Two sure things one cannot avoid in life, Death & Taxes. While avoiding both remains futile, we can try to live a longer life and pay less taxes.

The SRS now allows for contributions of up to $15,300 for annual tax relief. However, 50% of SRS withdrawal is also taxed at the then prevailing tax rate. One might wonder if they should contribute to SRS now just to be taxed eventually upon withdrawal.

In 2022 I made a decision to cease SRS contributions mainly because I wanted to avoid being taxed upon withdrawal. However, it was dumb of me to do so and I will explain why.

The question one really should ask is whether the Current Tax Savings are MORE THAN the future tax incurred.

The short answer to the question is a firm YES.

It is only in extreme scenarios one can be worse off that is pay more tax eventually upon withdrawal than saved.

According to the equation, the future tax rate MUST BE DOUBLE of the current tax savings to negate any eventual tax savings.

Let’s use the example below to illustrate the case

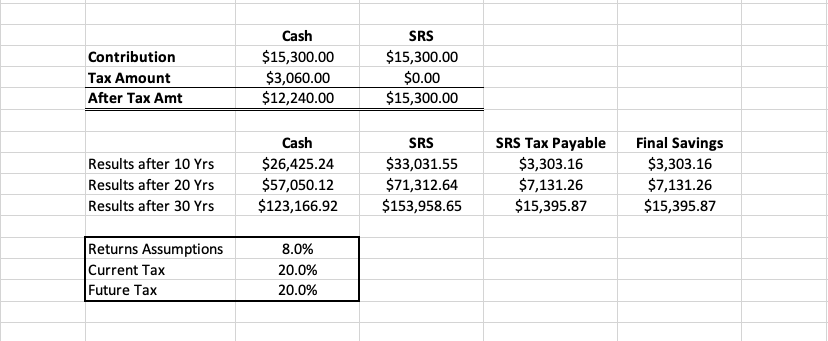

In the table above I made a comparison of using $15,300 of cash less tax versus contributing $15,300 directly into SRS. In the box below the table are my return assumptions, current and future tax rate of 20%.

The table shows the results after 10, 20 & 30 years of cash and SRS. It also shows the SRS tax payable and final savings after each period. As one can see if current and future tax rate remains the same there will be tax savings for SRS contributions.

If one is to assume the future tax rate to be lower due to less income during the withdrawal years the final tax savings will be even more.

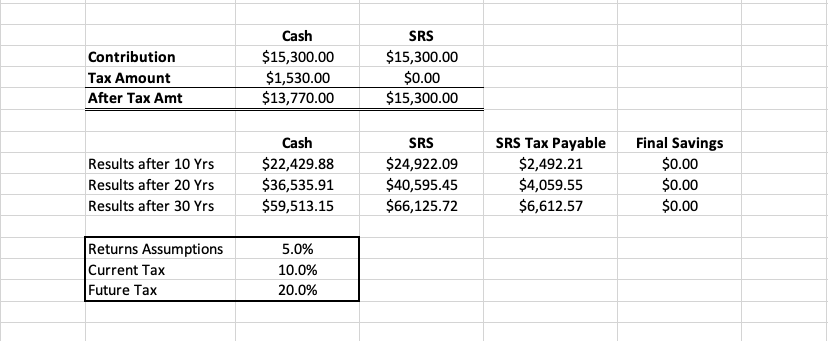

In the next example, we assume the future tax rate is to be double the current one with a different set of return assumptions and tax rate.

We can see from the table above that no matter the return assumptions when the future tax rate moves closer to DOUBLE the current tax rate, the tax savings will trend toward zero.

In conclusion, investors can be assured of having tax savings in the most common scenarios. While there is no assurance that future tax brackets may not double, I believe the event would be highly unlikely and the SRS scheme will remain valid as a tax/retirement planning tool.

