A Tale of the Three Banks Earnings

If you’ve been watching the Singapore market this past month, the narrative has been impossible to ignore: it is a tale of three banks, and unfortunately for UOB, it has found itself lagging its peers.

The main theme of the month’s SRS Fund update is the strategic reduction of my UOB position. Following a quarterly result that was the softest of the trio, UOB shares have experienced some weakness while DBS and OCBC continued to perform strongly

Consequently, I made the decision to reduce the SRS Fund’s UOB holding by 50%, rotating the proceeds into a high-conviction tech turnaround play: AEM Holdings.

The UOB Weakness: Why I Trimmed the Position

The market response to UOB’s earnings has been tepid, and given the comparative strength of its peers, I felt it was prudent to reallocate capital.

First, there was the loss provision. While its rivals are basking in clean balance sheets and holding reserves steady, UOB provided significant provisions in its earnings. While this may be a prudent move by management, the immediate market reaction has been negative, resulting in share price weakness that cannot be ignored.

Second, and perhaps more concerning, is the wealth management divergence. In a golden era for Asian wealth management, UOB’s income from this segment failed to grow as strongly as its rivals. Compared to the double-digit momentum seen in DBS, UOB’s growth looked more modest.

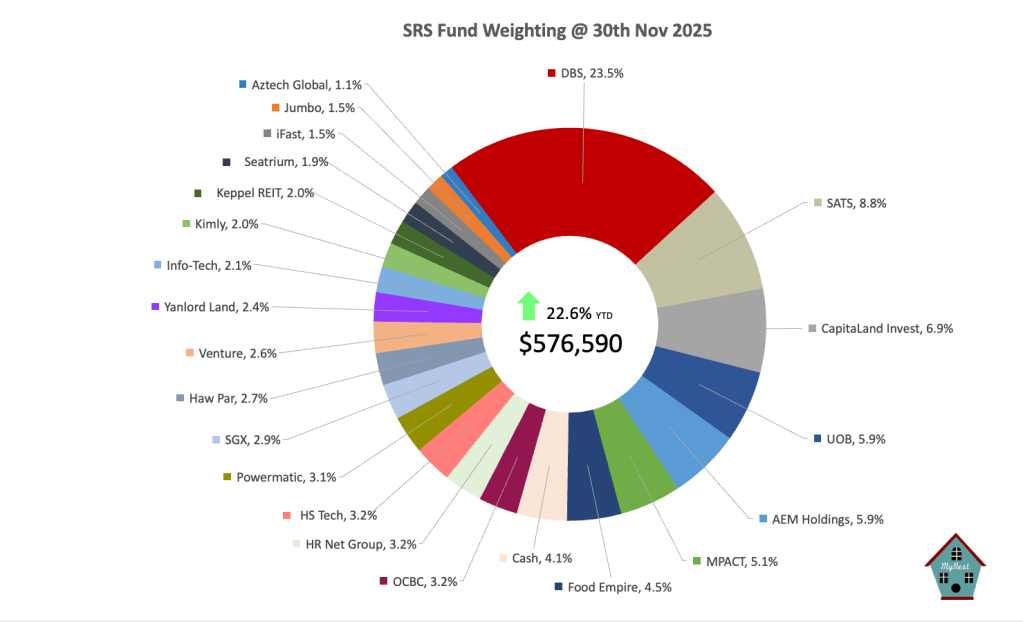

As a result, I have reduced the SRS Fund’s allocation to 5.9% effectively halving the fund’s exposure to manage opportunity cost while still retaining a position for potential longer-term recovery.

The Pivot: Doubling Down on AEM (5.9%)

The funds released from the UOB sale were immediately redeployed into AEM Holdings, bringing its weight in the portfolio to 5.9% – now equal to the UOB stake.

Why AEM? The thesis is to capitalise on two converging tailwinds:

- The Intel Turnaround : AEM’s fortunes have long been tied to its key customer, Intel. With Intel’s aggressive cost-cutting and strategic pivot finally gaining traction in 2025, there are definately green shoots of a genuine turnaround with its Malaysian new CEO. As Intel stabilises, AEM stabilises.

