The Return of STI

If someone had told me at the start of the year that the Singapore stock market would deliver returns in excess of 20%, I would have shrugged it off as wishful thinking.

After all, we have not seen such performance since the Global Financial Crisis. Yet 2025 proved the skeptics wrong. The ETF (ES3) tracking the Straits Times Index (STI) delivered a total return of 25.7%, making 2025 – by a wide margin – the best-performing year for the Singapore equity market in the past decade.

This resurgence did not happen by chance. In my view, the strong performance of the STI can be attributed to several structural and cyclical factors coming together at the right time.

1. Government Intent to Build a Strong Equity Market

Singapore has made no secret of its ambition to deepen and strengthen its capital markets. Policies aimed at improving market liquidity, encouraging listings, and enhancing the attractiveness of Singapore as a global financial hub have gradually laid the groundwork for a healthier equity ecosystem. While such initiatives take time to bear fruit, 2025 may well be the year when these efforts began to show tangible results in market performance.

2. Local Investment Requirements for Family Offices

Another meaningful tailwind comes from the growing number of family offices in Singapore and the requirement for them to deploy capital locally. This structural demand provides a steady and relatively sticky source of inflow into Singapore-listed equities, particularly large-cap and dividend paying stocks that dominate the STI. Over time, this creates a more resilient market base and supports valuations.

3. Storng GDP Growth Led by Key Sectors

Singapore’s economic growth has also been broad-based, with construction, finance, and manufacturing leading the charge. These sectors are well represented in the STI, allowing earnings growth to translate directly into index performance. As corporate profitability improved, investor confidence follows.

Looking Ahead to 2026: Momentum Remain Intact

Heading into 2026, the outlook for the Singapore economy remains constructive. The construction sector is once again at the forefront, supported by major infrastructure projects such as Changi Airport Terminal 5, the Marina Bay Sands expansion and new MRT lines. These large scale developments create positive spillover effects across employment, services, and related industries, contributing to a vibrant business environment.

Lower Interest Rates to Supoort SGD Asset Prices

The sharp decline in local interest rates adds another powerful tailwind. Three month SORA has fallen from around 3% to aproximately 1.85%, materially easing financial conditions. Lower borrowing costs are likely to support property prices and keep demand for big-ticket items such as cars resilient.

At the same time, the wealth effect from rising asset prices should help sustain consumer confidence and domestic consumption. With household balance sheets in relatively strong shape, local demand is likely to remain elevated.

