure requirements, I must admit that our inaction on ASML was a case of “thumb-sucking.”

During the October 2024 earnings call, ASML management highlighted a weakened outlook for 2025. The stock subsequently plummeted from $860 to a low of $574, languishing in a range-bound slump for nearly a year. At the time, I dismissed ASML, incorrectly inferring that its customer base was too concentrated to sustain growth.

This was a failure of imagination. I operated under the narrow assumption that only GPUs required ASML’s Extreme Ultraviolet (EUV) lithography machines. I was wrong. It has become clear that High Bandwidth Memory (HBM)—the literal backbone of AI processing—has similarly stringent EUV requirements.

This lack of technical depth forced our fund onto a more difficult path as we navigate the volatility ahead. While the market continues to present opportunities, this experience is a stark reminder that “digging deeper” is not optional.

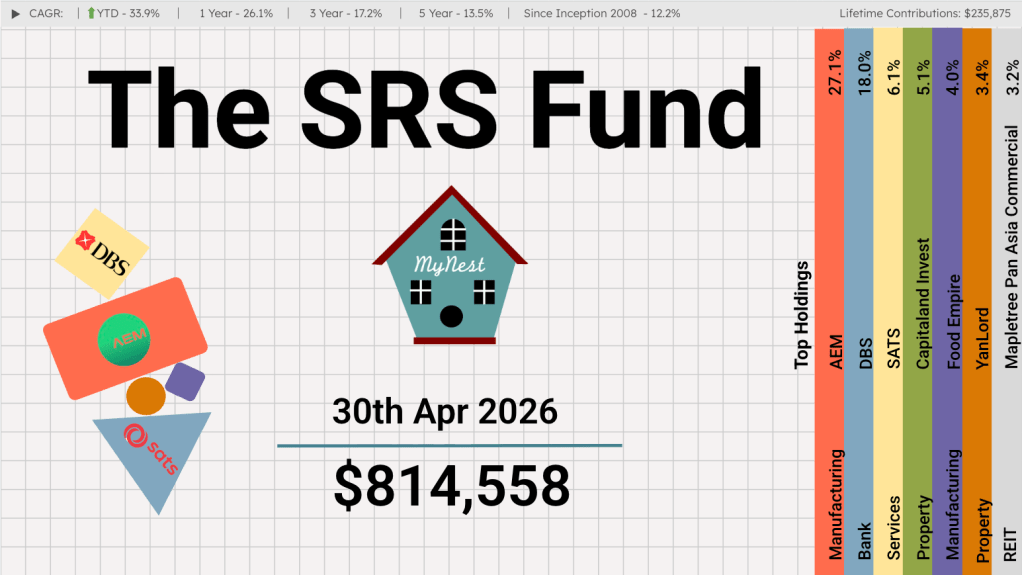

Though we missed the initial windows for ASML and subsequently Micron, I believe the SRS Fund finds its silver lining in AEM Holdings (Will discussed more on this position over at the SRS Fund post). We are positioning ourselves where we see mispriced value, hoping this “stumble” remains a lesson in diligence rather than a permanent setback.

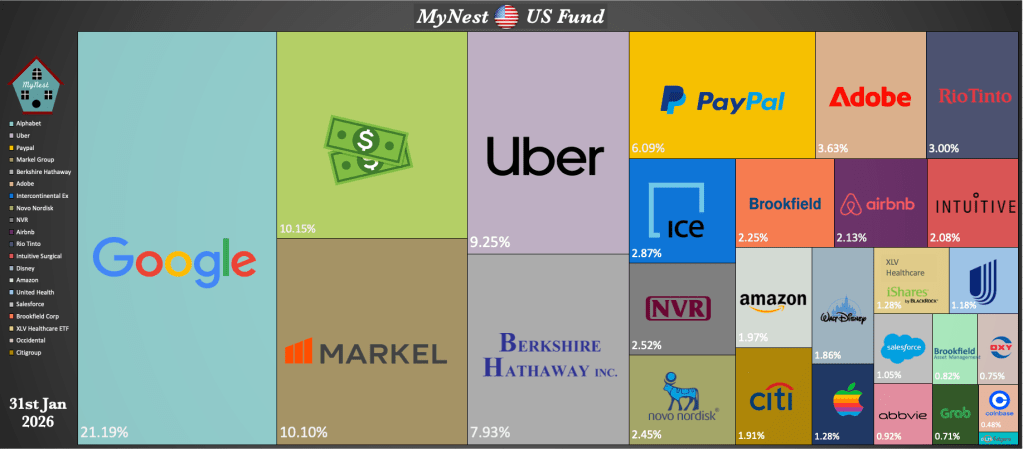

MyNest US Fund Portfolio Compositions

We added 2 new positions into MyNest US Fund and they are

- United Health (1.18%) : As part of the fund healthcare portfolio diversification, we have added this stable giant to complement Intuitive Surgical, Novo Nordisk, Abbive and Fulgent Genetics.

