Chicken or Egg First?

Does low interest rates cause inflation or inflation brings about higher interest rates?

In a populist democratic world the default will always be lower interest rates as this bring financial comfort to the masses. The underlying assumption will be price stability as without it any incremental financial comfort one may benefits from low interest rates will be eroded by higher everything prices.

Hence we can conclude that it’s inflation that leads interest rate both higher and lower.

In November with some signs of slowing inflation I believe the stock market had jumped the gun to rally optimistically in tandem of retreating bond yield.

Like the old saying goes don’t count the chickens before they hatch. The Fed had sensibly guided to a slow down in rates increases as well as to hold rates high for a reasonable amount of time to tame inflation.

As such more pain is expected throughout 2023 even though the intensity may have dropped. Just like taking a pain killer it is easy to feel optimistic when the pain is lowered. The relief rally here will hence likely be short lived.

As of the time of writing, the China recovery may be well on its way as policy changes made to Covid reopening in China spark a rebound in Chinese equities that are selling at dirt cheap prices.

We may see the tale of 2 countries play out in 2023 where China takes the lead in driving the global economy while the US takes a back seat fighting inflation.

The SRS Fund Review Nov 2022

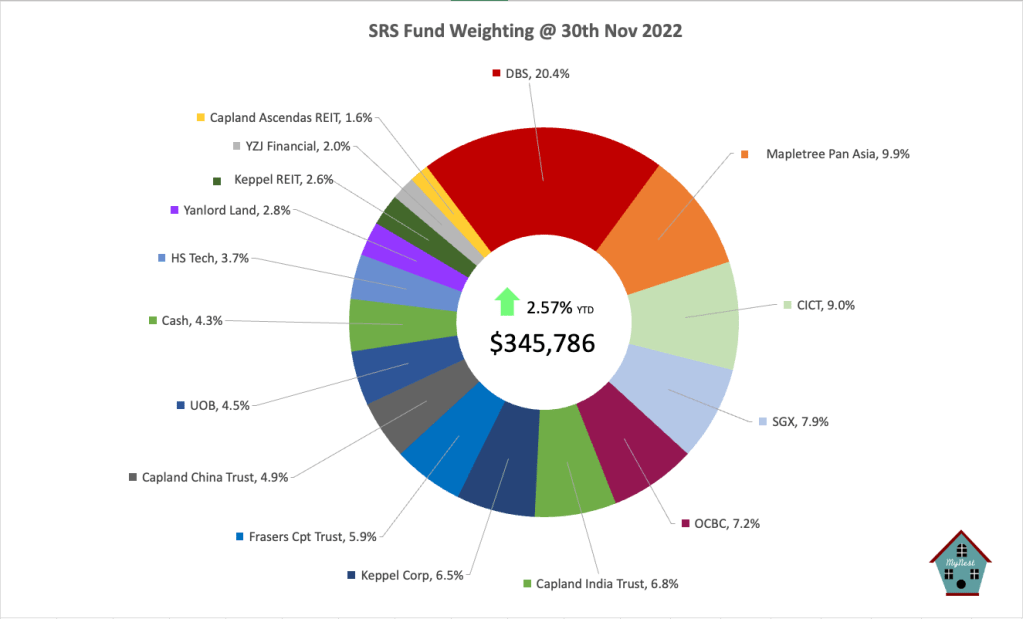

In Nov the fund welcome a new counter to the portfolio. YZJ Financials a spinoff from YZJ Shipbuilding was added. My investment thesis for this addition is as follows

- Cheap Valuation 35c to a dollar

- China reopening to improve value of its portfolio

- Continuous share buybacks and pledge by owner to acquire more if valuation stays low

- YZJ Shipbuilding uninterrupted dividend payout bores well for YZJ Financial dividend stability