Portfolio Milestone and Strategic Progress

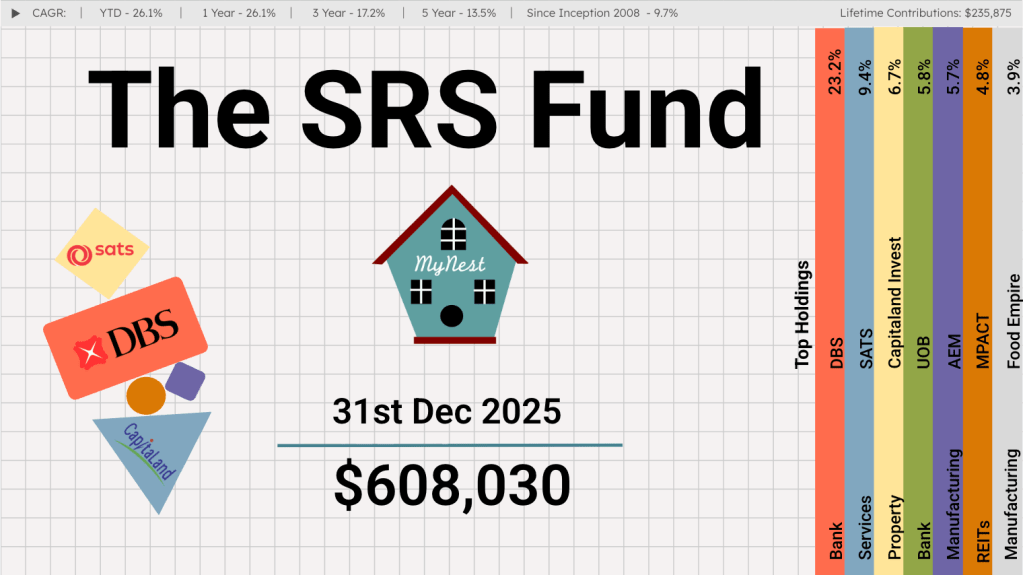

2025 marked a defining year for the SRS Fund, as it crossed the $600k mark for the first time, ending the year at $608,030. This milestone feels particularly meaningful given that the fund had only just overcome the $500k threshold at the start of the year.

In a single year, disciplined positioning and favourable market conditions combined to deliver a 26.1% YTD return, accelerating the fund meaningfully along its long term compounding path

The strong performance in 2025 has also lifted the SRS Fund’s longer term metrics. The 3Y CAGR has risen to 17.2%, while the 5Y CAGR now stands at 13.5%. Since inception, the SRS Fund has compounded at 9.7% per annum over a period of 18 years. A solid outcome for a retirement focused SRS strategy that balances growth with resilience.