- Massive AI Chip Order Volume: The demand for testing services is skyrocketing, driven by the increasing volume of next-generation AI chips entering the market. AEM’s test handlers are critical for these complex, high-performance chips. The company recently reported a 16% rise in Q3 revenue and a staggering 592% jump in profit before tax, proving that the “AI/HPC ramp” is not just a buzzword but is showing up in the bottom line.

Portfolio Resilience: The “DBS Shield”

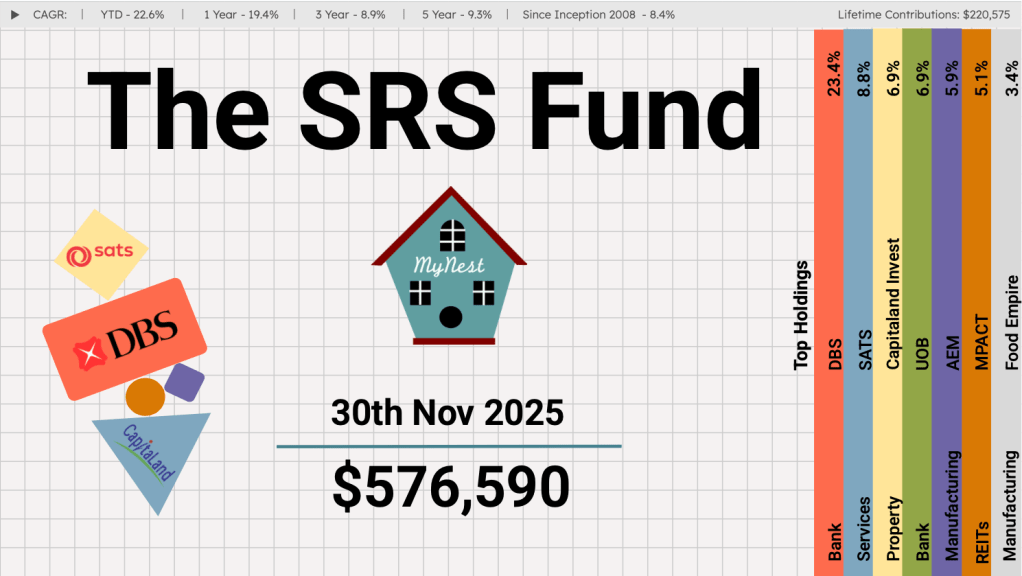

Despite the weakness in UOB, I am pleased to report that the SRS Fund is up 22.6% YTD, hitting a fresh high of $576,590.

The Heavyweight Hero (DBS @ 23.5%). As shown in the chart above, my conviction in DBS has paid off. At 23.5% of the portfolio, DBS is doing the heavy lifting. Its earnings beat and dominant wealth management franchise have effectively acted as a shield, buffering the portfolio against the UOB dip.

Portfolio Segments

With the trimming of UOB, the SRS Fund has reduced its focus on the finance sector from 43% to 37.1%. Reducing exposure to the finance segment also gives the SRS Fund a more balanced concentration, diversifying risk.

