What a difference a month make. This March we watch the banking crisis unfolded as something finally broke after long periods of interest rate increases. Both the casualties Silicon Valley Bank SVB and Credit Suisse are not technically close but their shareholders had been truly wiped out without a doubt. With this turn of event something interesting is transpiring in the bond market.

Since the turn of the year, the bond market begin to bet that the Fed will start to pause and turn around sooner rather than later as we watch interest rates across the curve starts to inch lower. When the bank crisis broke out mid March interest rates really begin its dive as investors shifted their assets into safety of bonds.

With the crisis unfolding, the Fed over that weekend guaranteed all deposits of SVB stemming out an immediate crisis but left open a possible slower contagion of fear by not guaranteeing all deposits throughout. At the FOMC, Jerome Powell reiterated the need for cautious as he keeps his eyes firmly on inflation with a quarter point hike. However, he also suggest they are close to the terminal rate and likely one more hike is in place before a long pause.

I believe the Fed will do what they say (even though they may be wrong) and market will have to adjust accordingly. As such interest rates will likely stay high for the rest of the year and more things will continue to break along the way. I am inclination at this point to look towards the commercial real estate market which have high leverage and are not restructured to withstand an extended period of high rates.

My view to inflation is that it is not a beast that can be easily tamed. A stab to inflation will see it retreat but investors thinking it will not fight back may be in for a nasty surprise. Inflation will likely stay volatile over the next decade and investors with a good sense of it will likely come up on top in such an environment.

