A Long Term Horizon

The SRS fund is constructed base with a focus on financial and real estate sector using a diversified portfolio of stocks with good long term fundamentals. The investment horizon is long term in nature with its mandatory first withdrawal date set at the age of 62.

A portfolio with a long term horizon is certain to go through market crashes probably several times along the way. While the investor is unable to control factors such as interest rates and inflation, one can certainly choose to invest in businesses that can weather through all types of conditions.

The rise in interest rate is like a tsunami submerging all REITs due to its sudden impact. The stronger REITs with good sponsor will likely survive while those weaker ones will eventually drown. On the other hand raising interest rates started to fuel banks earnings giving the portfolio a good balancing effect.

Investors with a long term horizon need not worry too much about the impact caused by interest rate cycle as the very term cycle means is self correcting and oscillating.

As risk free rates moves up, valuation of REITs will have to fall to compensate for the risk premium. When risk free rates fall risk premium will also subsequently be reduced.

Overall however investors needs to demand returns exceeding inflation because a high return simply meant for nothing if the eventual purchasing power is lost.

In the medium terms of 3 to 5 years, I expect inflation to hover in between the 4% – 6% level and I consider this level of discount rate/interest rate to be reasonable in the calculation of intrinsic value of companies.

This higher hurdle means a more conservative approach to valuation and as such equity prices in particular the US market will need to come down. The same cannot be said of the China market where valuations have almost reached scream buy levels (huge margin of safety if numbers are legit). I consider the Singapore market to be fairly valued and expect continue interest rate pressure in the REITs sector.