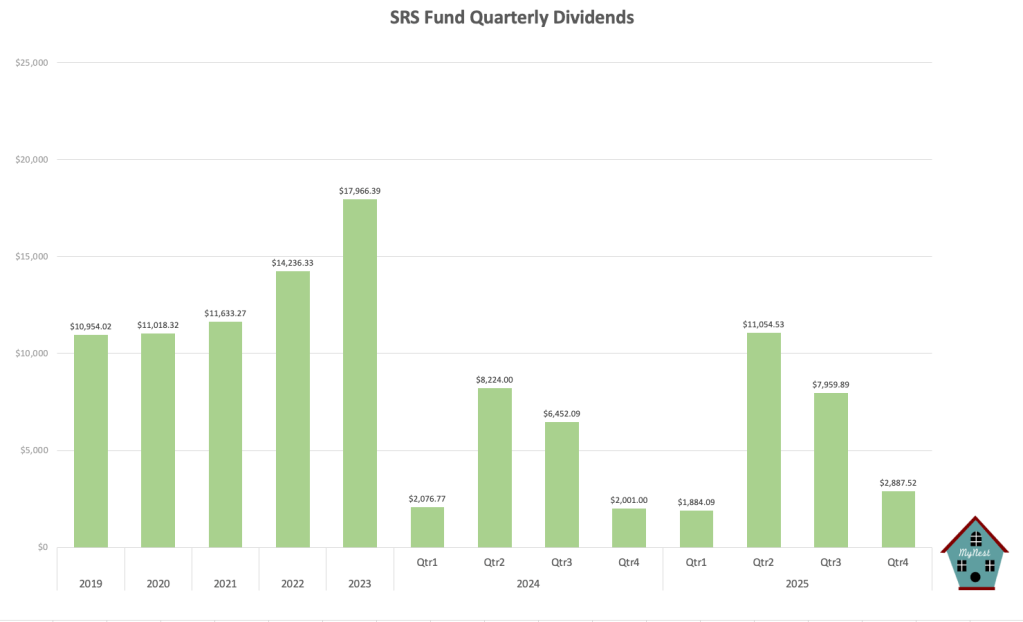

Dividends

Q4 is off to a quiter start on the dividend front with $2,887.52 worth of collection compared to the massive Q2 & Q3 payout saw earlier in the year. This seasonality is expected, but the steady flow of income continues to anchor total return.

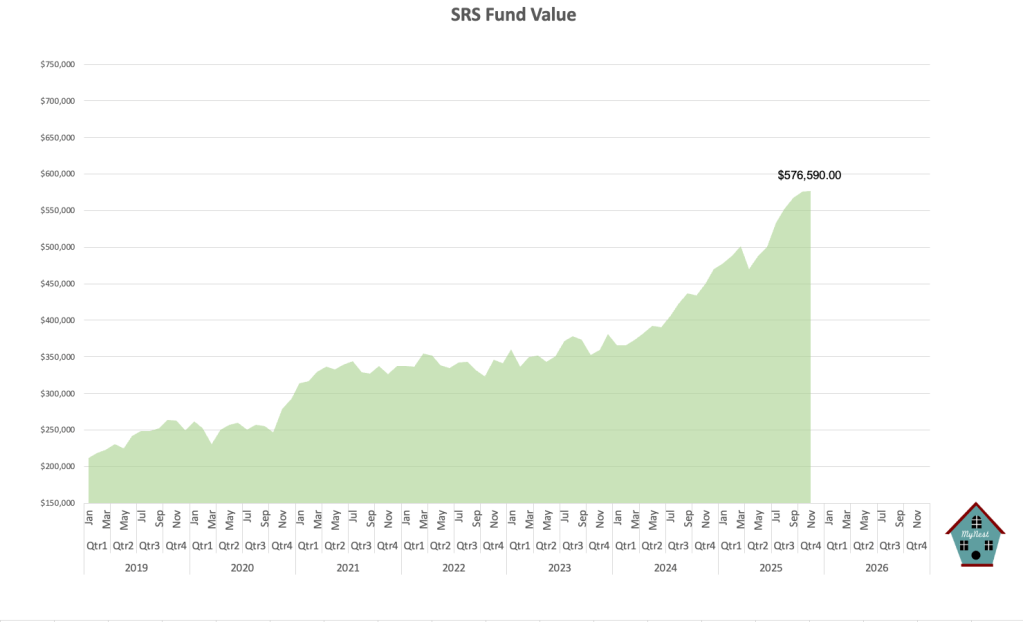

SRS Fund Value

Total SRS Fund value hit another record high at $576,590. I wouldn’t write off the $600k mark just yet with still another month to go and pending this year contributions.

Cash Levels

With the proceeds from the selling of UOB shares cash level now stands at 4.1% allowing me to add to any opportunities that arise in the following few months.

Summary

The trimming of UOB was a necessary rotation as I aim to keep the SRS Fund’s capital working efficiently. By halving the UOB position and rotating into AEM, I have swapped a slower-moving bank allocation for a recovery tech play with a strong AI tailwind.