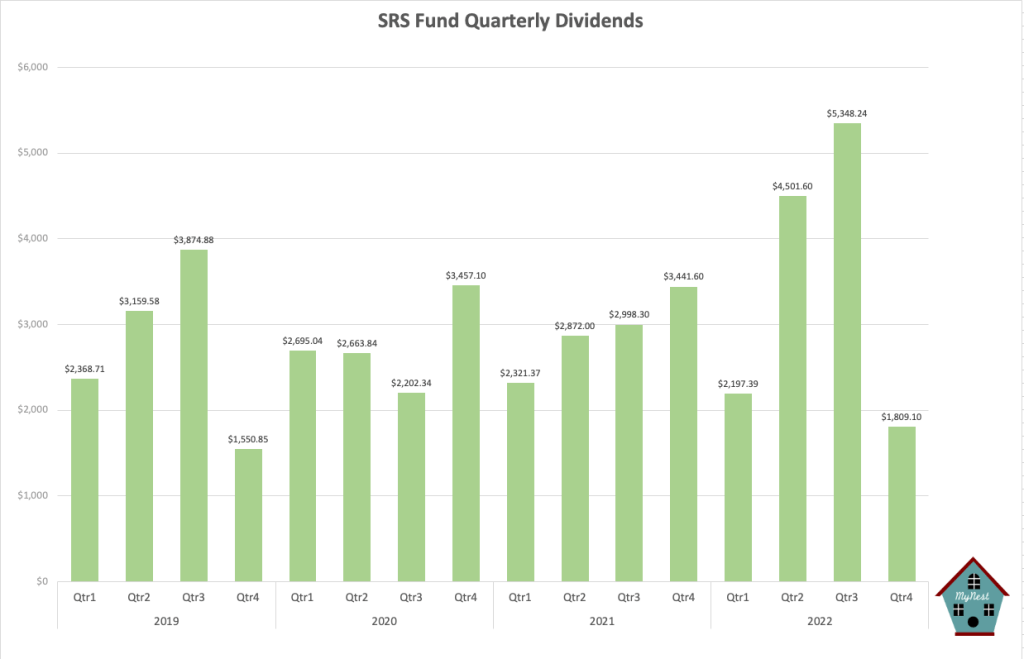

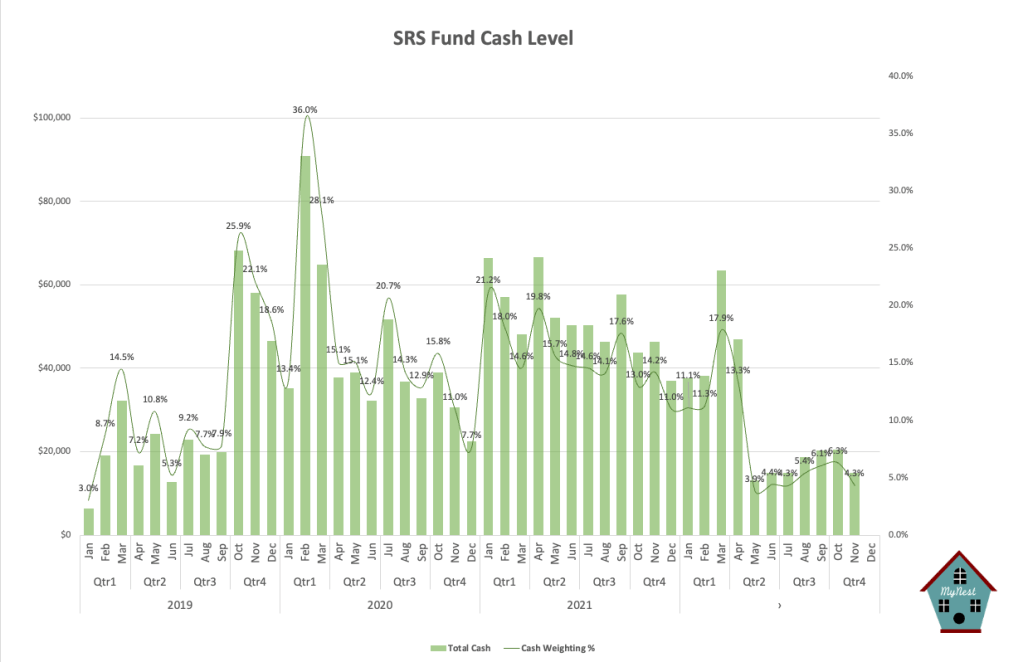

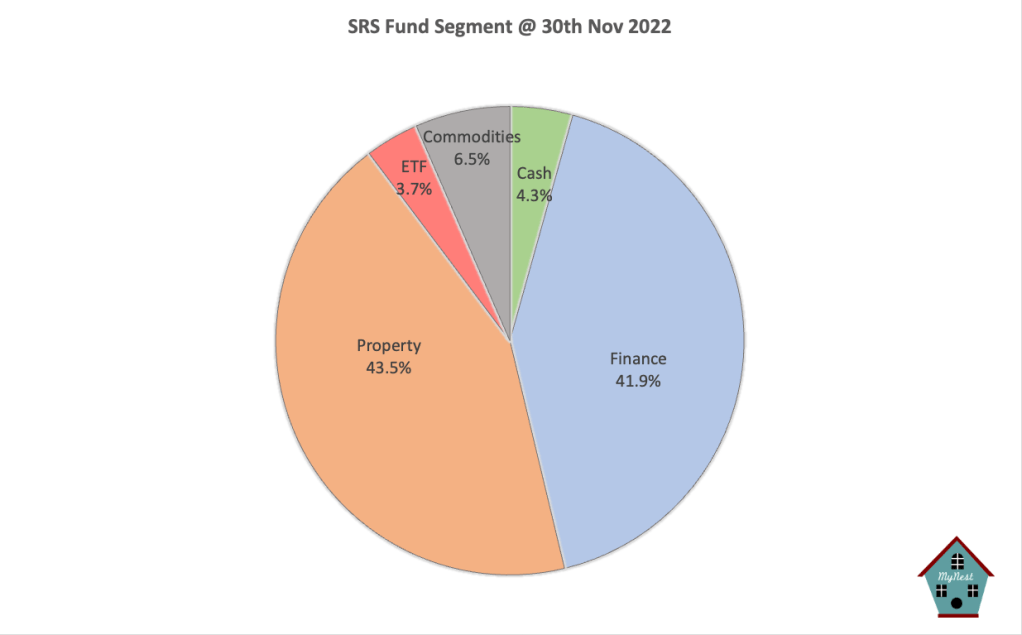

With this addition cash level dropped to 4.3% with Q4 dividend coming in above the $2k level. Dividend for 2022 will come in at above $13k for the fund and is expect to climb to record high in 2023 given record earnings from banks and stable returns from REITs.