The SRS Fund Review Oct 2022

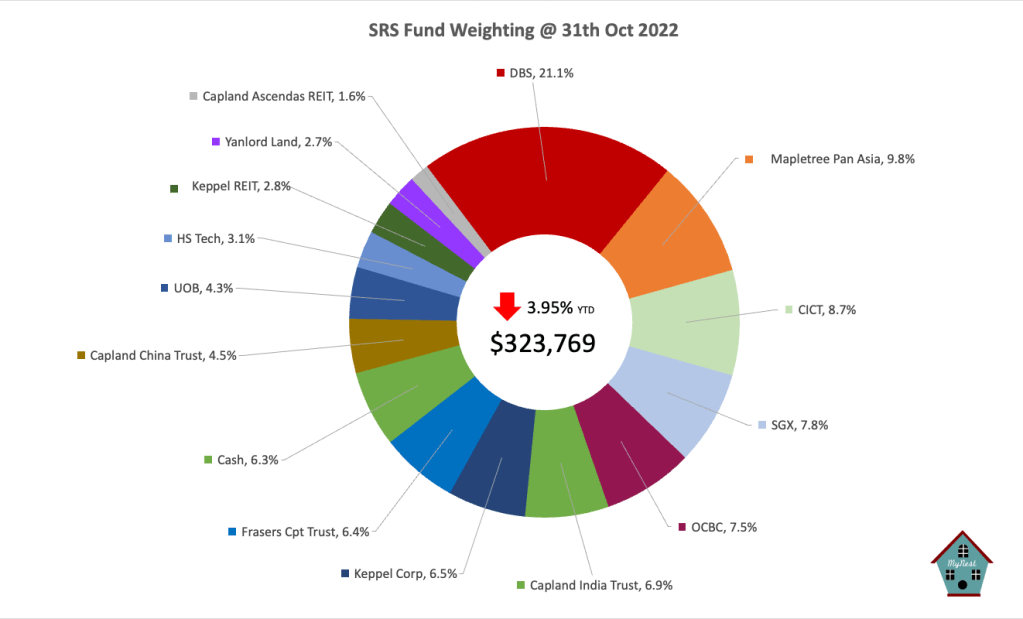

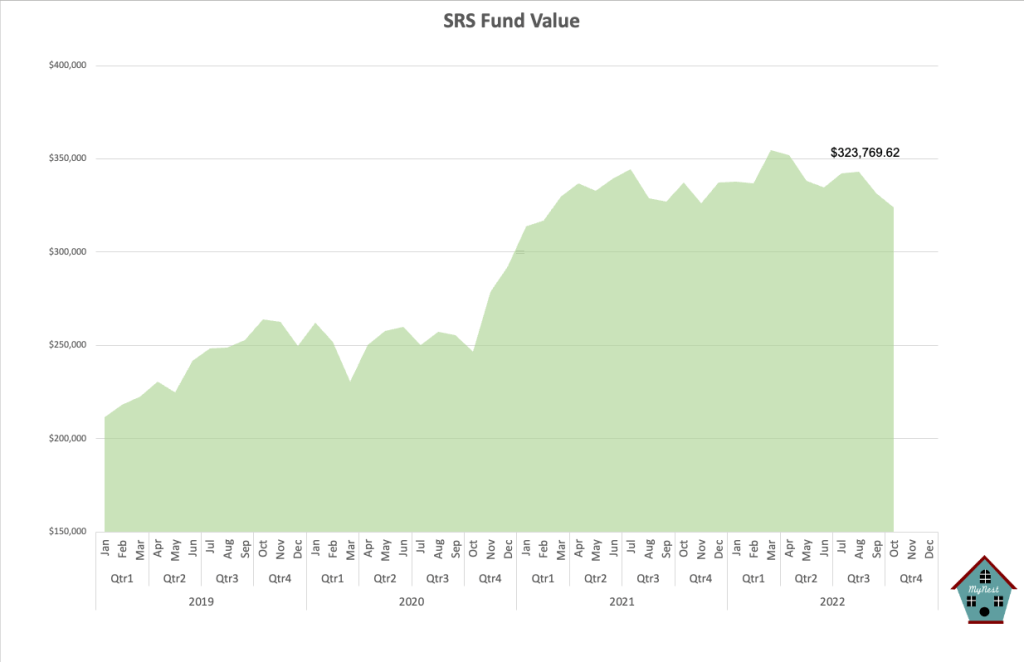

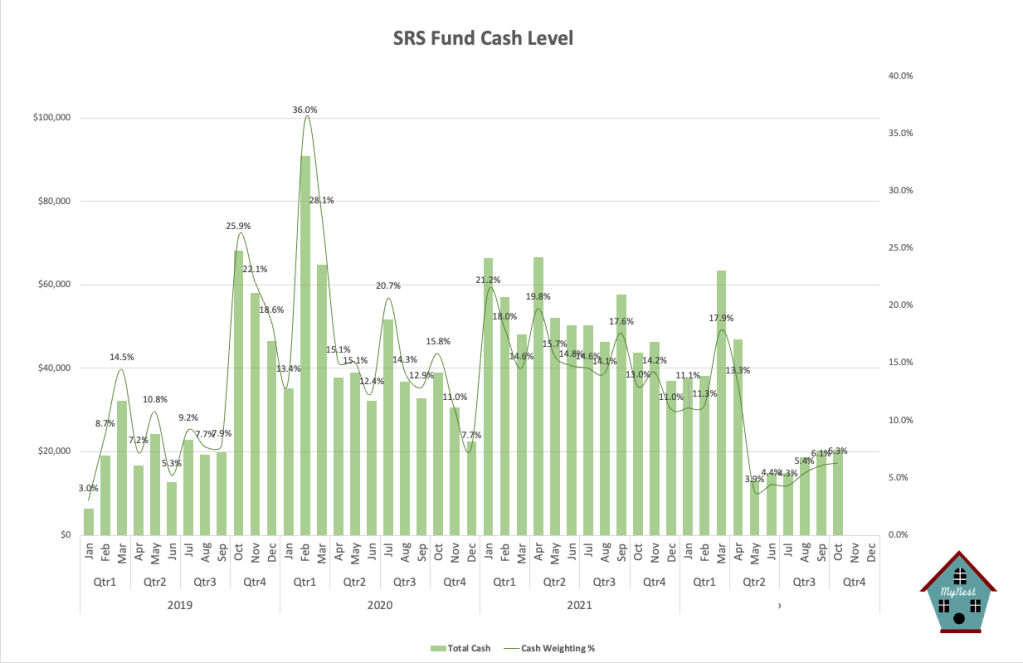

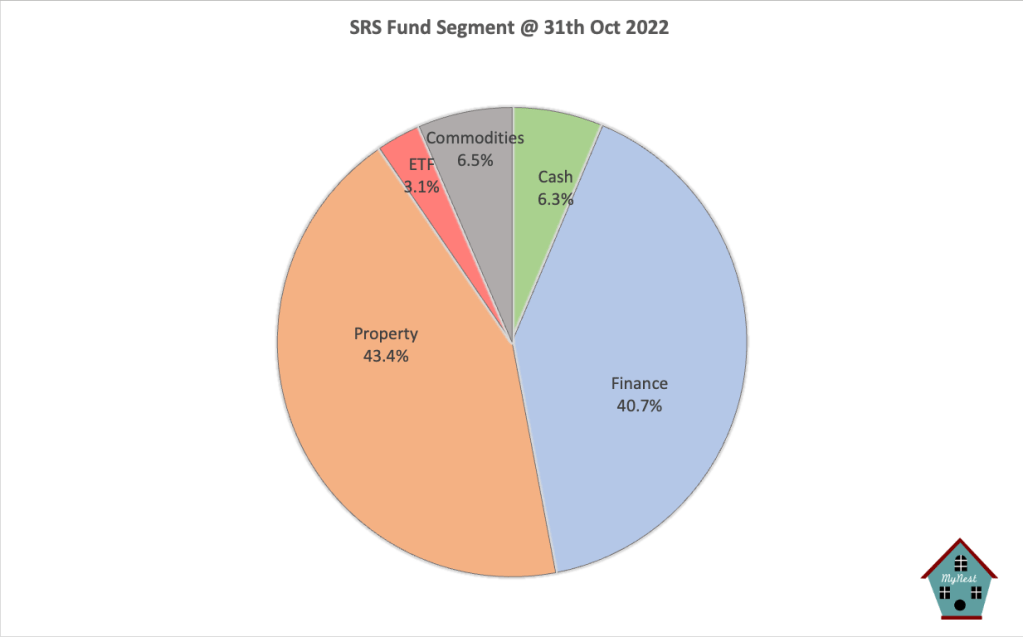

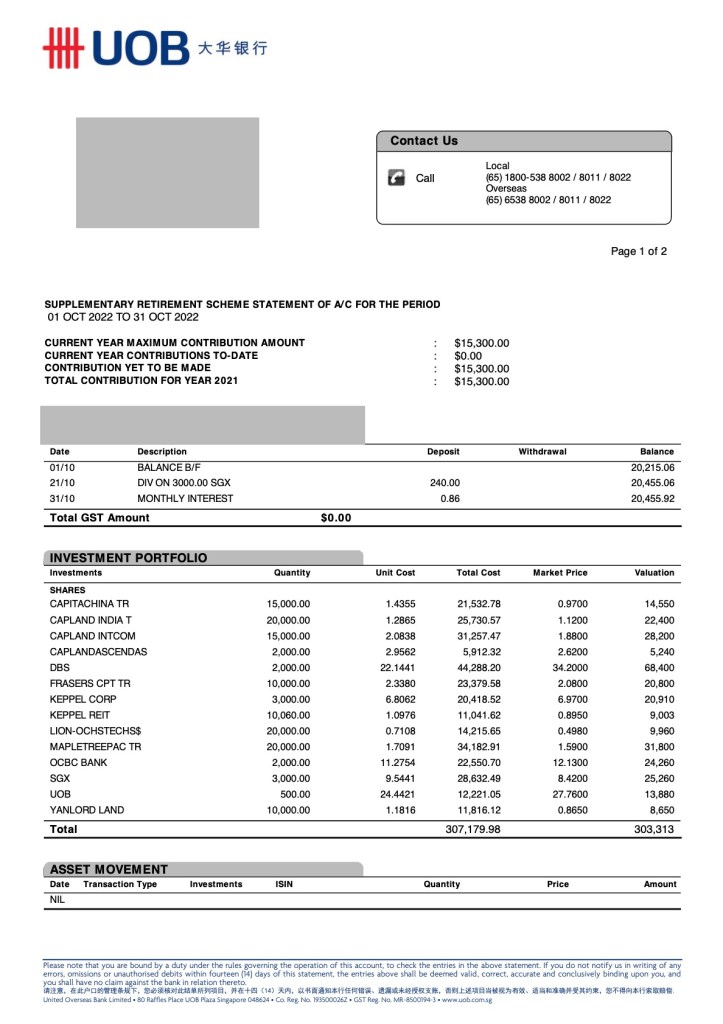