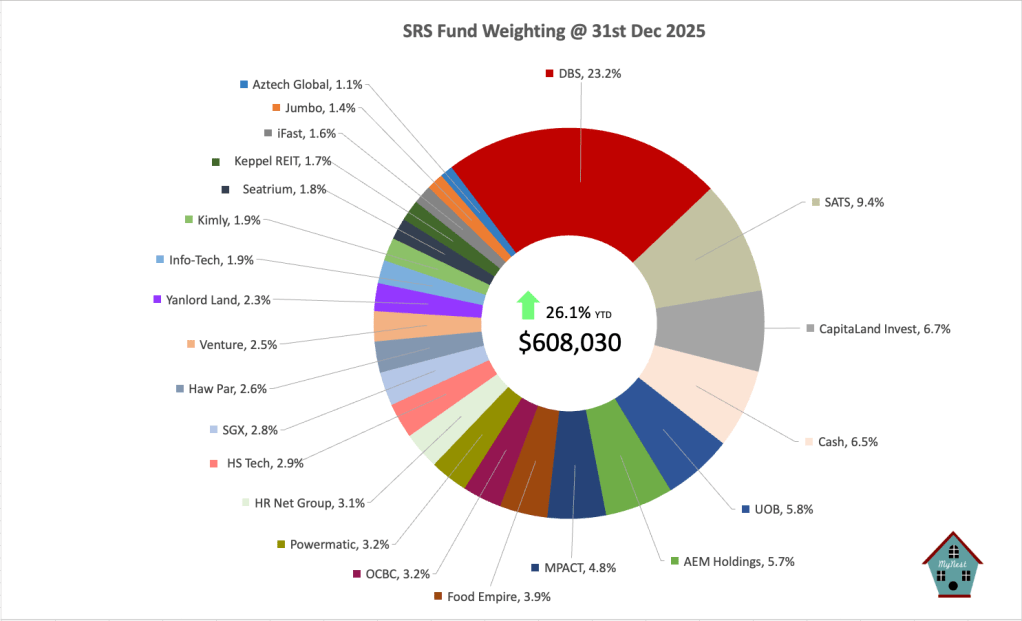

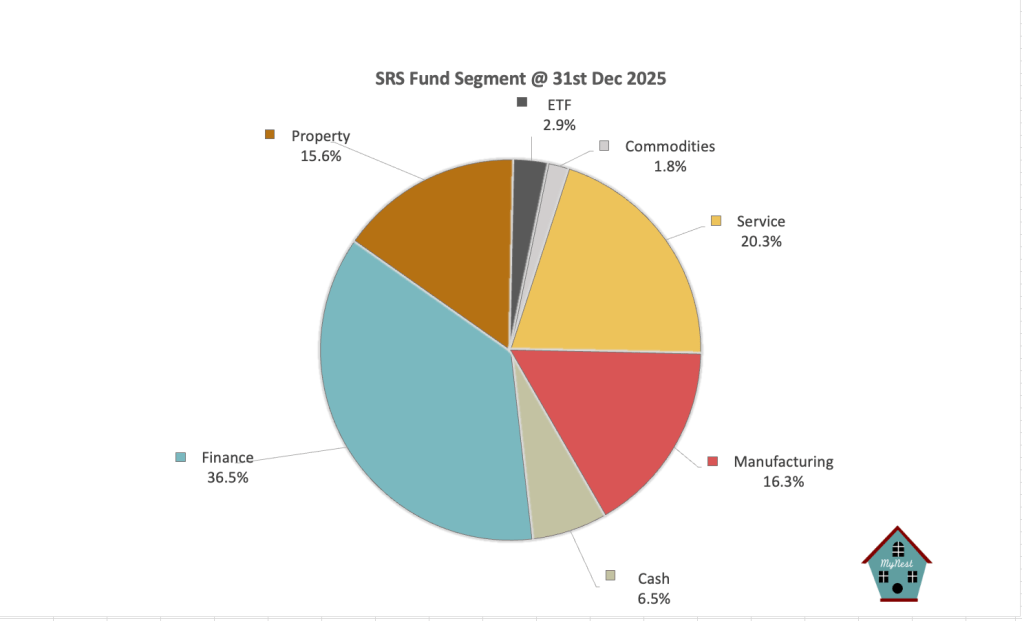

Portfolio Segments

Beyond headline performance, this year also represented an important step forward in portfolio construction. Historically, the SRS Fund carried a heavy bias towards local banking sectors, with DBS, OCBC and UOB forming the core. While banks remain meaningful holdings, deliberate diversification efforts have been made to broaden future growth drivers. Poisition in SATS, CapitaLand Investment and AEM Holdings were built up to complement the financials exposure, adding structural growth, asset management leverage and technology linked upside to the portfolio

