Dear Investors,

November tested the patience of the broader market, defined by a distinct shift in sentiment regarding Artificial Intelligence. The narrative of an “AI Bubble” finally took hold, punishing companies in the AI-related space as investors scrutinised massive capital expenditures with renewed skepticism. The S&P 500 largely moved sideways, weighed down by this specific tech weakness.

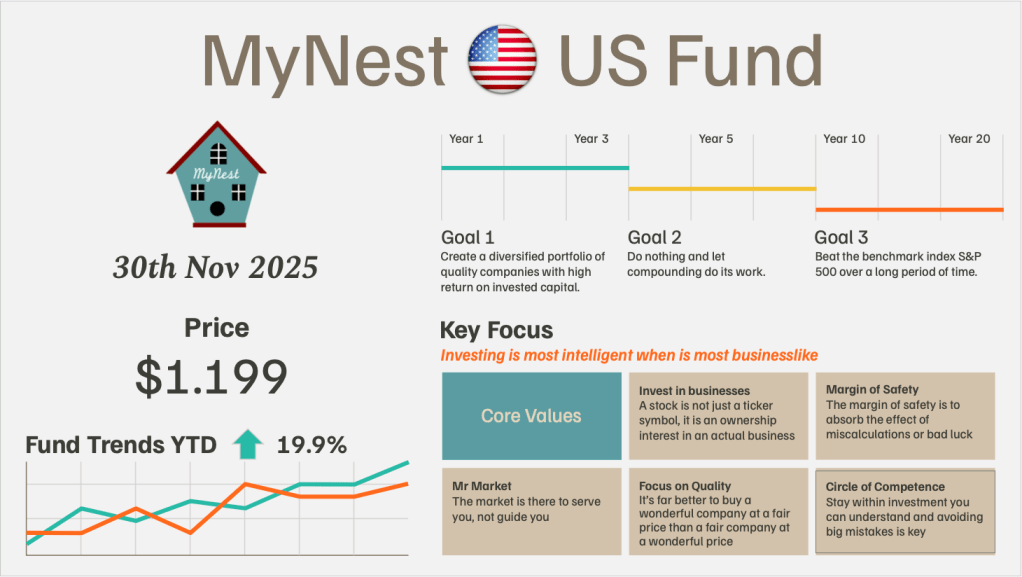

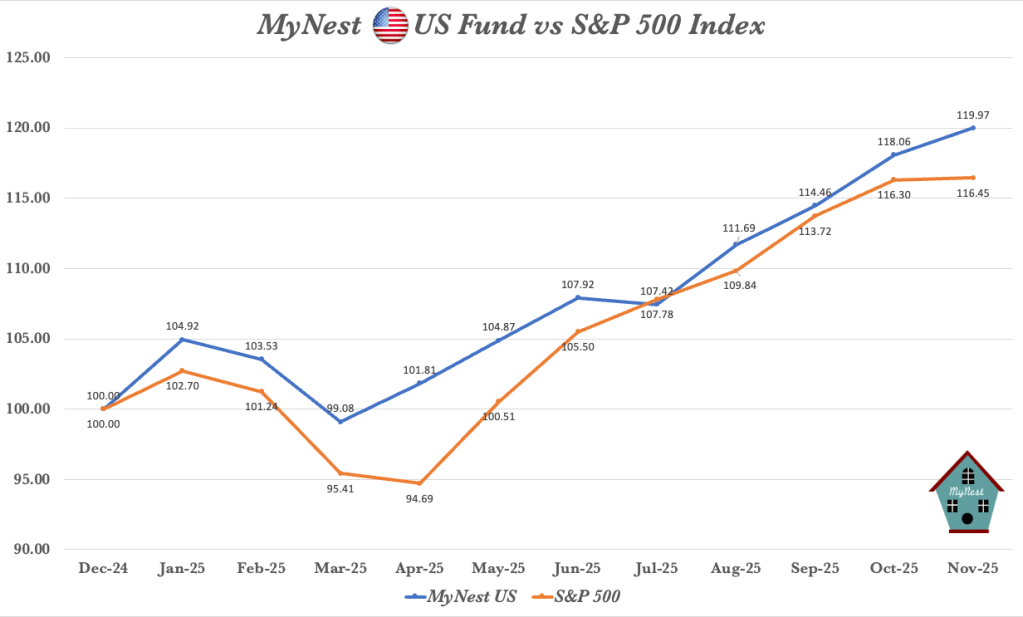

However, for the MyNest US Fund, it was a breakout month. As you can see in the performance charts below, we have officially decoupled from the benchmark, ending the month at a unit price of $1.199.

