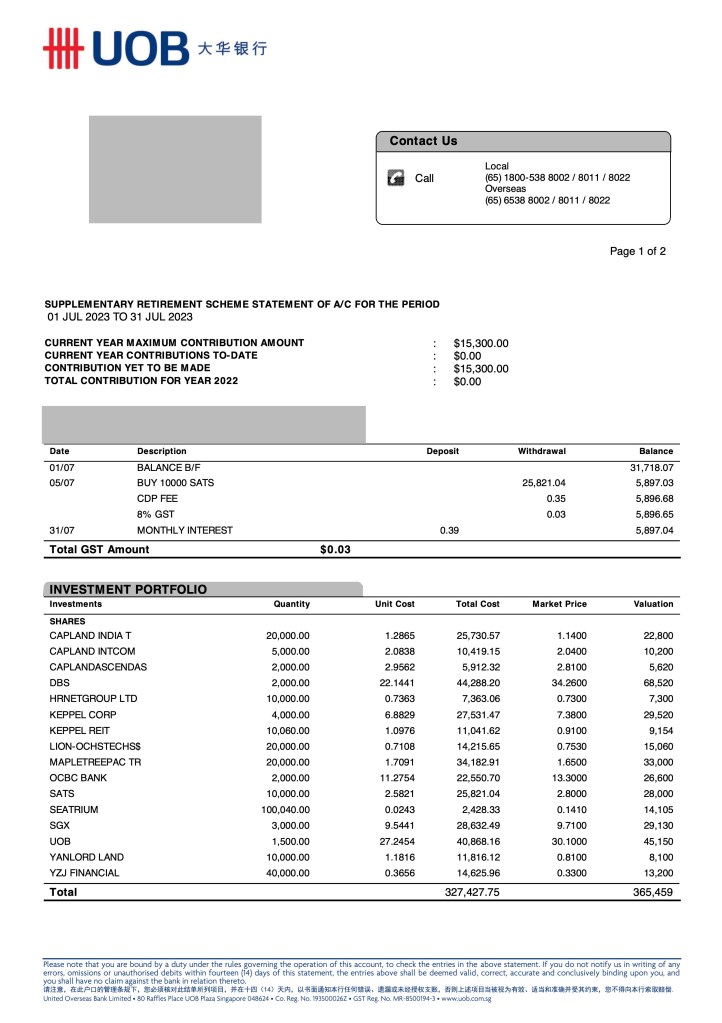

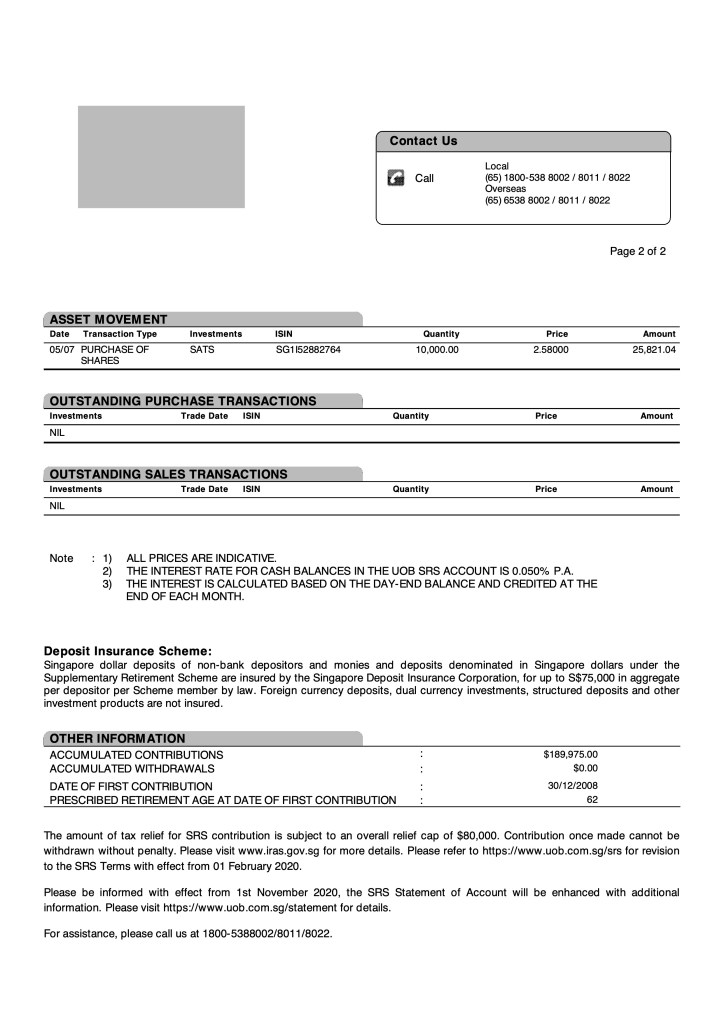

Recently I decided to made some changes and separate my monthly article with the SRS Fund update. This change enable me to better focus on the fund itself as well as the underlying companies. As mention in my last month update, I added SATS into the SRS Fund with my thesis of the revenge travel boom.

However during SATS Annual General Meeting the CEO mention that things was not as rosy for the Air Cargo part of the business (especially for the latest upcoming quarter) and it will certainly take time to see result of the merger with WFS. While SATS share price has risen since my purchase, I expect to see limited upside until the company return to profitability.

The Good

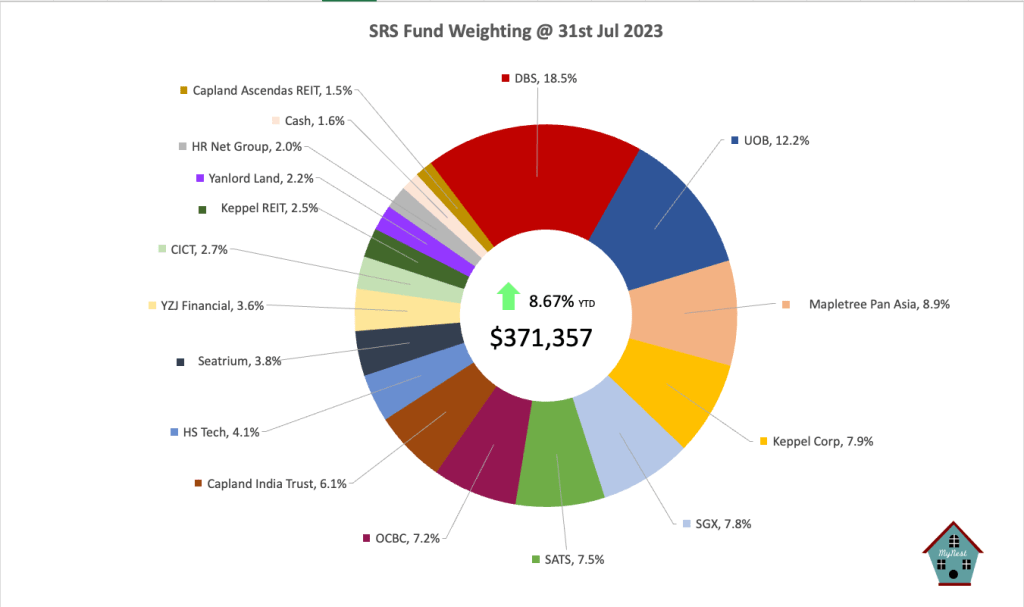

Previous bets are starting to payoff starting with the reduction of REITs holdings into Banks as I added more UOB during its recent selloff. All 3 banks reported record earnings as interest rate normalise. This is also to suggest it will likely take another 2008 typed financial crisis to see ultra low interest rate that we had so enjoy over the past 15 years.

Hence conclusion for banks, their recent results are normalise earnings and they are not one off. The individual bank results will thus be more dependent on their loan quality going forward with a slight tailwind from net interest margin expansion.

The fund is also boosted by our previous investment in Keppel and Seatrium as they embark on different paths. Keppel is on its way of realising value and turning asset light which will likely throw off more actions such as the recently announced Keppel REIT dividend. (Maybe some Keppel DC REITs for shareholders?)

Seatrium while still unprofitable has already amass a gigantic order book that is likely to swell as inflation continue to push up the price of oil. If the US and China get their act together, we will likely switch into 2nd gear of the post Covid recovery adding even more inflationary pressure on oil demand. With the lack of investment into oil and gas due to sustainability focus there is a good chance the world may find itself short in oil production.