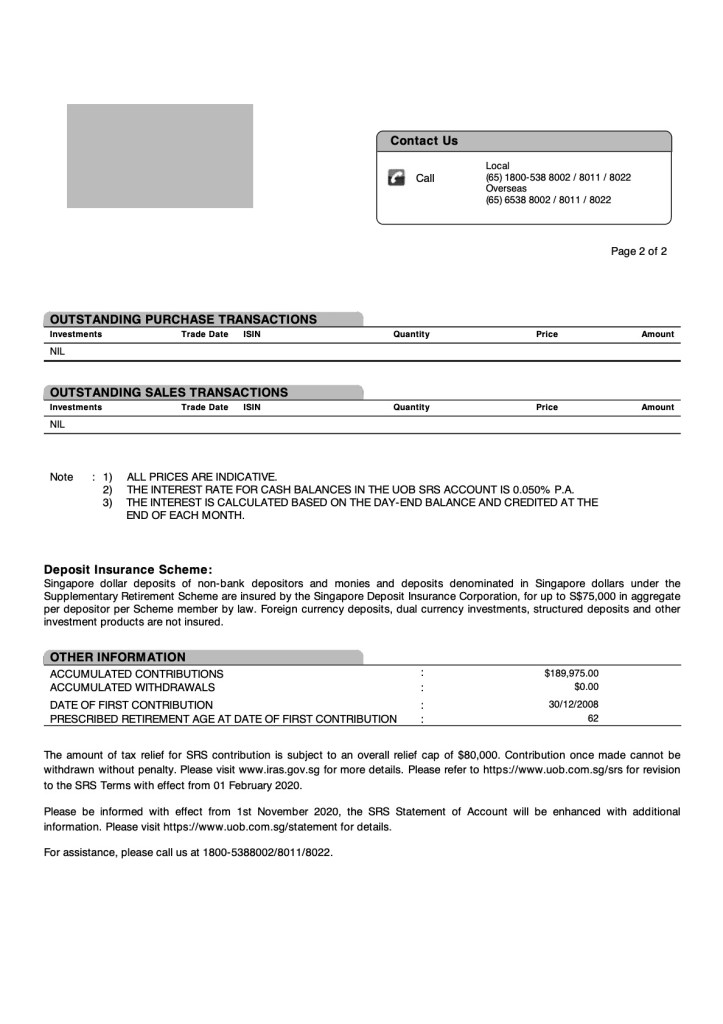

The month of Oct extended Sep losses in REITs as the sector continue to reprice from higher rates. Banks report a stellar set of results due to increasing net interest margins. Again I have continue to sit on my ass and do nothing to the portfolio to not only reduce frictional cost but wait for business especially the REITs to start peddling especially now they are at the deep end of the pool.