- Intercontinental Exchange (2.87%) : While investing into an exchange is nothing to shout about, our interest into this company is mainly on their new acquisition: Polymarket.

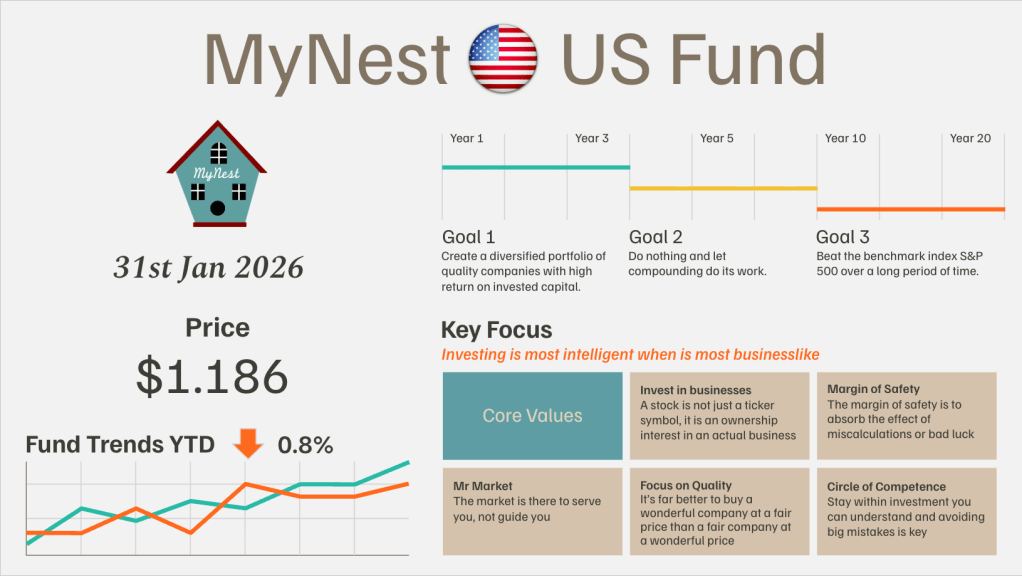

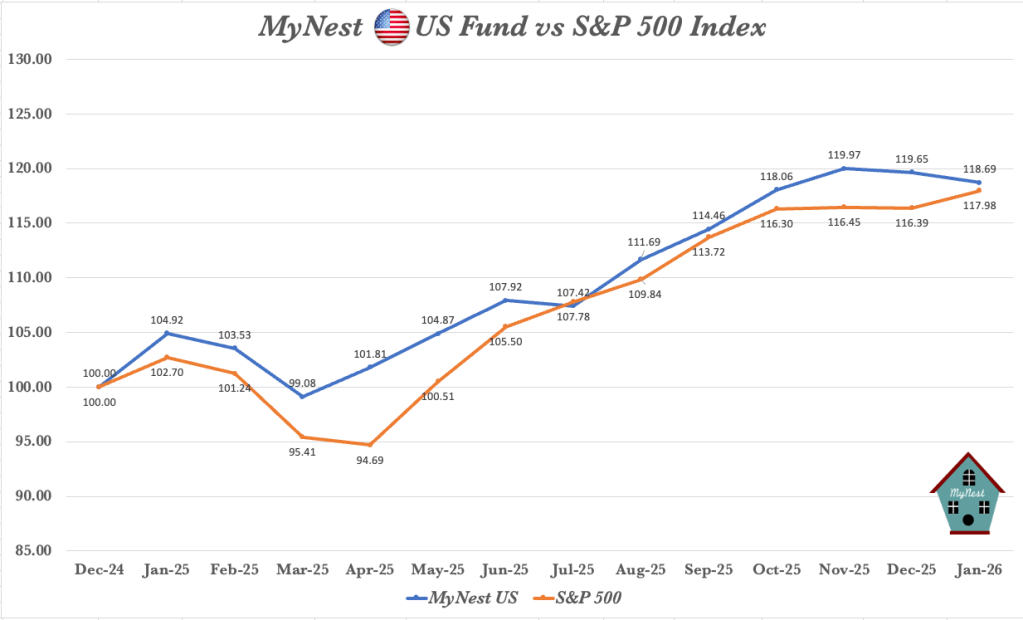

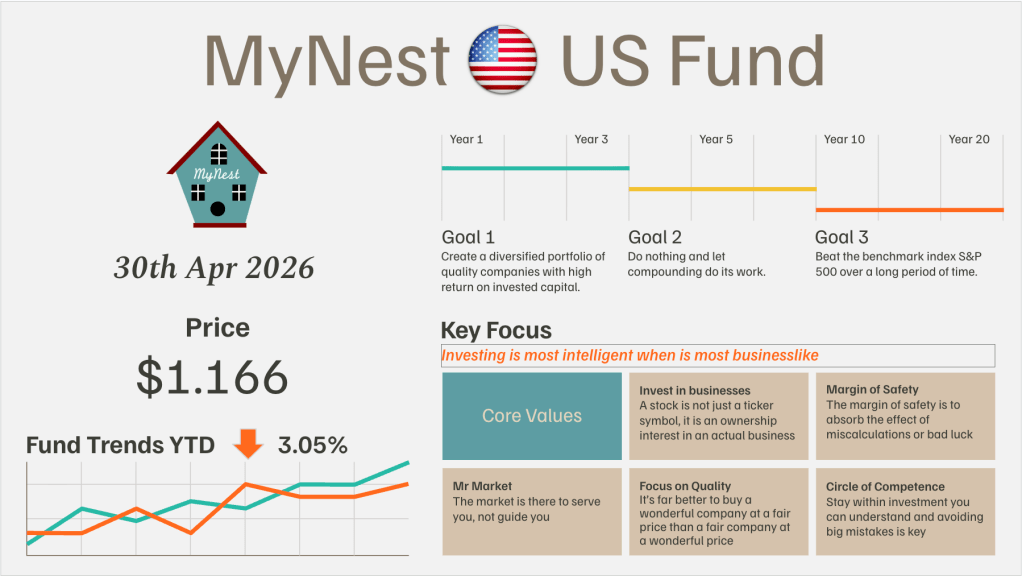

MyNest US Fund Performance

Our lead over the S&P 500 index had narrowed as AI related stocks continued to strengthen through the month.

We remain focused on the three core goals:

- Diversify into quality companies with high returns on capital

- Do nothing and let compounding work

- Beat the benchmark over the long haul

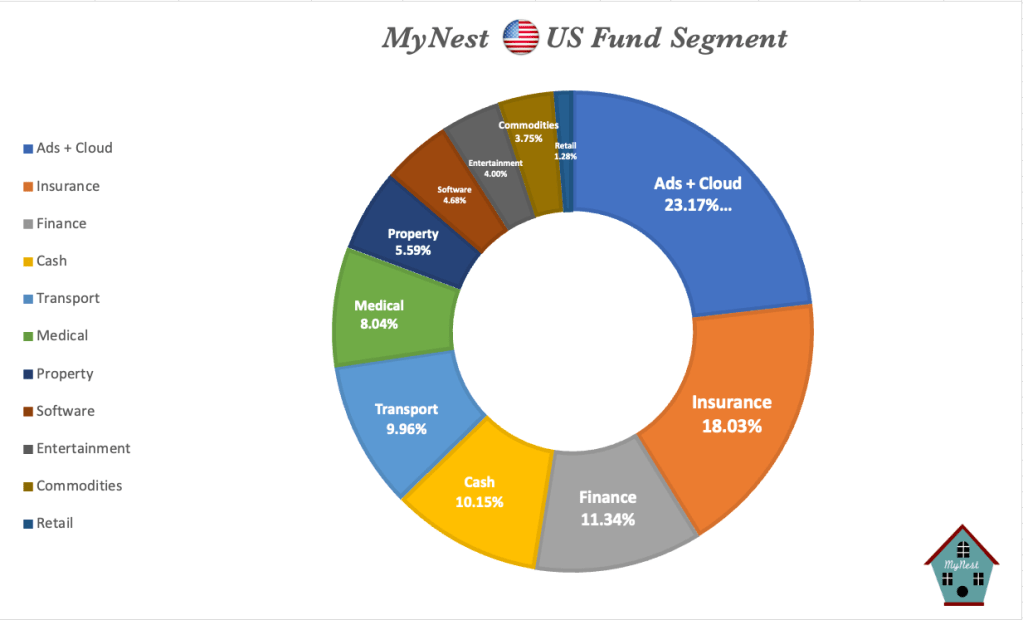

Segment Chart

-

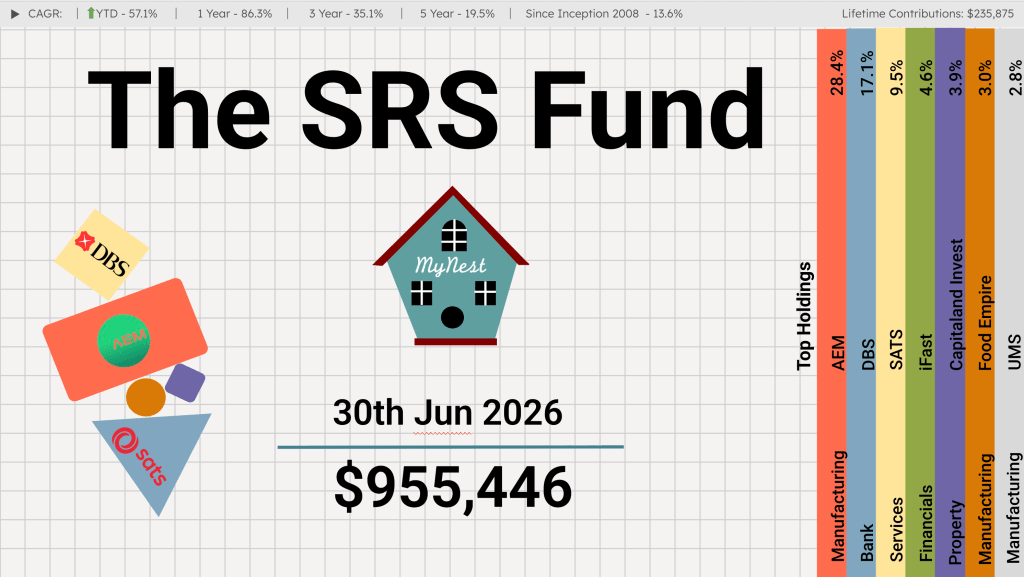

The SRS Fund Jun 2026

The month of Jun provided an important milestone in the Iran conflict. The agreement