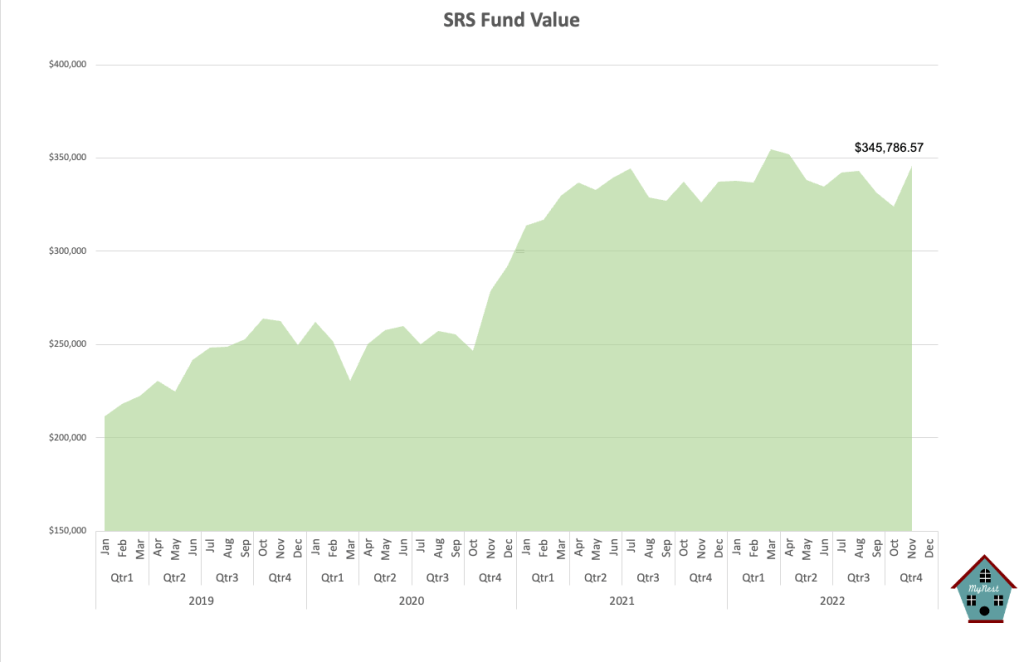

Investment into Keppel Corp yielded a nice return as it continue its upward march. HS Tech also seems to be turning the corner following events in China. In all however the fund will likely lagged STI in 2022 due to the drag by higher interest rates on REITs in the fund.