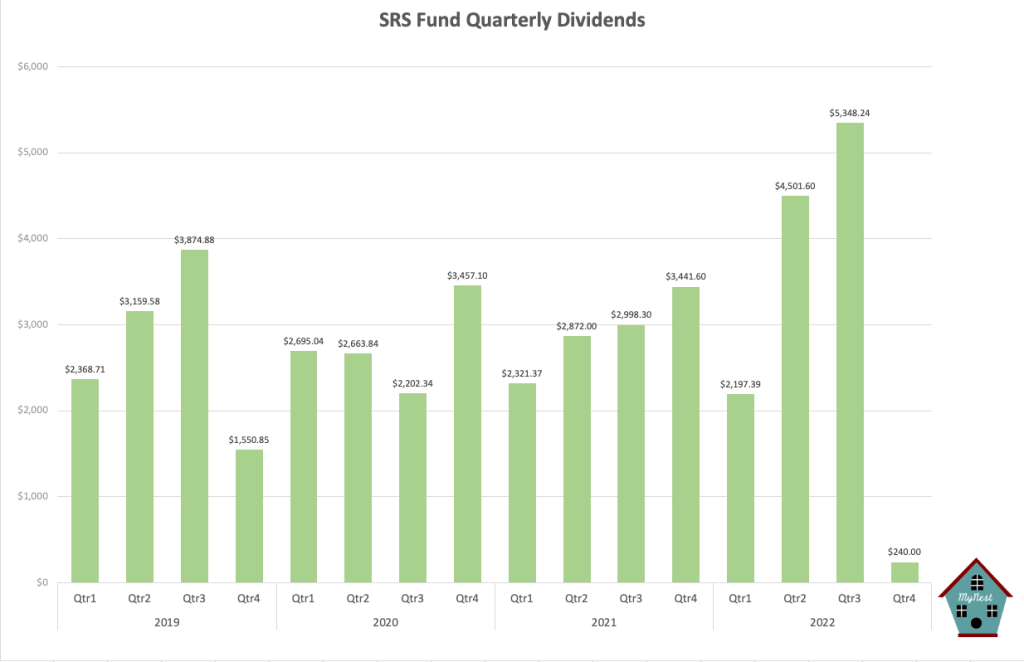

Dividend in Q4 should normalise to around the $2,000++ level and is expected to boost the portfolio cash to around 7% of portfolio. I will continue to seek investment opportunities with the fall in valuation of many companies. There is also a likelihood for the portfolio cash to be place in short term risk free as it approaches the 5% return level.