-

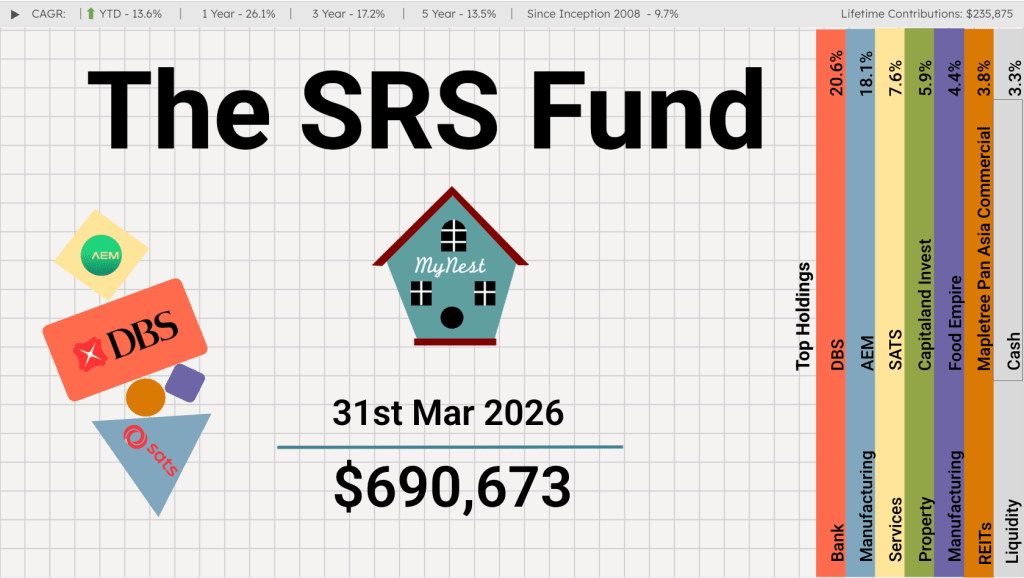

The SRS Fund Mar 2026

It is an enduring market reality that a concentrated minority of holdings drives the vast majority of returns. For years, DBS (currently the largest individual holding at 20.6%) has served as the compounding engine of the SRS Fund.

-

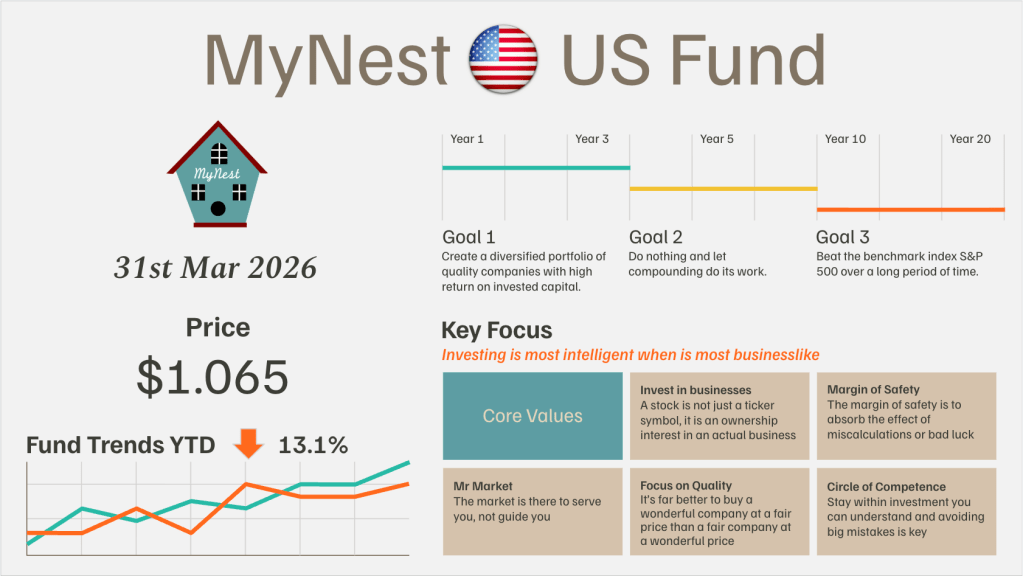

MyNest US Fund Mar 26

March shattered any lingering market complacency, pivoting sharply from the localized damage of the “SaaS-pocalypse” to a systemic shock driven by the war in Iran.