Dividends

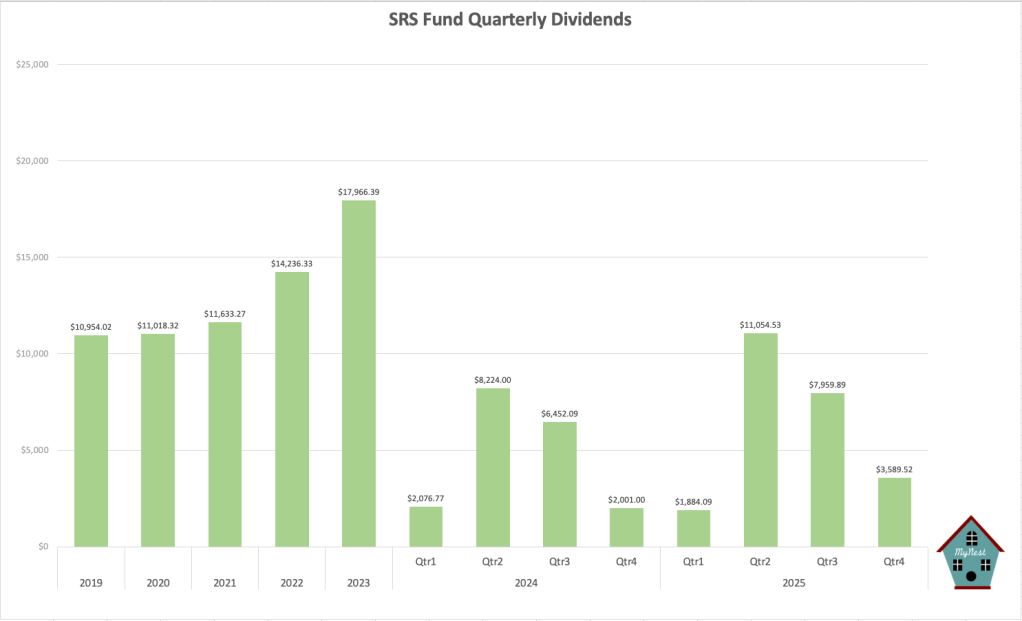

Total dividends received in 2025 amounted to $24,488.03, representing a 30% increase over the $18,753.86 collected in 2024. This step up in income was driven by both the fund’s growth and improved dividend payouts from core holdings

Importantly, annual dividend income now exceeds new cash contributions by a wide margin, marking a meaningful inflection point in the SRS Fund’s journey. At this stage, dividends have become the primary engine of compounding, allowing capital to grow increasingly through internally generated cash flows rather than fresh injections.

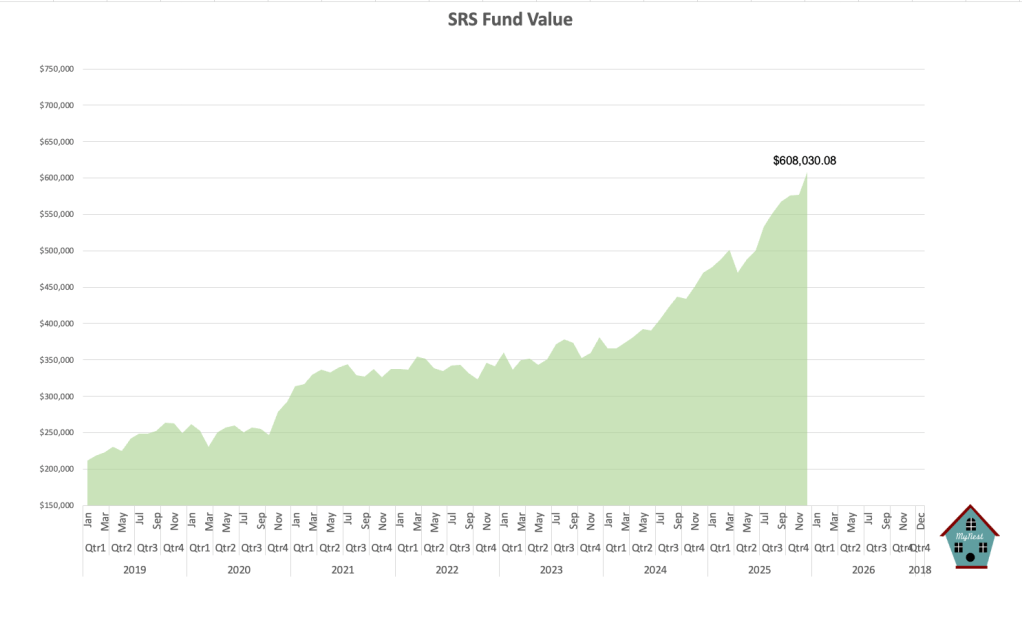

SRS Fund Value

The chart shows the steady long term growth of the SRS Fund, culminating in a year end value of $608,030.08, the highest level reached since inception. After several years of gradual accumulation and consolidation, the SRS Fund entered a strong acceleration phase in 2024 and 2025, reflecting both favourable market conditions and compounding at scale.

A $15,300 contribution was made towards the end of th year, primarily for tax optimisation purposes. While this late contribution provided a modest boost to the headline fund value, the majority of the year’s gain were driven by investment performance rather than fresh capital, underscoring the strenght of returns achieved during the year.