between the United States and Iran marked a significant step towards reducing geopolitical tension and reopening a clearer path for global energy flows

-

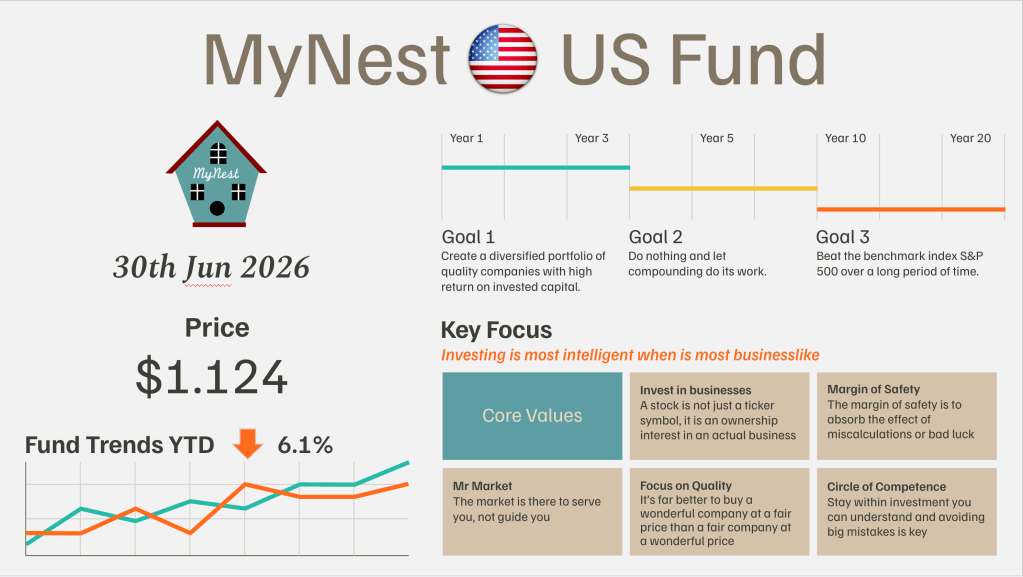

MyNest US Fund Jun 26

June was another remarkable month in the evolution of the global capitalism and the artificial intelligence investment cycle.