While our diversified “nest” of insurance, transport and financials played their defensive roles perfectly, the offensive power came from a single familiar name that woke up in a big way this month.

Alpha by Alphabet

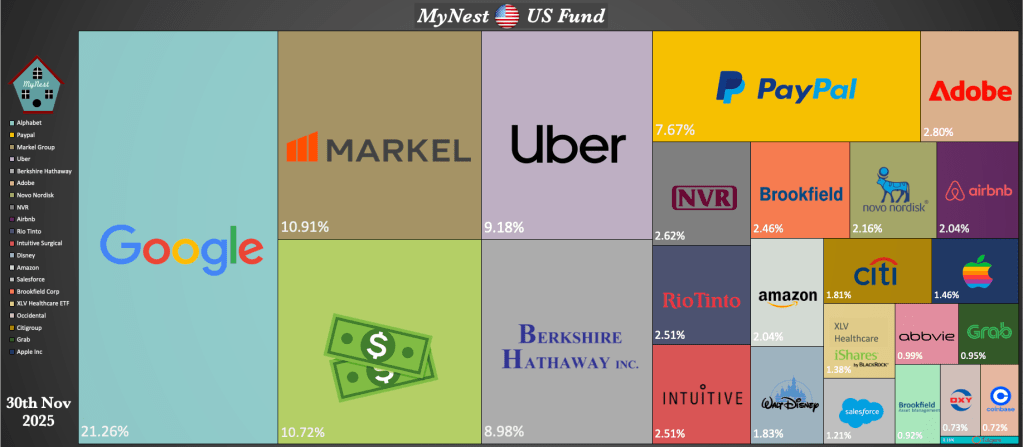

The headline story for November – and the primary driver of our outperformance – is Alphabet (Google), which now constitutes 21.27% of our total portfolio.

For the better part of 2024 and early 2025, holding Google felt like an exercise in contrarian patience. The market narrative was relentless: Google was a legacy giant, too slow to dance, seemingly “falling behind” in the AI arms race it helped invent. While competitors grabbed the headlines, we held our position, grounded in the conviction that their proprietary data advantages – Search, YouTube, Android – were unassailable moats that just needed the right spark.

In November, the sleeping giant didn’t just wake up. Mother Google slipped into her ballerina shoes and started dancing, moving with a precision and grace that left the rest of the industry stumbling to keep up.

The turning point was the launch of Gemini 3. This wasn’t merely a product update; it was a statement of infrastructure dominance. When early benchmarks showed Gemini outperforming GPT-5 in critical reasoning and coding tasks, the market was forced to rerate Google from a “participant” to the “platform”

But for the business-minded investor, the most exciting development was happening quietly in the background. As competitors watched their capital expenditures balloon on third-party hardware, Alphabet demonstrated the power of vertical integration. The confirmation that they are successfully shifting the bulk of their AI workloads to custom Tensor Processing Units (TPUs) effectively decouples their destiny from external chip suppliers. They are protecting margins where others are sacrificing them.

Finally, just as the technical thesis was proving itself, the value thesis received the ultimate seal of approval. The mid-month revelation that Berkshire Hathaway had built a stake in Alphabet acted as a massive signal flare. It confirmed what we had suspected all along: the tech giant had entered rare “value” territory relative to its growth.