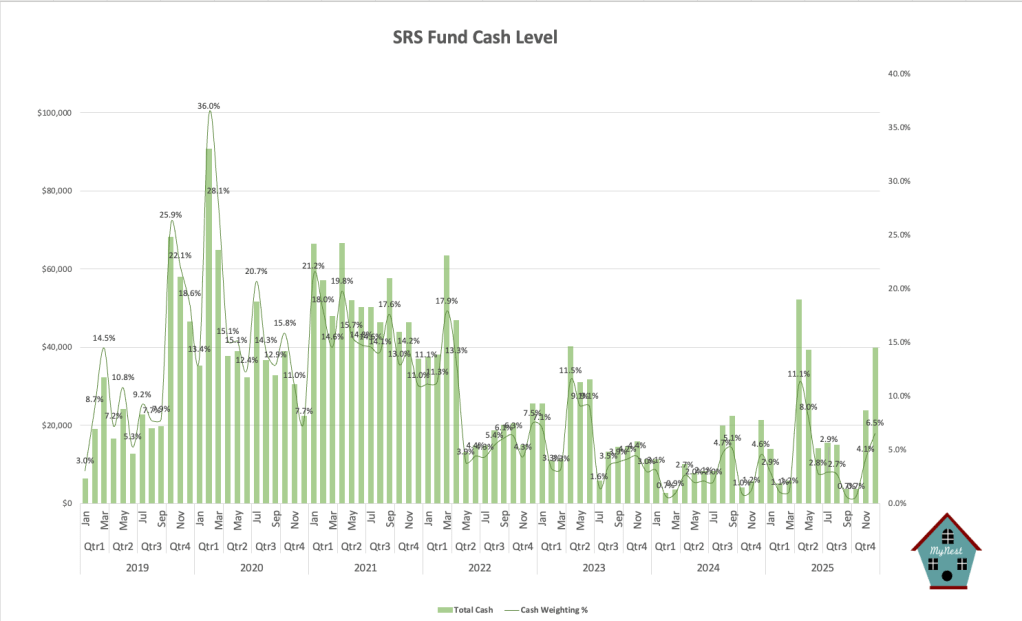

Cash Levels

Following the latest cash contribution and the retention of proceeds from the earlier reduction of the UOB position, the SRS Fund’s cash level has increased to 6.5%. This cash buffer provides flexibility going into 2026, allowing the SRS Fund to respond opportunistically to market dislocation or attractive valuation setups.

Final Thoughts

While past performance should never be extrapolated blindly, the 2025 rally in the STI appears to be underpinned by genuine structural and macroeconomic drivers rather than short term speculation. If these forces persist, Singapore equities may finally be entering a period of renewed relevance after years of relative underperformance.