-

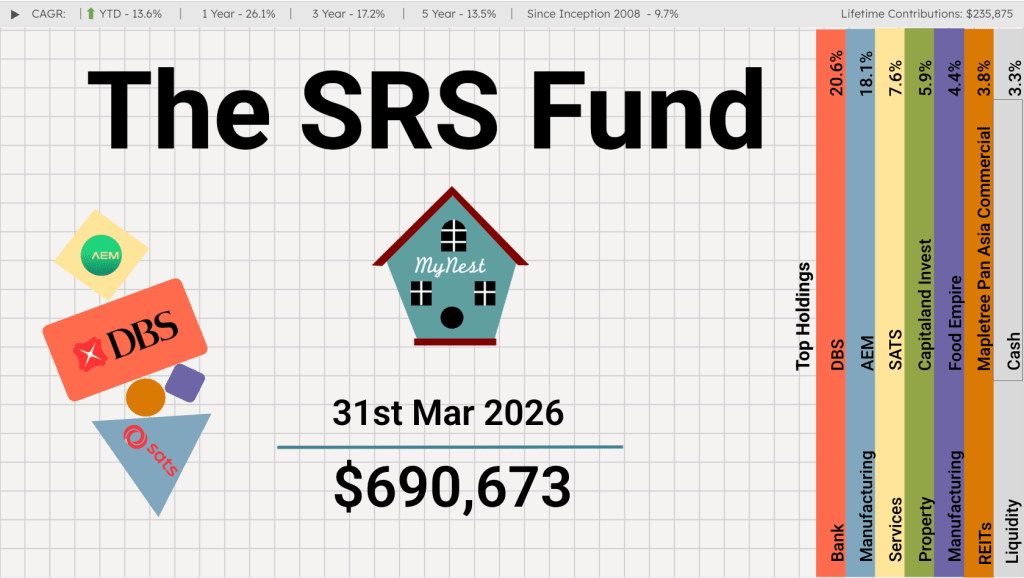

The SRS Fund Mar 2026

It is an enduring market reality that a concentrated minority of holdings drives the vast majority of returns. For years, DBS (currently the largest individual holding at 20.6%) has served as the compounding engine of the SRS Fund.

-

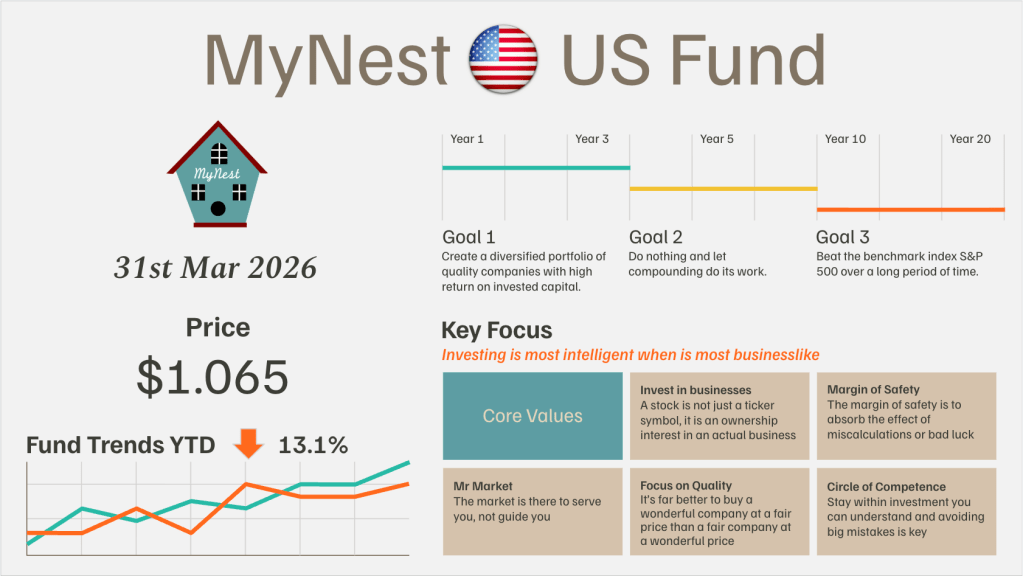

MyNest US Fund Mar 26

March shattered any lingering market complacency, pivoting sharply from the localized damage of the “SaaS-pocalypse” to a systemic shock driven by the war in Iran.