Longer term the fund should continue to outperform the benchmark as I continue to seek alpha companies that will grow faster than those in the index.

-

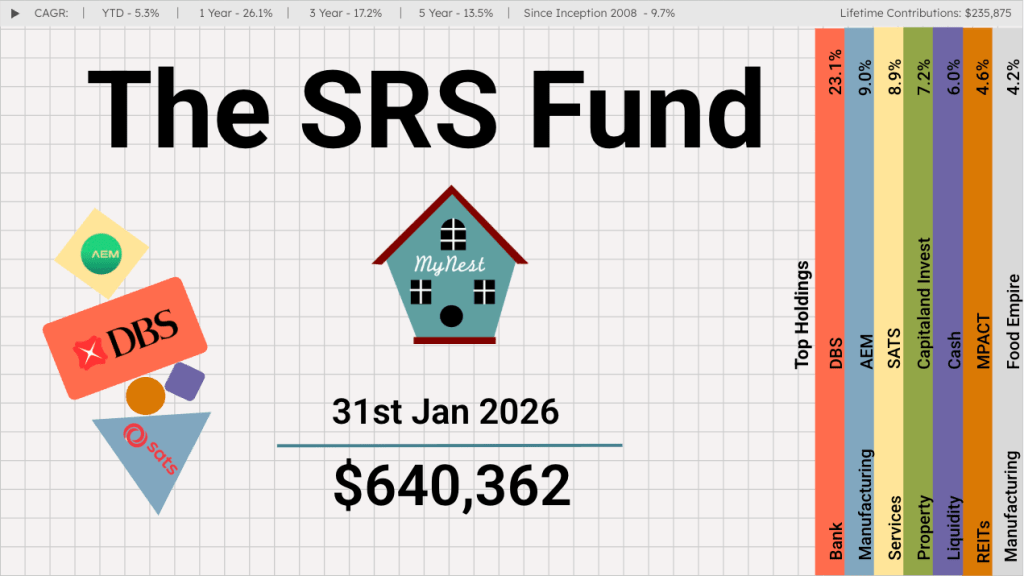

The SRS Fund Jan 2026

After a blockbuster 2025 that saw GDP growth hit a surprise 4.8%, the first month of 2026 has proven that the momentum is far from a fluke. Between record-breaking stock market performance and massive industrial investments, the “Little Red Dot” is making a very big noise.

-

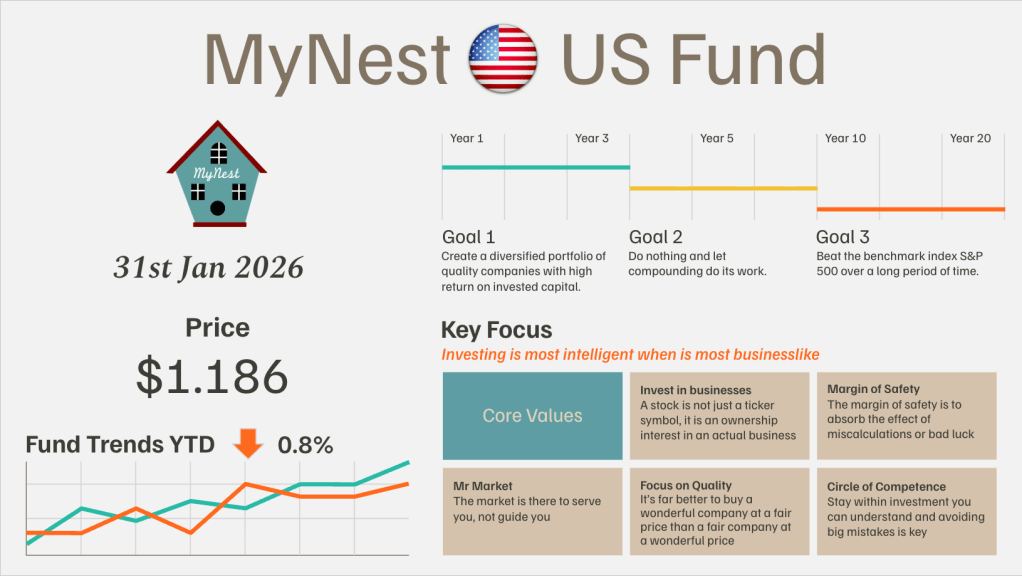

MyNest US Fund Jan 26

I have a confession to make. After reading Chip War at the end of 2022, I fully grasped the strategic importance of TSMC and ASML in the global semiconductor supply chain.