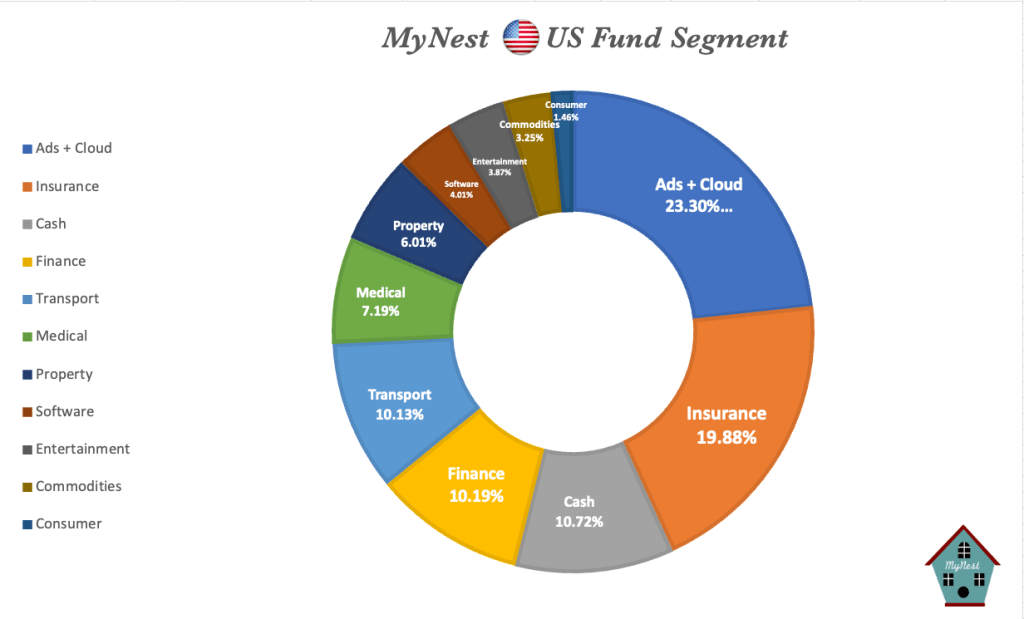

With 23.3% of our fund allocated to the advertising and cloud segment, we are perfectly positioned to capture the upside of AI. When a compounder of this quality finds a new gear, the best thing to do is some thumbsucking and enjoy the ride.

MyNest US Fund Portfolio Compositions

Outside of our tech alpha, the portfolio remains robustly defensive, designed to let us sleep well even if the tech rally fades.

- Insurance (19.8%) : Our second largest segment led by Markel and Berkshire Hathaway, continues to provide the steady float that underpins our strategy. Markel, often called “Baby Berkshire”, remains a quiet compounder in the background.

- Uber & The Gig Economy (9.1%) : Uber remains a top 5 holding. Their continued dominance in mobility and delivery logistics is turning them into a utility-like staple in our Transport segment.

- The Cash Buffer (10.7%) : We are carrying a healthy cash position. While some might call this a drag in a rising market, we view it as optionality. With the unit price at nearly $1.20, we have dry powder ready for any volatility the future may bring.

MyNest US Fund Performance

Looking at the trends YTD, we are up 19.9%, significatly widening the gap against the S&P 500.

We remain focused on our three core goals:

- Diversify into quality companies with high returns on capital

- Do nothing and let compounding work

- Beat the benchmark over the long haul

As we head into the final month of 2025, we will continue to stick to our Circle of Competence and, at the same time, also expanding it. We aren’t chasing the next hot trend; we are owning the businesses that build the future’s infrastructure.