-

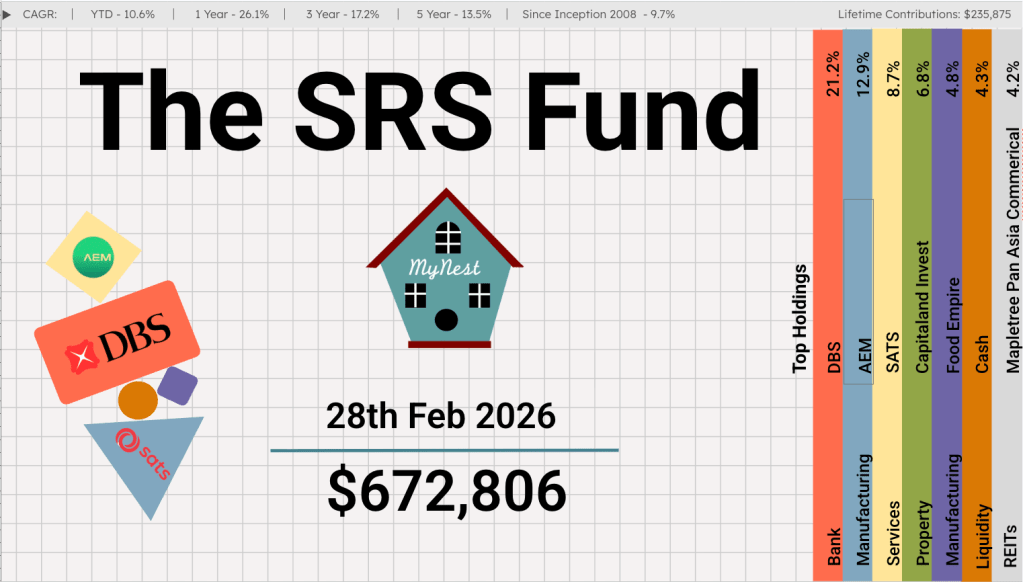

The SRS Fund Feb 2026

The Singapore Budget 2026 has set a robust backdrop for local investors. For the third consecutive year, the government is operating from a position of immense “dry powder,” with an overall fiscal surplus of $8.5 billion projected for FY2026.

-

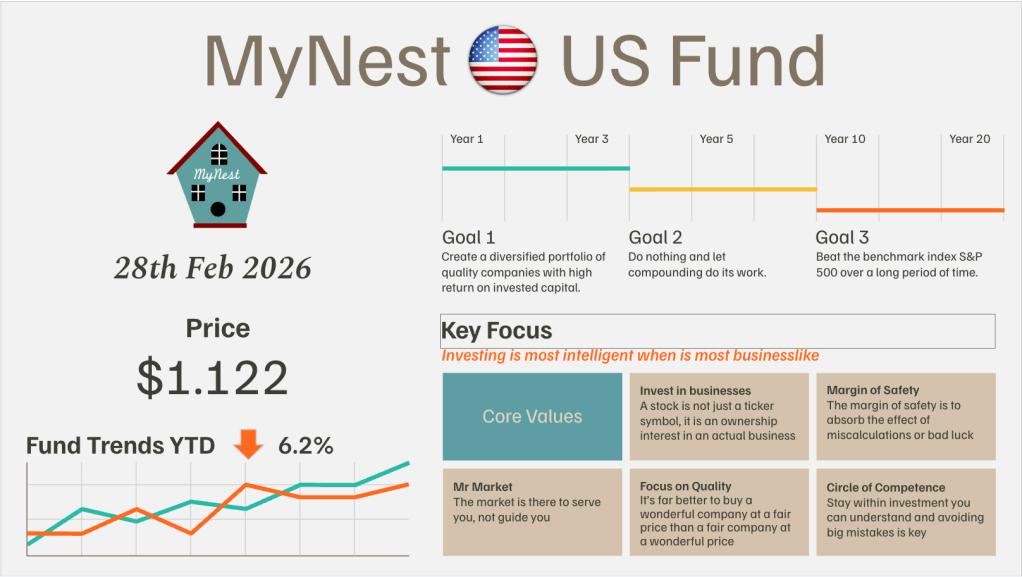

MyNest US Fund Feb 26

February 2026 proved to be one of the most challenging months for our fund since its inception. A wave of “AI anxiety” swept through the Software-as-a-Service (SaaS) sector