-

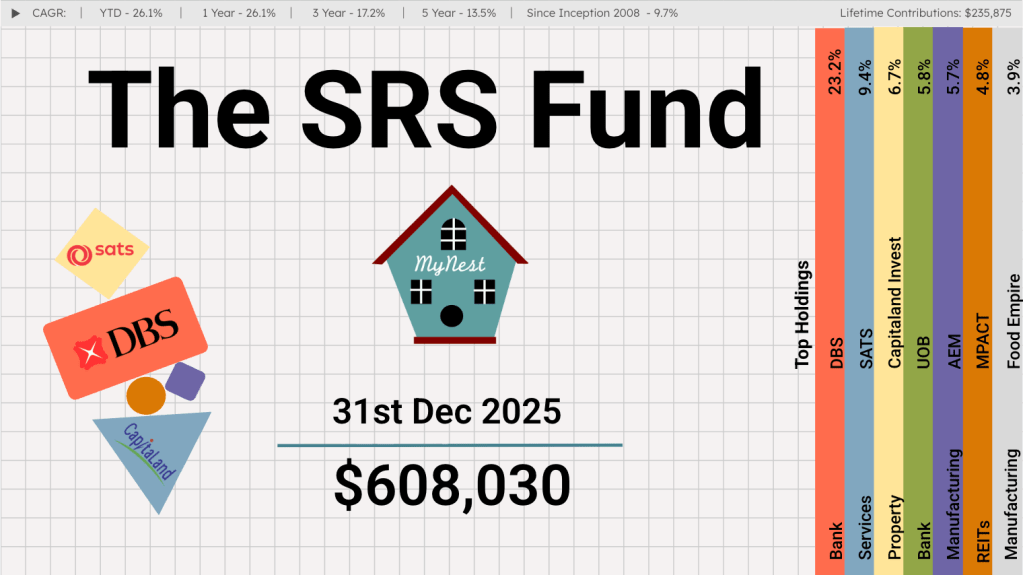

The SRS Fund Dec 2025

If someone had told me at the start of the year that the Singapore stock market would deliver returns in excess of 20%, I would have shrugged it off as wishful thinking.

-

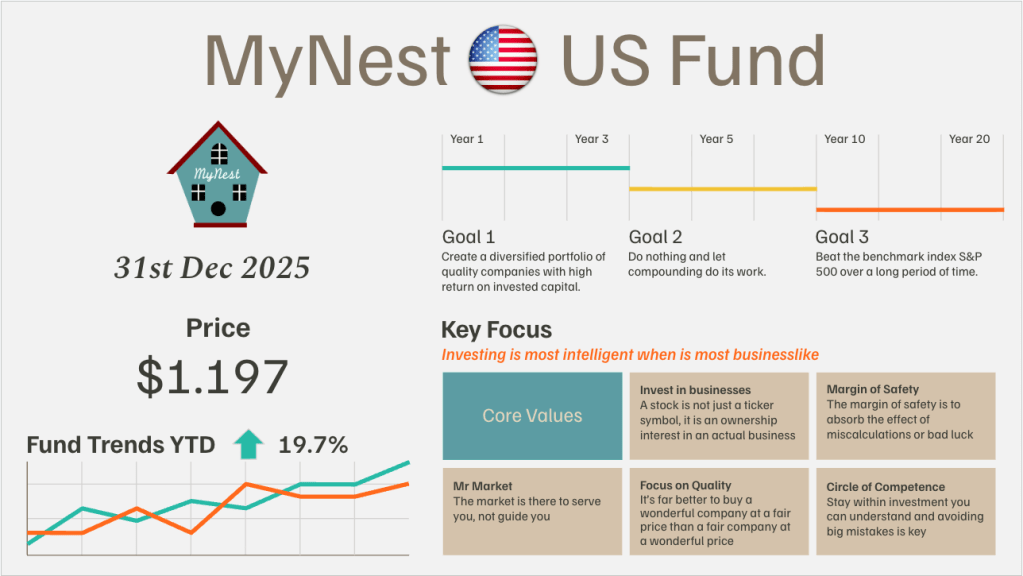

MyNest US Fund Dec 25

MyNest US Fund rounded the first year of inception with a slight outperformance to our benchmark the S&P 500. The first year of operation tested to resolve in knowing what we own as we navigated volatility which started on Trump’s Liberation Day.