Segment Chart

-

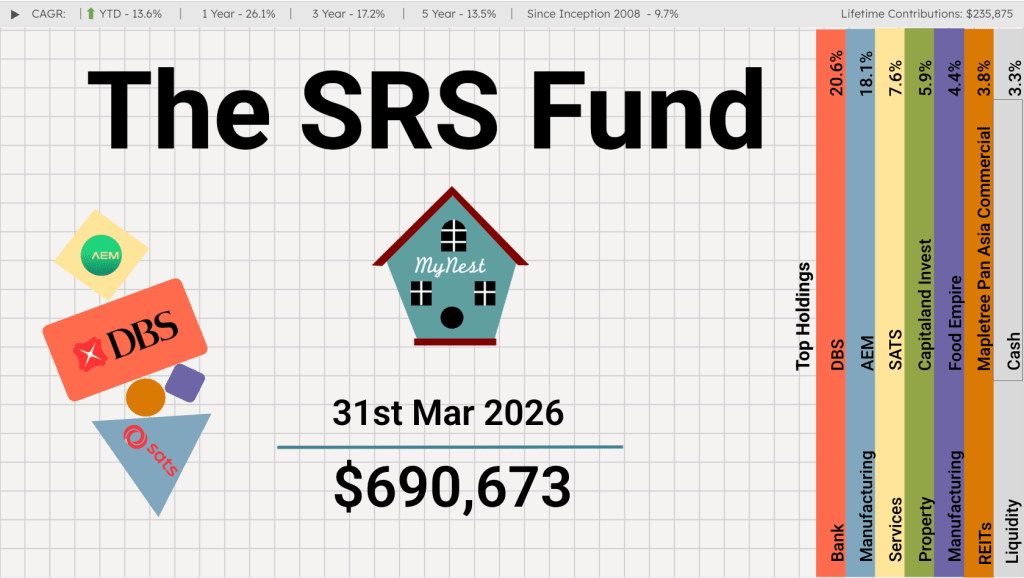

The SRS Fund Mar 2026

It is an enduring market reality that a concentrated minority of holdings drives the vast majority of returns. For years, DBS (currently the largest individual holding at 20.6%) has served as the compounding engine of the SRS Fund.

-

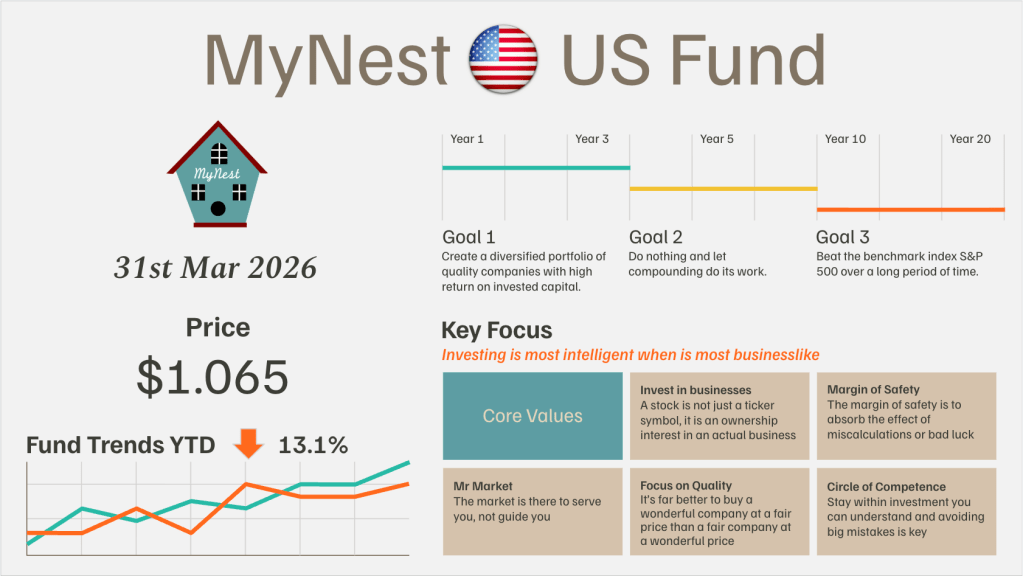

MyNest US Fund Mar 26

March shattered any lingering market complacency, pivoting sharply from the localized damage of the “SaaS-pocalypse” to a systemic shock driven by the war in Iran.