-

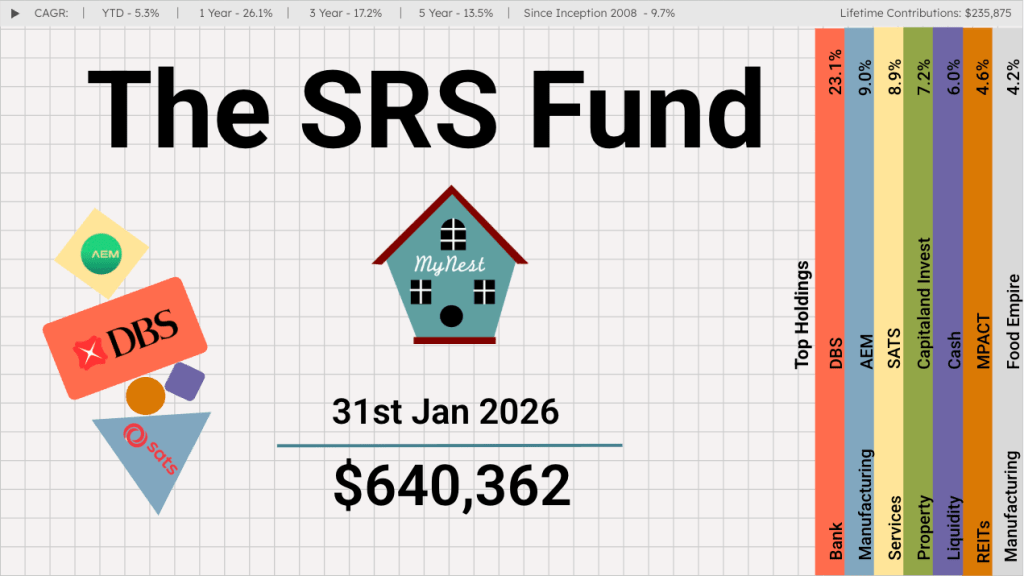

The SRS Fund Jan 2026

After a blockbuster 2025 that saw GDP growth hit a surprise 4.8%, the first month of 2026 has proven that the momentum is far from a fluke. Between record-breaking stock market performance and massive industrial investments, the “Little Red Dot” is making a very big noise.

-

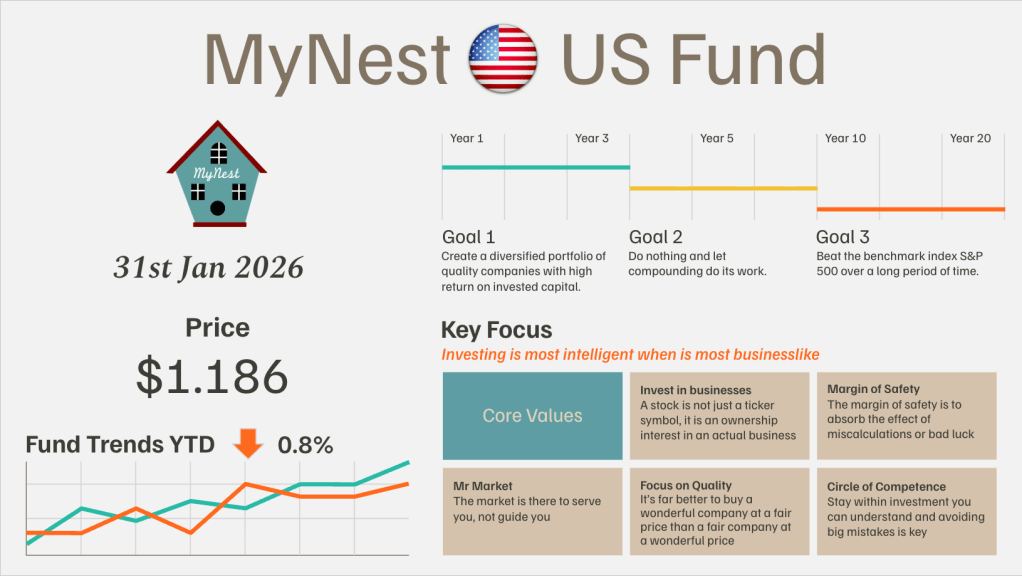

MyNest US Fund Jan 26

I have a confession to make. After reading Chip War at the end of 2022, I fully grasped the strategic importance of TSMC and ASML in the global semiconductor supply chain.