-

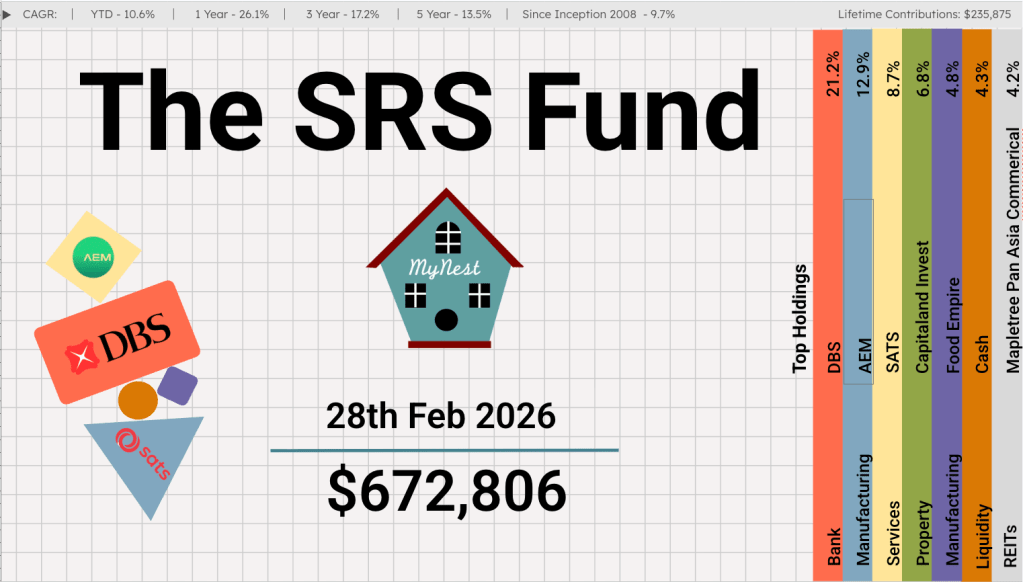

The SRS Fund Feb 2026

The Singapore Budget 2026 has set a robust backdrop for local investors. For the third consecutive year, the government is operating from a position of immense “dry powder,” with an overall fiscal surplus of $8.5 billion projected for FY2026.

-

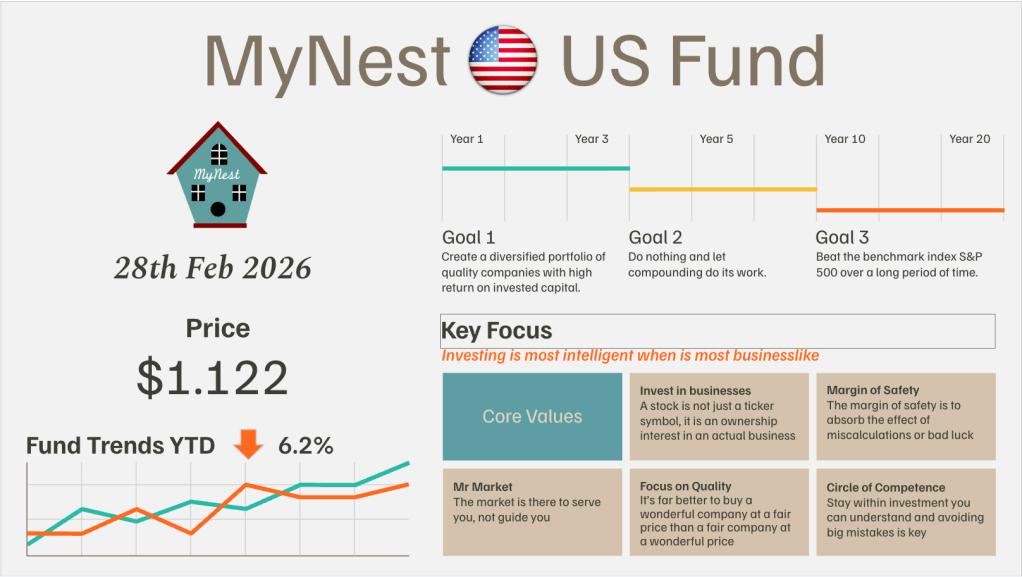

MyNest US Fund Feb 26

February 2026 proved to be one of the most challenging months for our fund since its inception. A wave of “AI anxiety” swept through the Software-as-a-Service (SaaS) sector