-

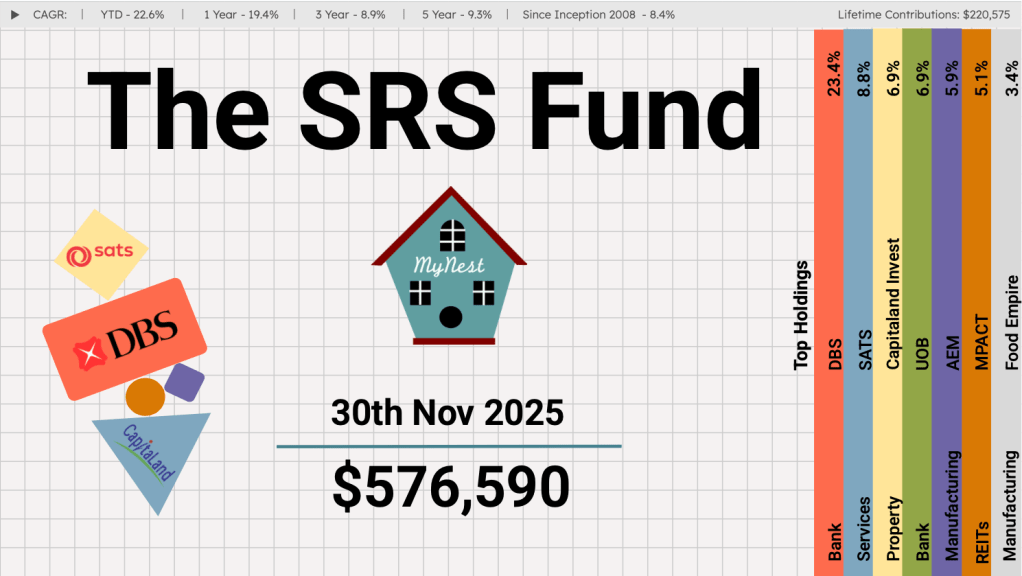

The SRS Fund Nov 2025

If you’ve been watching the Singapore market this past month, the narrative has been impossible to ignore: it is a tale of three banks, and unfortunately for UOB, it has found itself lagging its peers.

-

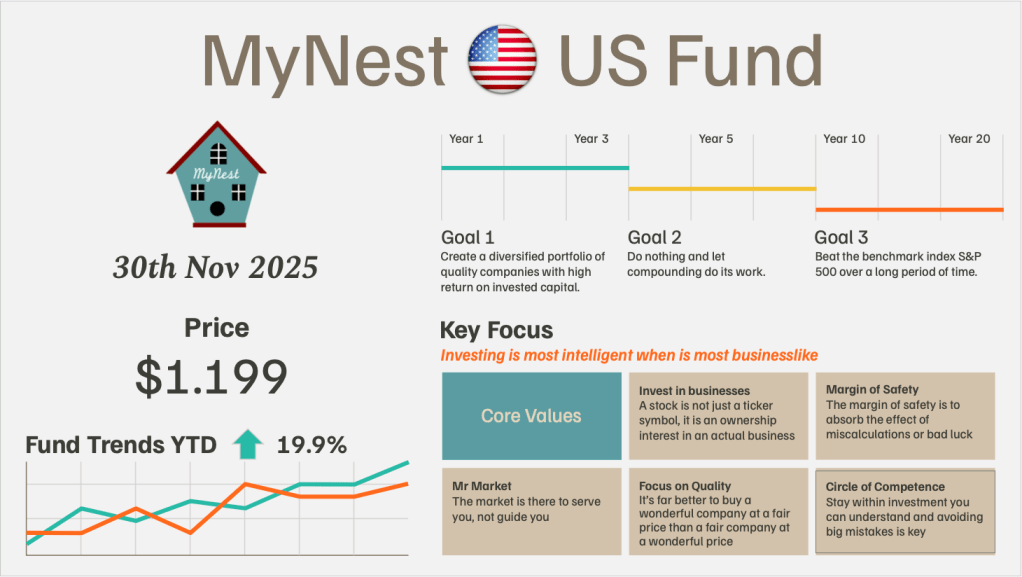

MyNest US Fund Nov 25

November tested the patience of the broader market, defined by a distinct shift in sentiment regarding Artificial Intelligence. The narrative of an “AI Bubble” finally took hold,