The Bad

China had been a start stop in recent months as economic numbers point to a fading recovery after its initial boom. There is currently still no strong sign of the Chinese government getting their act together especially on the real estate front which was the main pillar of the economy in the past decade. The SRS Fund foray into the Chinese market using HST still needs time for it to play out.

The other related company YZJ Financial recently got a share price boost due to record earning by its sister company YZJ Ship Building. I am keeping my fingers cross awaiting YZJ Financial results. However the company is deeply undervalued and it will be a matter of time before this investment pays off.

The Ugly

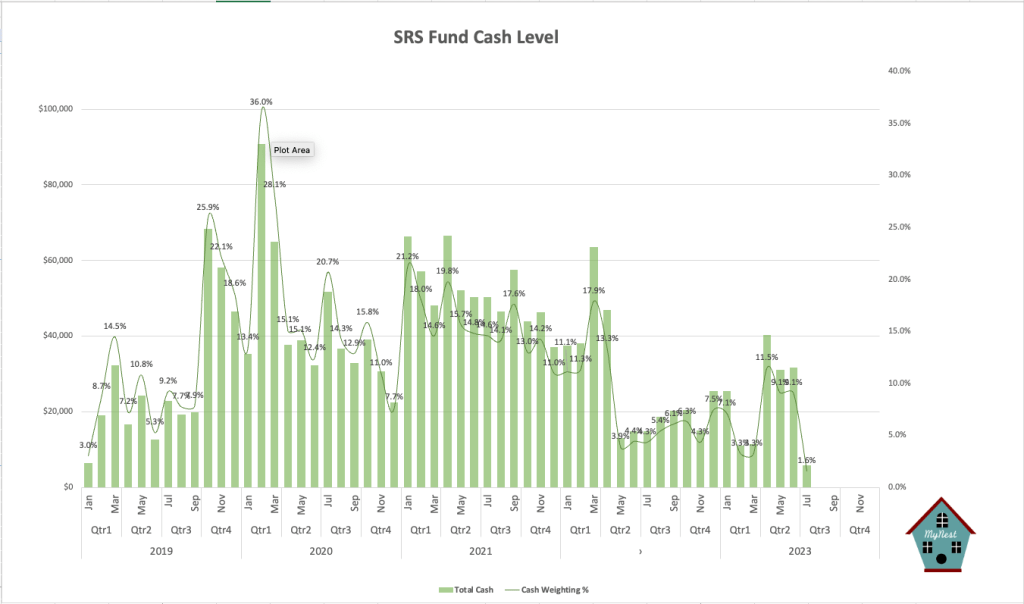

Well I have to count my blessing as I finally got the REITs sector to under 20% of the SRS Fund post July. I have completely dispose CICT at a reasonable price before its result announcement. Bad news continues to flow in the sector as previously highlighted cause of higher interest rate eating into DPU narrative continues to play out. I am horrified by some REITs manager to even consider any acquisitions at this moment in time.

In my view REITs manager should roll up their sleeves and work on improving occupancy rate and really be upfront to their unit holders on the effect of interest rate. Interest payment at 30%-40% of net property income for most REITs at the start of the rate hike cycle will simply be more than 60% after fixed rate hedges run their course. Many disillusioned managers are still holding on to hopes that interest rates will go back down to ultra low levels.

For the SRS Funds we will be bag holders of REITs too. MPACT is currently still a large position with Capland India Trust coming in 2nd. However with less than 20% position size the REITs position will hopefully be less of a drag to the fund.

The worst performer in the fund goes to Yanlord. The company was greedy buying land last year when everyone was fearful. Well it has gotten even more fearful now that China’s real estate is on the brink of collapsing. With Singpore’s real estate sector slowing due to more restrictive measures, it is a double whammy for Yanlord. I guess we can forget about any dividend this year from the company as well.