-

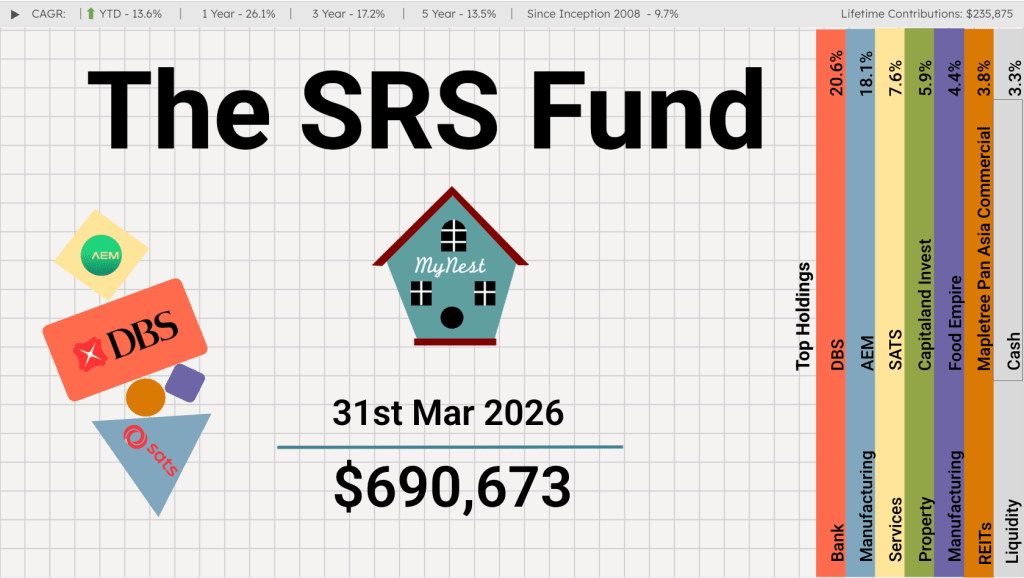

The SRS Fund Mar 2026

It is an enduring market reality that a concentrated minority of holdings drives the vast majority of returns. For years, DBS (currently the largest individual holding at 20.6%) has served as the compounding engine of the SRS Fund.

-

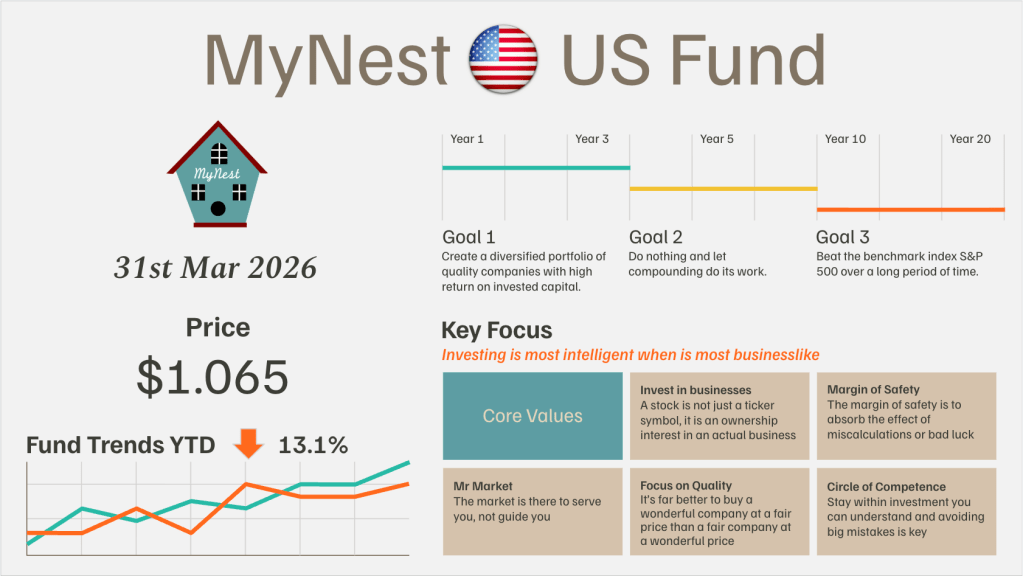

MyNest US Fund Mar 26

March shattered any lingering market complacency, pivoting sharply from the localized damage of the “SaaS-pocalypse” to a systemic shock driven by the war in Iran.