-

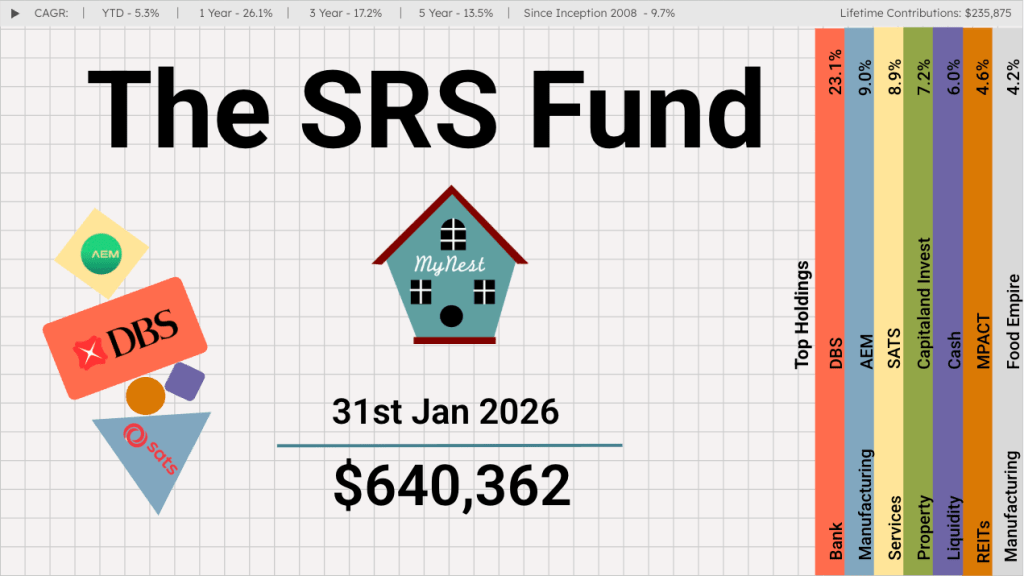

The SRS Fund Jan 2026

After a blockbuster 2025 that saw GDP growth hit a surprise 4.8%, the first month of 2026 has proven that the momentum is far from a fluke. Between record-breaking stock market performance and massive industrial investments, the “Little Red Dot” is making a very big noise.

-

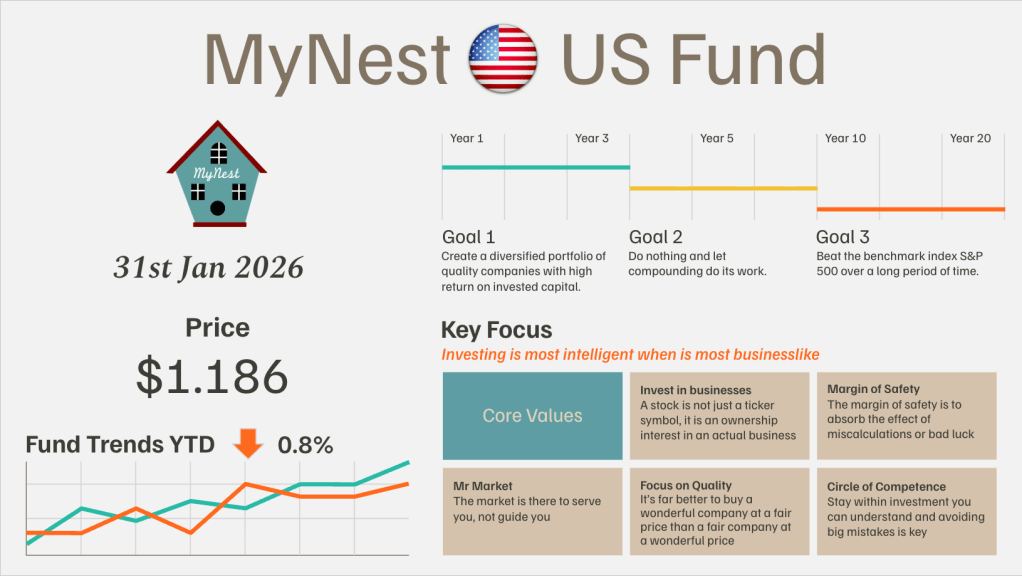

MyNest US Fund Jan 26

I have a confession to make. After reading Chip War at the end of 2022, I fully grasped the strategic importance of TSMC and ASML in the global semiconductor supply chain.