-

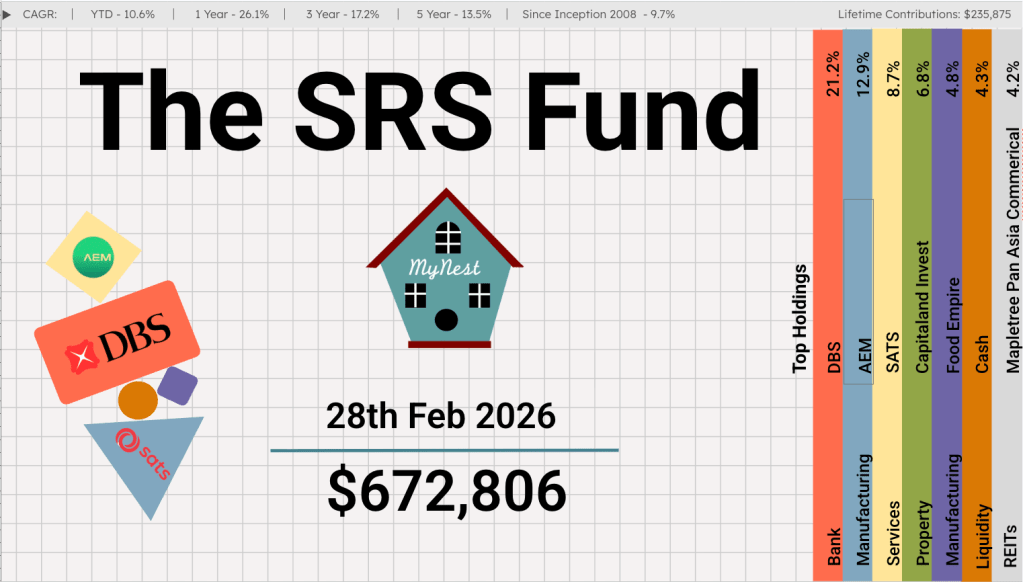

The SRS Fund Feb 2026

The Singapore Budget 2026 has set a robust backdrop for local investors. For the third consecutive year, the government is operating from a position of immense “dry powder,” with an overall fiscal surplus of $8.5 billion projected for FY2026.

-

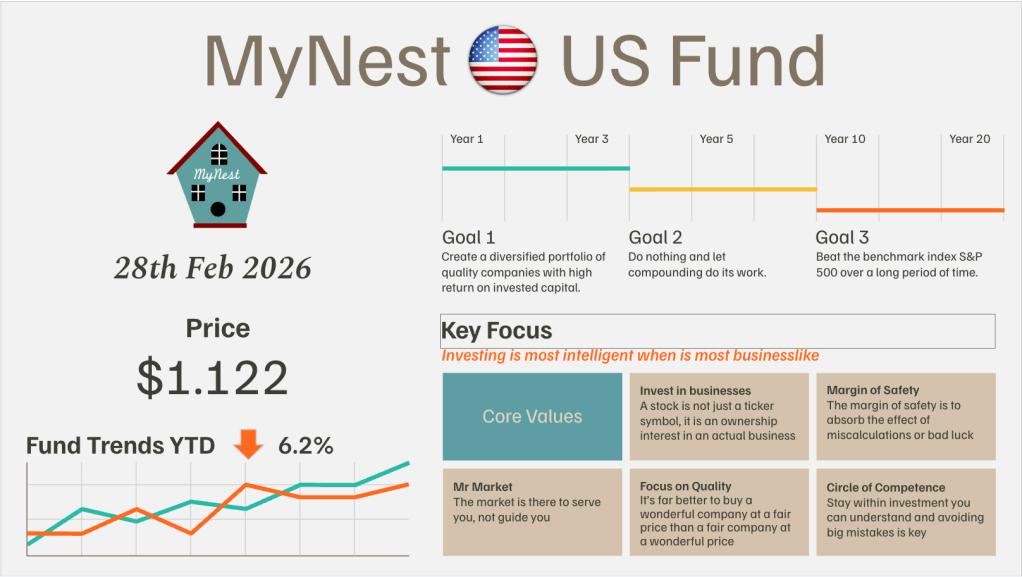

MyNest US Fund Feb 26

February 2026 proved to be one of the most challenging months for our fund since its inception. A wave of “AI anxiety” swept through the Software-as-a-Service (SaaS) sector