-

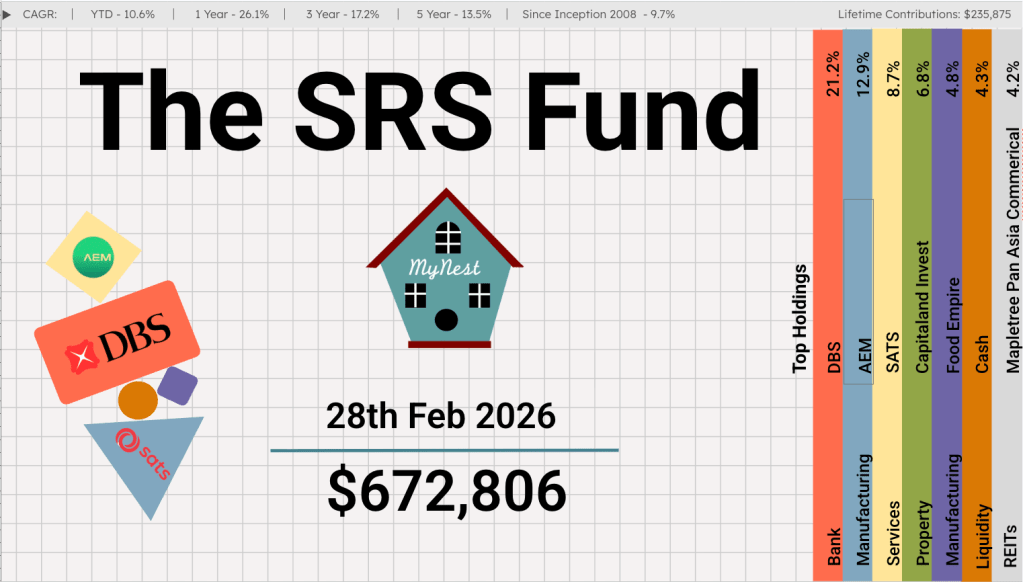

The SRS Fund Feb 2026

The Singapore Budget 2026 has set a robust backdrop for local investors. For the third consecutive year, the government is operating from a position of immense “dry powder,” with an overall fiscal surplus of $8.5 billion projected for FY2026.