-

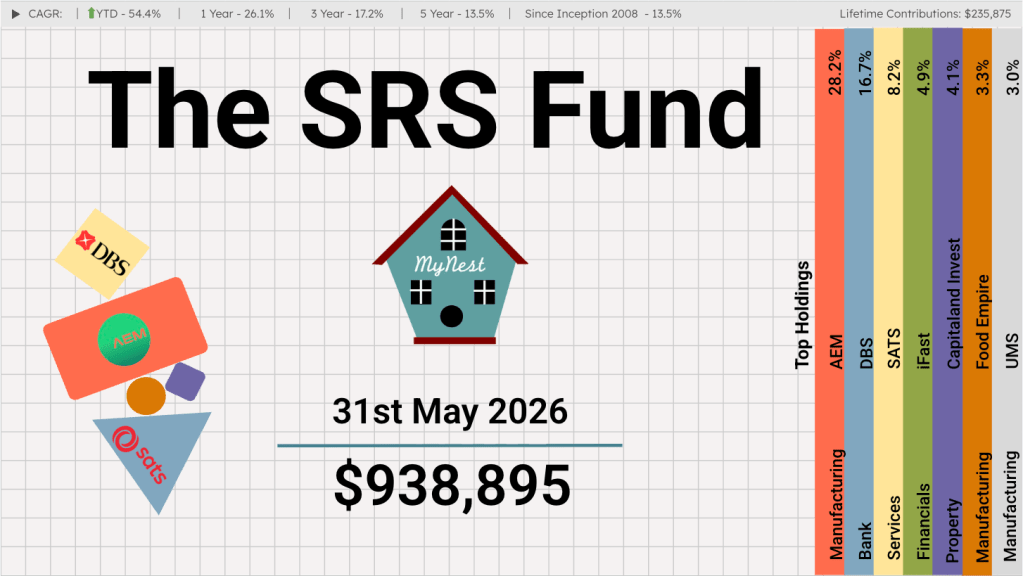

The SRS Fund May 2026

Korea, powered by the worldwide shortage and surge in memory demand, was hit directly by the AI wave, with its stock market more than doubling in a matter of 5 months. Taiwan, already the world’s most important advanced chip manufacturing hub has risen to become one of the largest stock market globally.

-

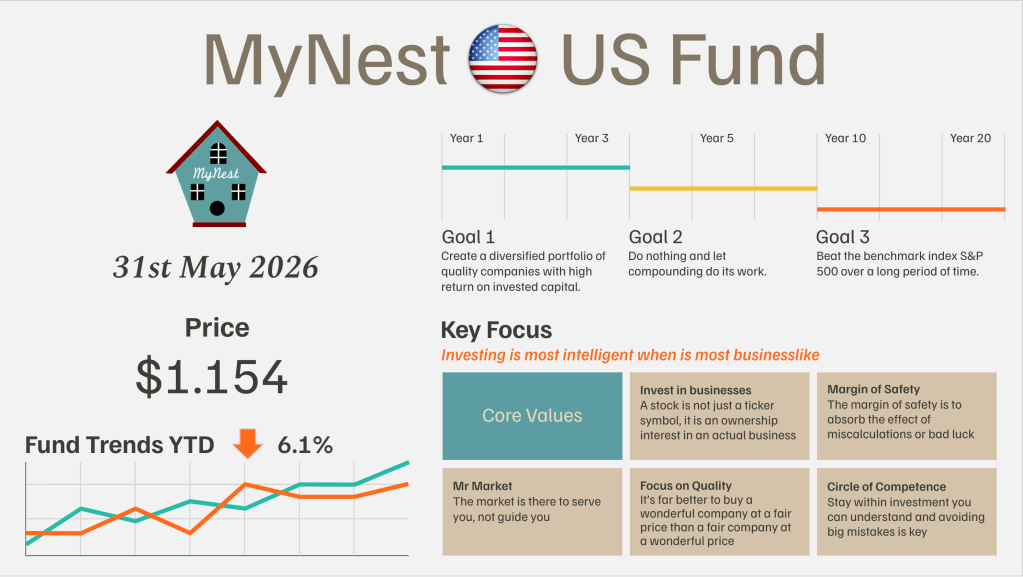

MyNest US Fund May 26

May has been an incredibly illuminating month for the MyNest US Fund. Looking across the broader landscape, the S&P 500 Index has continued its steady leg up, gaining +5.15% in the month of May alone to push its Year-to-Date (YTD) gain to +10.73%.

-

The SRS Fund Apr 2026

In my investment journey, there have been three occasions where I witnessed a company deliver a 10x return.

-

MyNest US Fund Apr 26

The market rebounded strongly in April as investors appeared to look past geopolitical uncertainty and renewed their focus on earnings, artificial intelligence, and the long-term growth prospects of quality businesses.