-

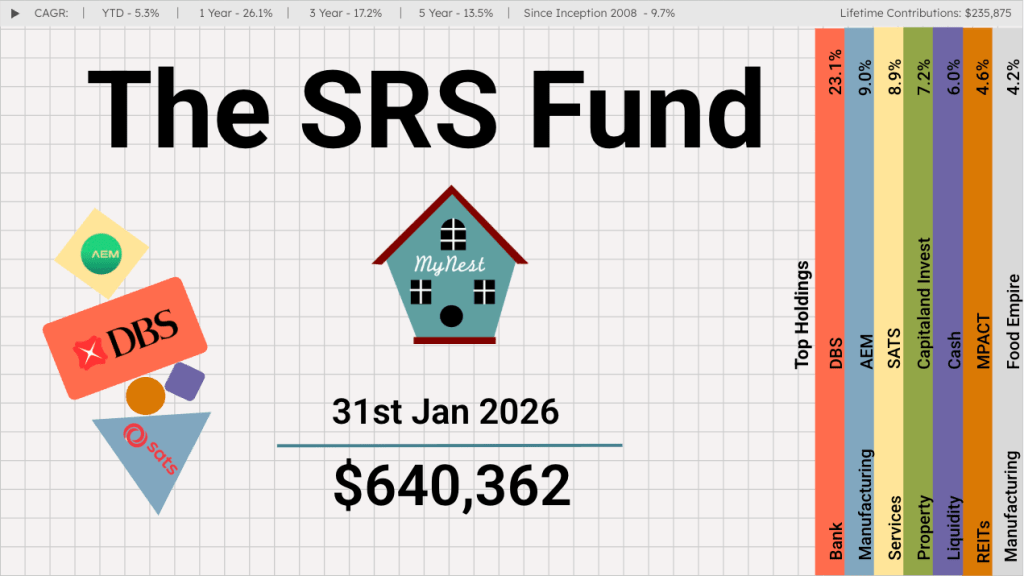

The SRS Fund Jan 2026

After a blockbuster 2025 that saw GDP growth hit a surprise 4.8%, the first month of 2026 has proven that the momentum is far from a fluke. Between record-breaking stock market performance and massive industrial investments, the “Little Red Dot” is making a very big noise.

-

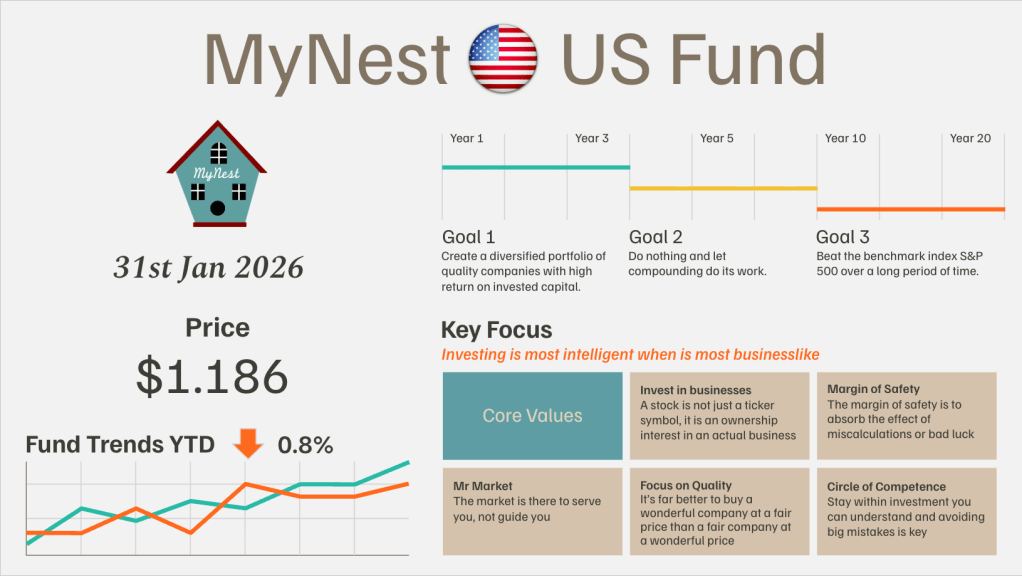

MyNest US Fund Jan 26

I have a confession to make. After reading Chip War at the end of 2022, I fully grasped the strategic importance of TSMC and ASML in the global semiconductor supply chain.