-

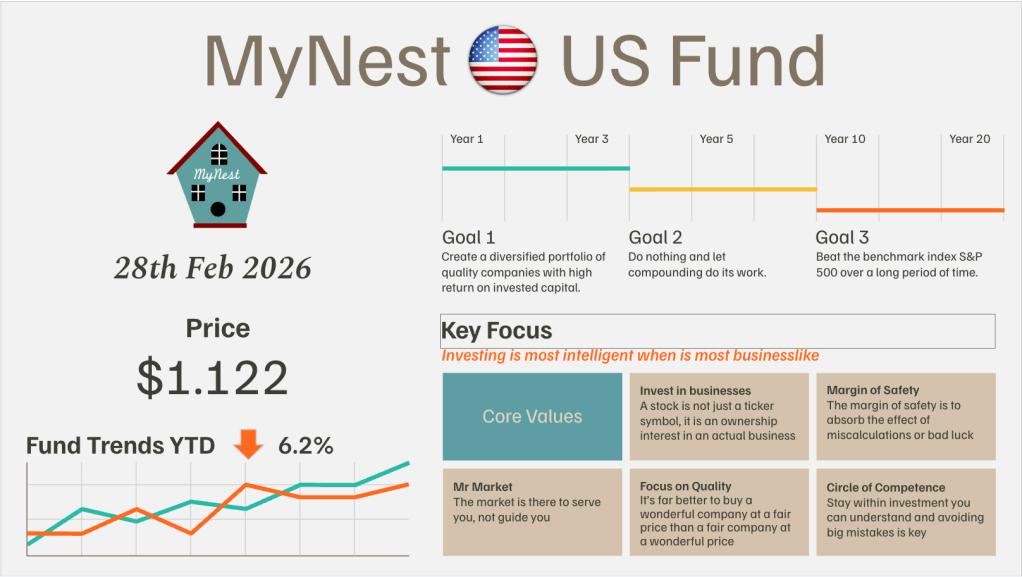

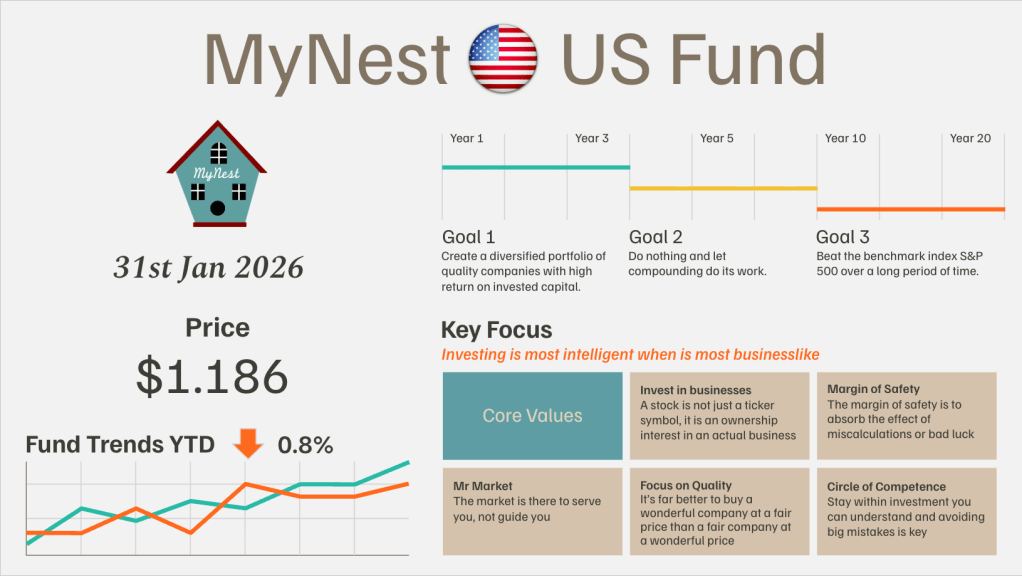

MyNest US Fund Feb 26

February 2026 proved to be one of the most challenging months for our fund since its inception. A wave of “AI anxiety” swept through the Software-as-a-Service (SaaS) sector

-

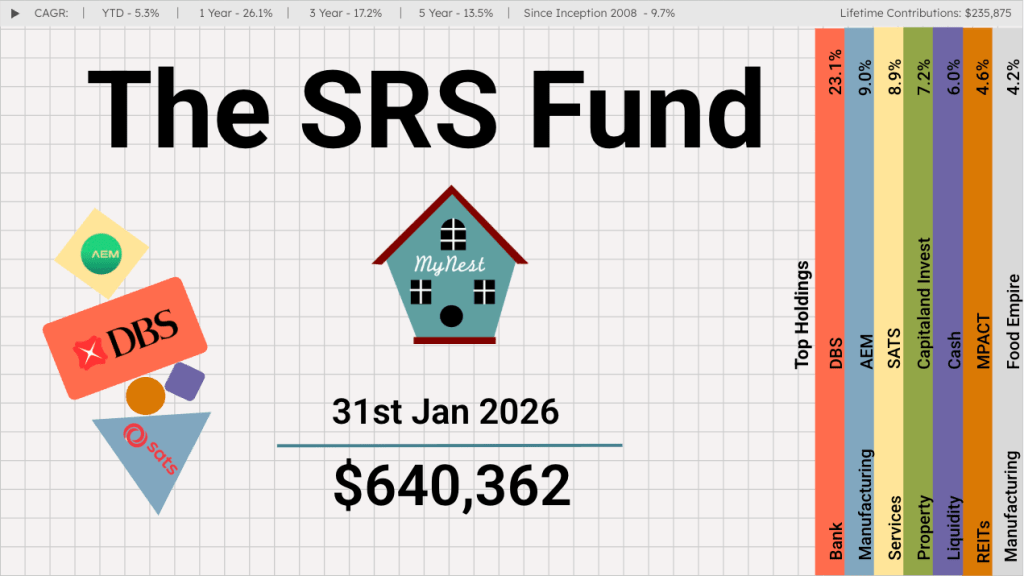

The SRS Fund Jan 2026

After a blockbuster 2025 that saw GDP growth hit a surprise 4.8%, the first month of 2026 has proven that the momentum is far from a fluke. Between record-breaking stock market performance and massive industrial investments, the “Little Red Dot” is making a very big noise.

-

MyNest US Fund Jan 26

I have a confession to make. After reading Chip War at the end of 2022, I fully grasped the strategic importance of TSMC and ASML in the global semiconductor supply chain.