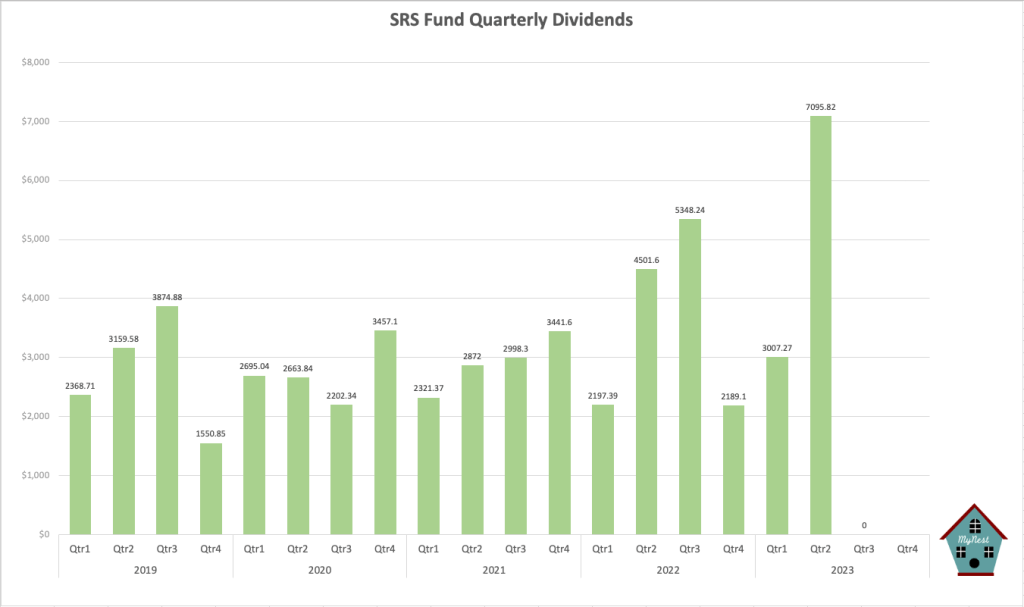

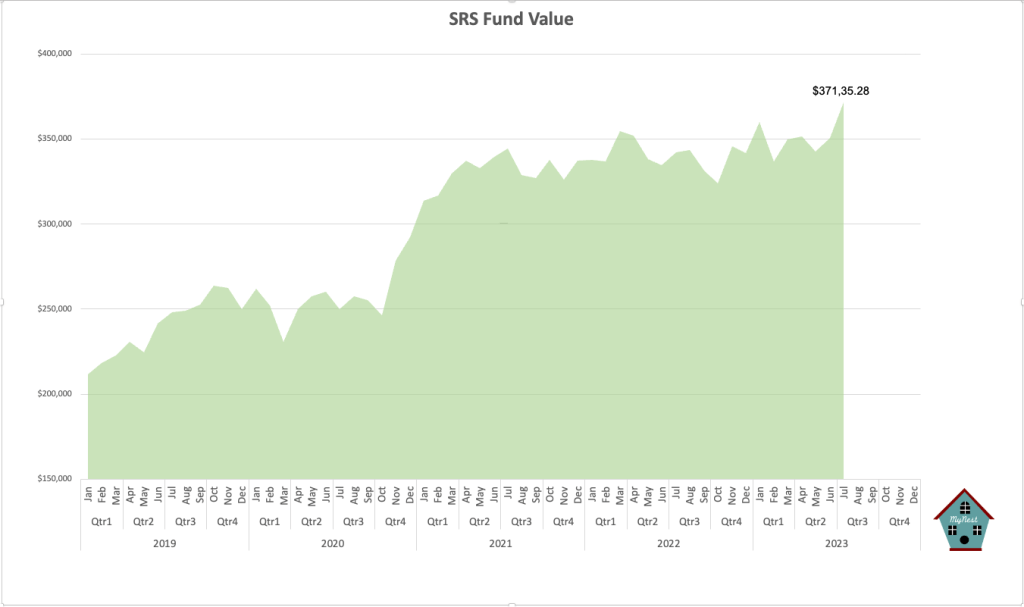

In summary the portfolio had a stellar month out performing the STI by whopping 5% point with even more upcoming dividends on its way. This will likely be the month alpha is created for the year as the SRS Fund returns to it’s index beating way after underperforming past 2 years. I have also made a key decision in August for the fund that will affect its long term trajectory. So do stay tune for the August update and cheers to all investors with the strong market so far.