-

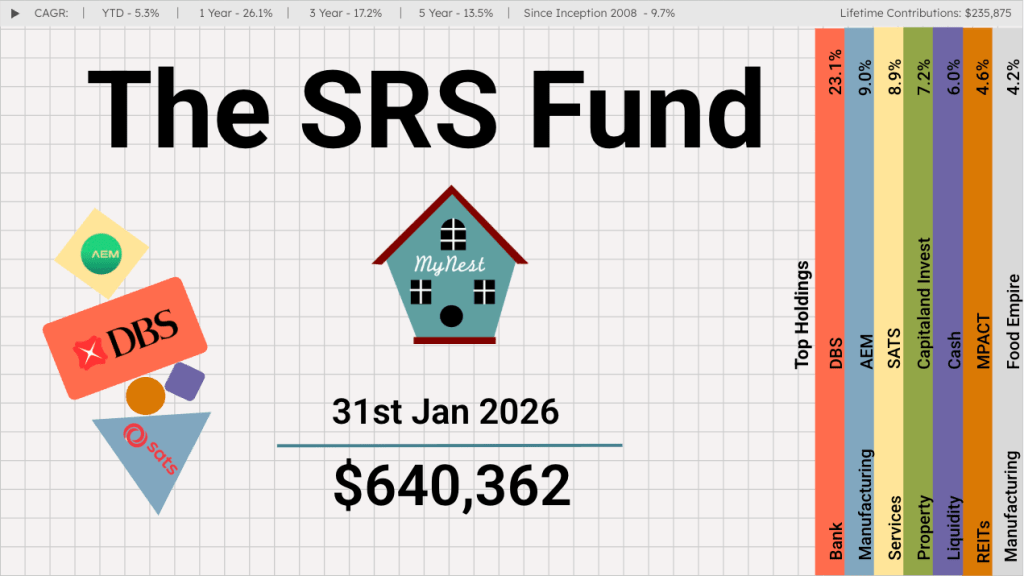

The SRS Fund Jan 2026

After a blockbuster 2025 that saw GDP growth hit a surprise 4.8%, the first month of 2026 has proven that the momentum is far from a fluke. Between record-breaking stock market performance and massive industrial investments, the “Little Red Dot” is making a very big noise.

-

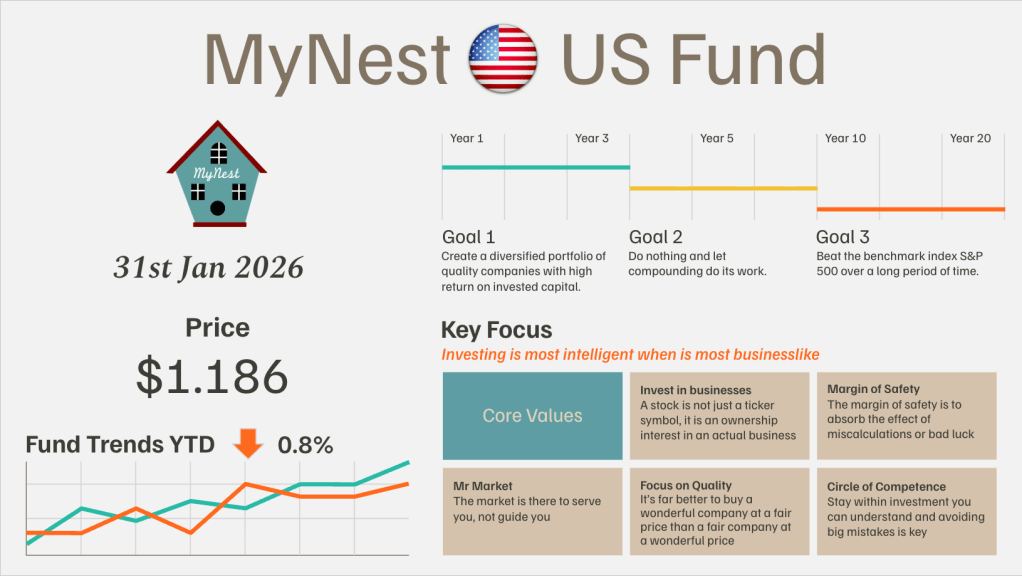

MyNest US Fund Jan 26

I have a confession to make. After reading Chip War at the end of 2022, I fully grasped the strategic importance of TSMC and ASML in the global semiconductor supply chain.