-

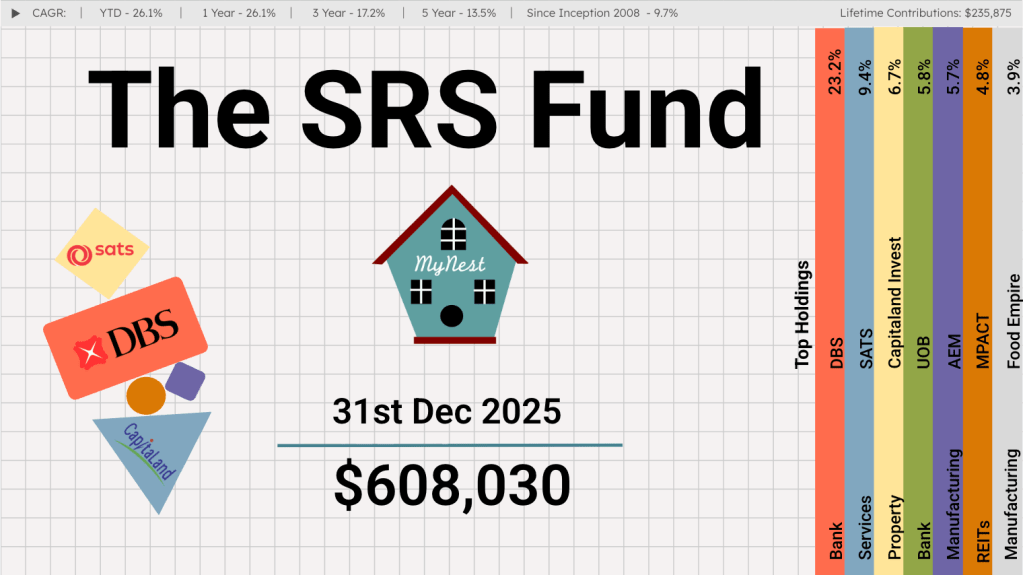

The SRS Fund Dec 2025

If someone had told me at the start of the year that the Singapore stock market would deliver returns in excess of 20%, I would have shrugged it off as wishful thinking.

-

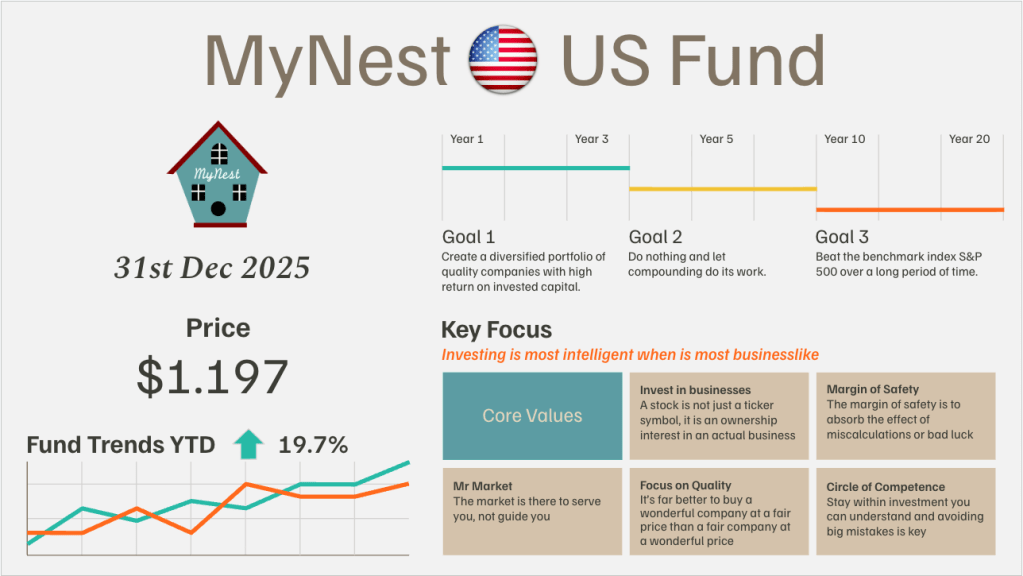

MyNest US Fund Dec 25

MyNest US Fund rounded the first year of inception with a slight outperformance to our benchmark the S&P 500. The first year of operation tested to resolve in knowing what we own as we navigated volatility which started on Trump’s Liberation Day.