-

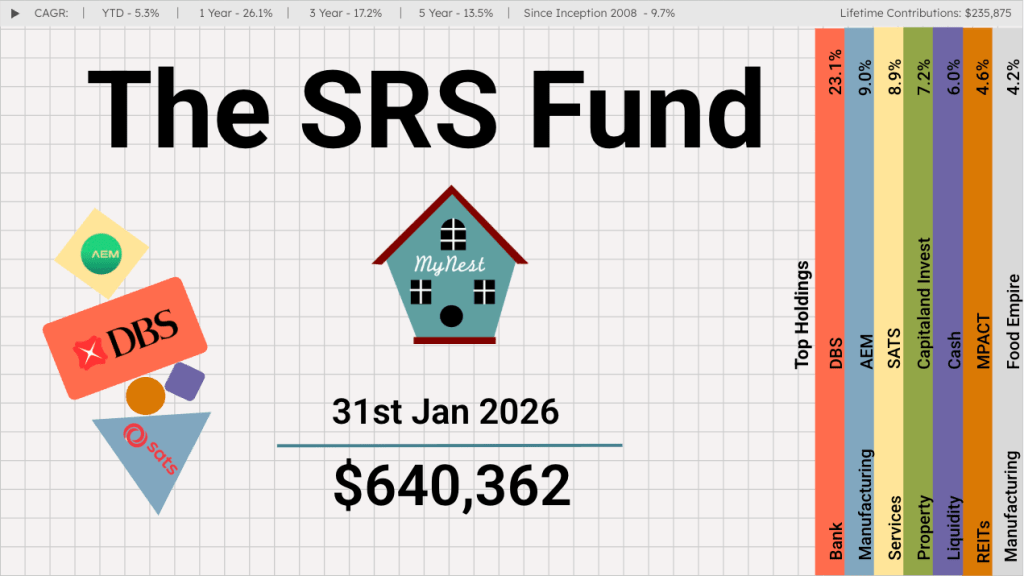

The SRS Fund Jan 2026

After a blockbuster 2025 that saw GDP growth hit a surprise 4.8%, the first month of 2026 has proven that the momentum is far from a fluke. Between record-breaking stock market performance and massive industrial investments, the “Little Red Dot” is making a very big noise.

-

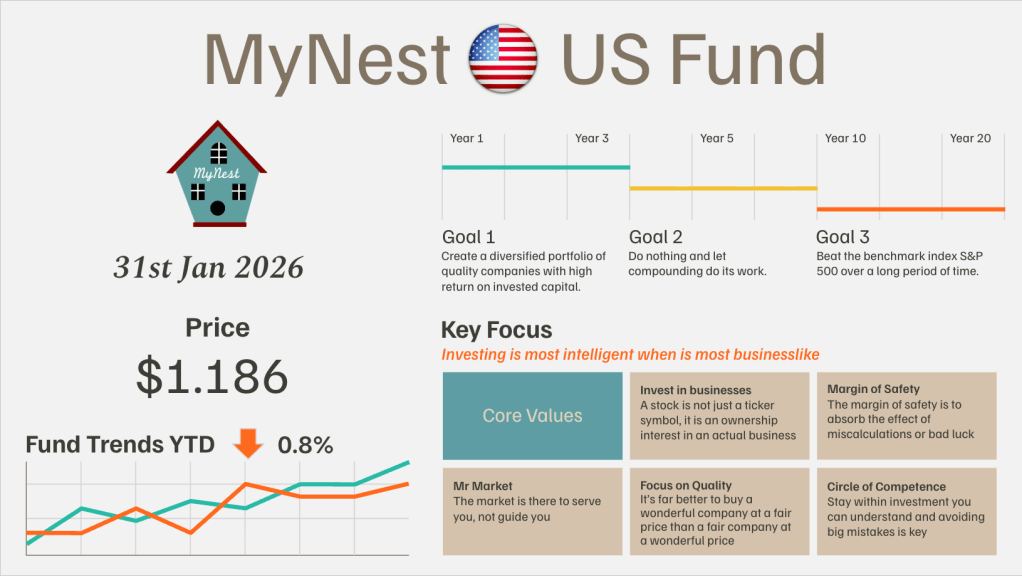

MyNest US Fund Jan 26

I have a confession to make. After reading Chip War at the end of 2022, I fully grasped the strategic importance of TSMC and ASML in the global semiconductor supply chain.