-

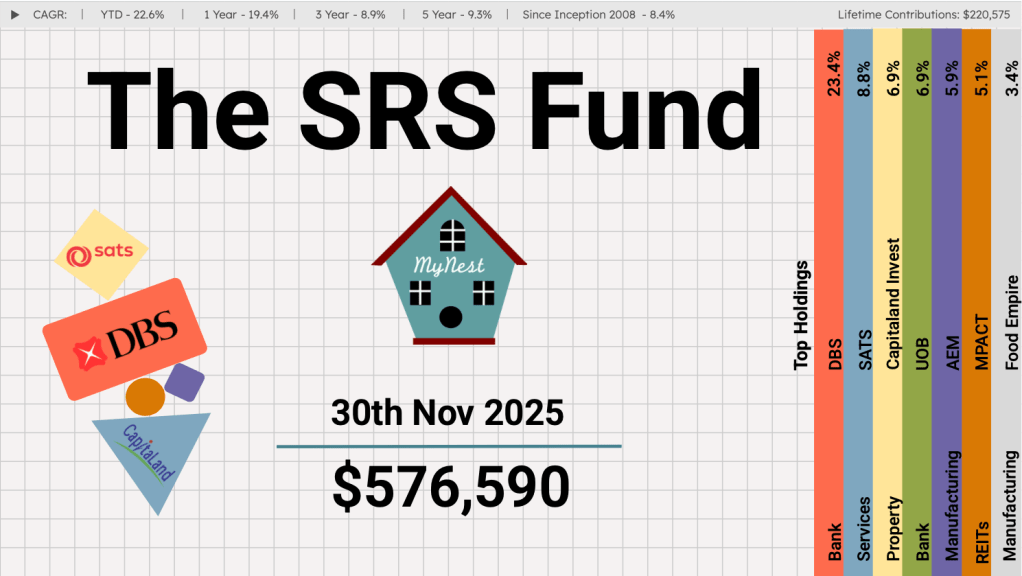

The SRS Fund Nov 2025

If you’ve been watching the Singapore market this past month, the narrative has been impossible to ignore: it is a tale of three banks, and unfortunately for UOB, it has found itself lagging its peers.

-

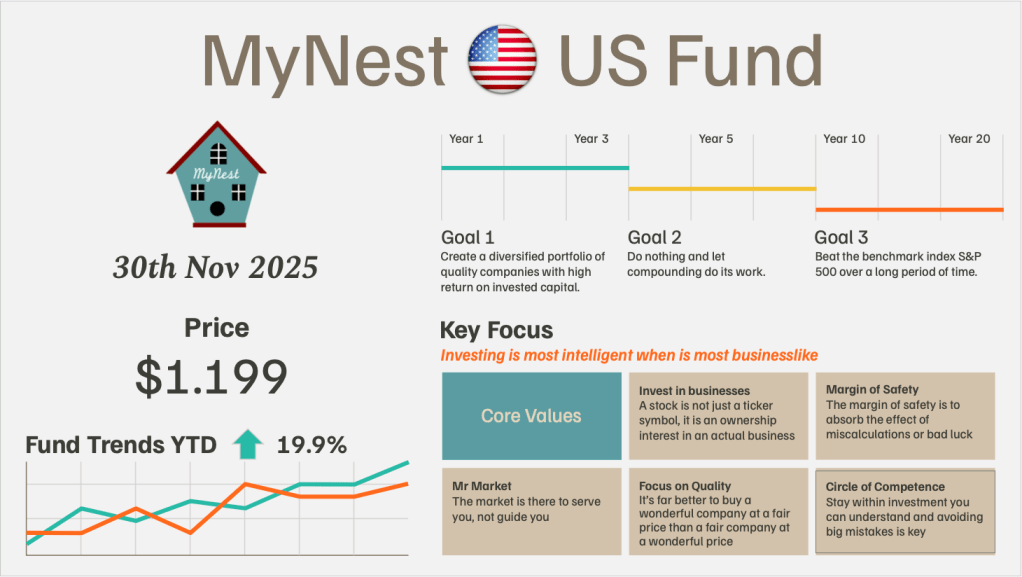

MyNest US Fund Nov 25

November tested the patience of the broader market, defined by a distinct shift in sentiment regarding Artificial Intelligence. The narrative of an “AI Bubble” finally took hold,