-

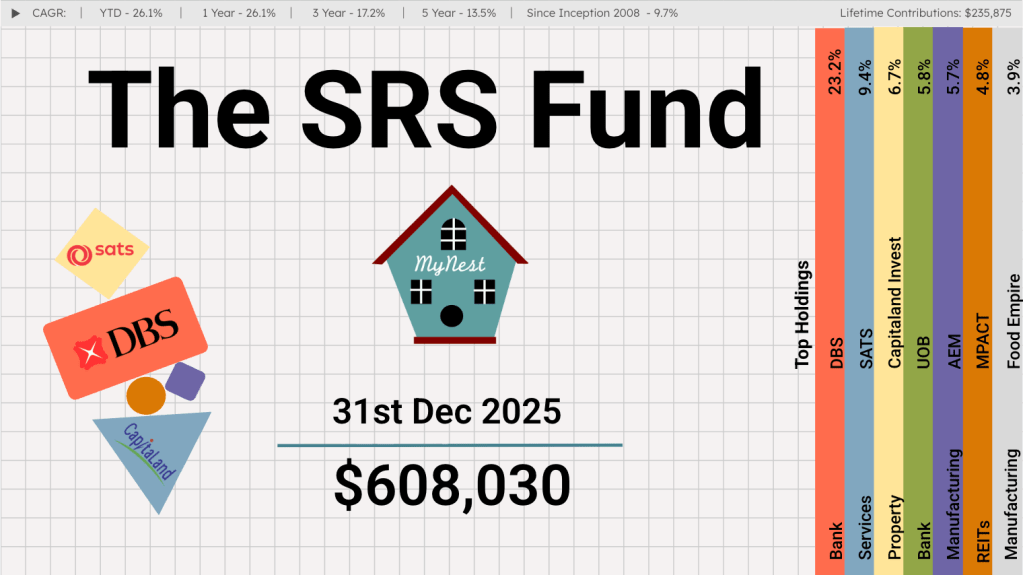

The SRS Fund Dec 2025

If someone had told me at the start of the year that the Singapore stock market would deliver returns in excess of 20%, I would have shrugged it off as wishful thinking.

-

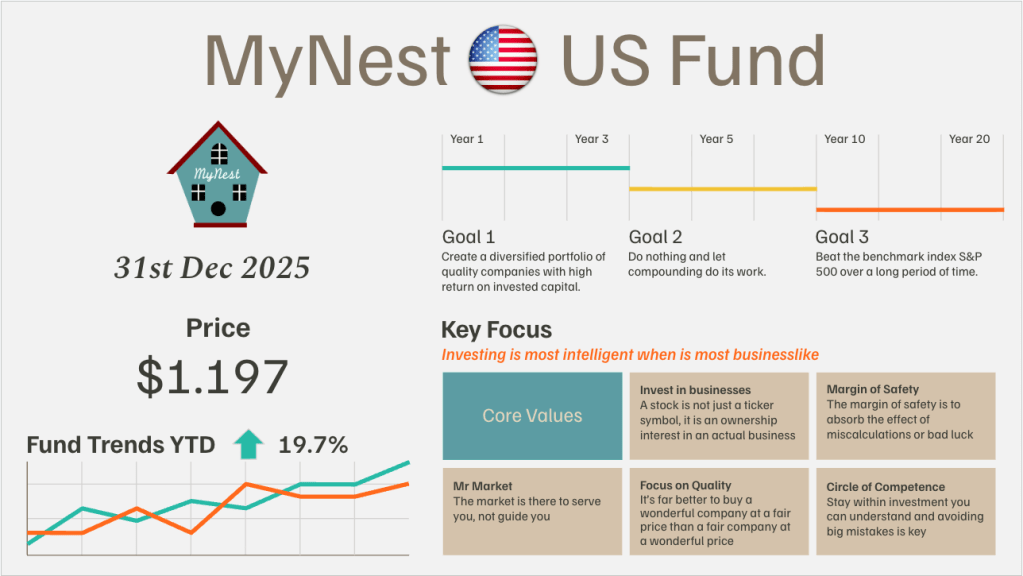

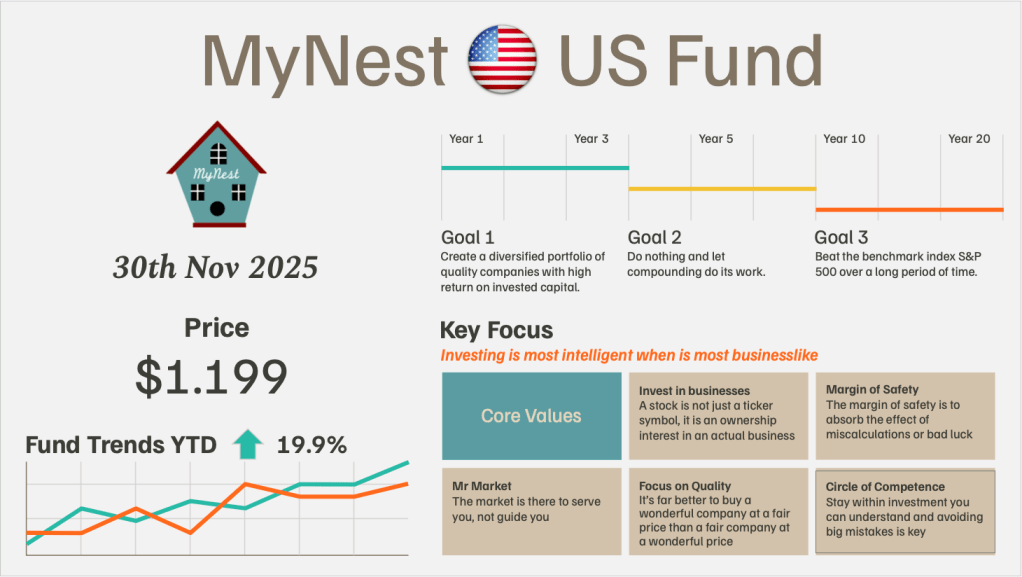

MyNest US Fund Dec 25

MyNest US Fund rounded the first year of inception with a slight outperformance to our benchmark the S&P 500. The first year of operation tested to resolve in knowing what we own as we navigated volatility which started on Trump’s Liberation Day.

-

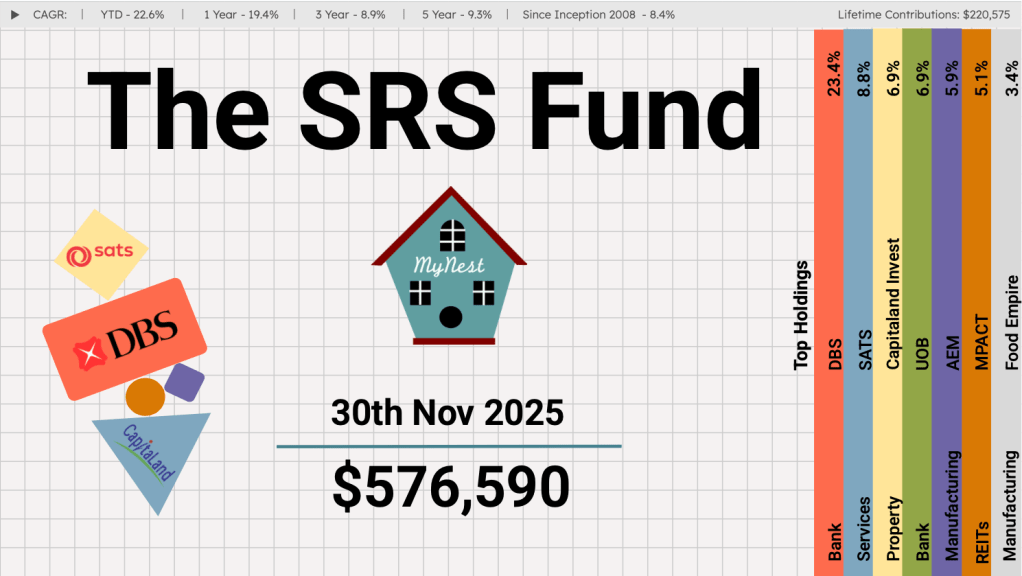

The SRS Fund Nov 2025

If you’ve been watching the Singapore market this past month, the narrative has been impossible to ignore: it is a tale of three banks, and unfortunately for UOB, it has found itself lagging its peers.

-

MyNest US Fund Nov 25

November tested the patience of the broader market, defined by a distinct shift in sentiment regarding Artificial Intelligence. The narrative of an “AI Bubble” finally took hold,