The SRS Fund Review

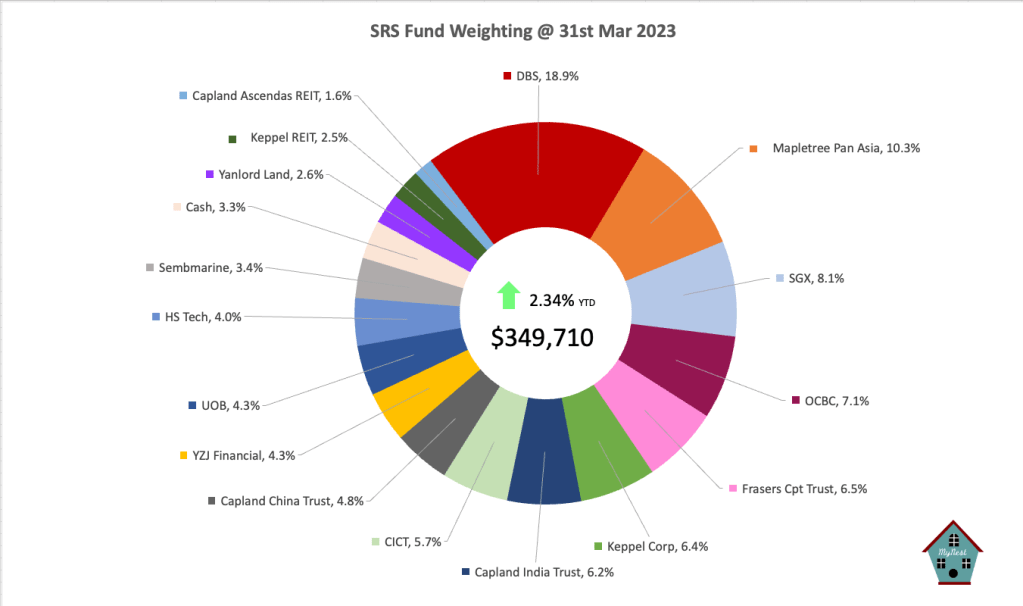

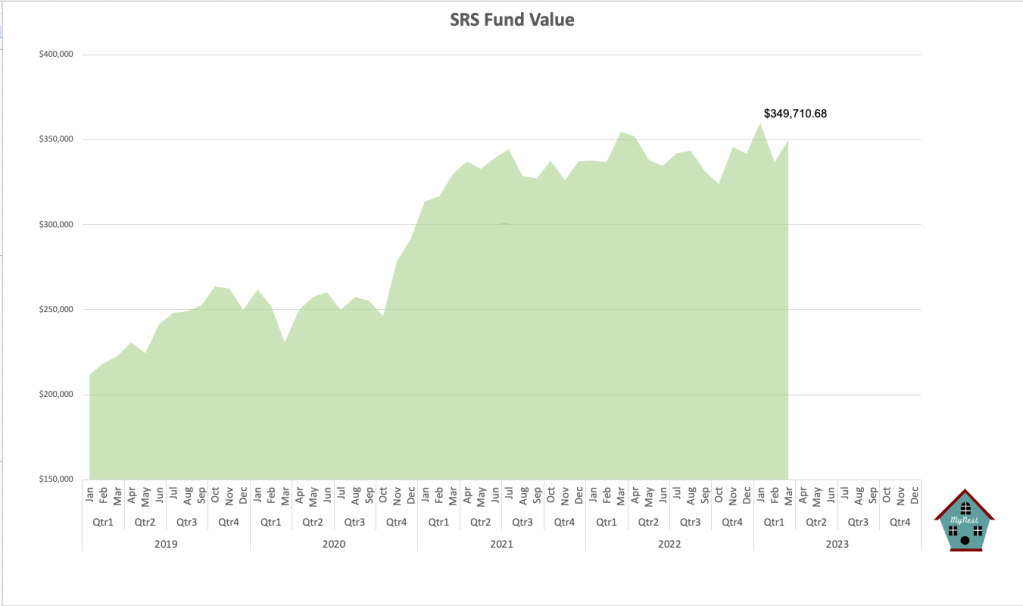

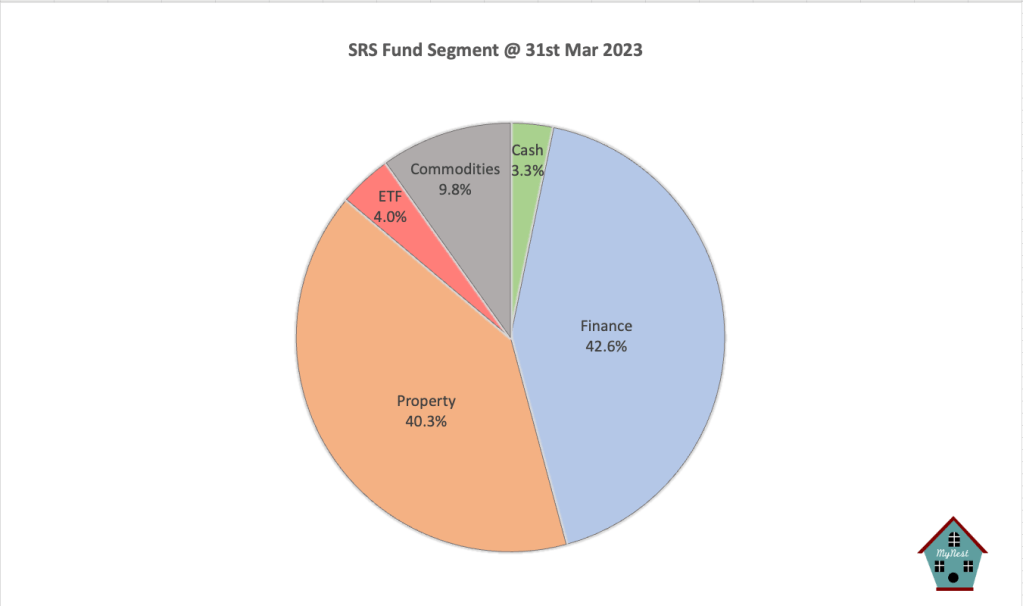

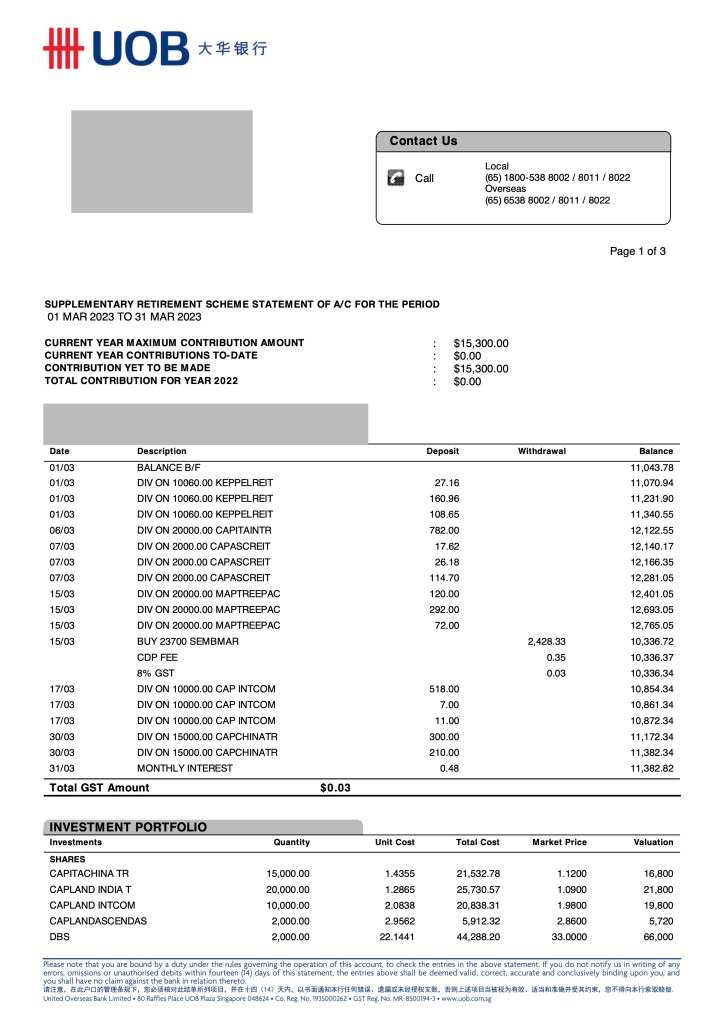

The SRS Fund recovered from Feb and is now back into the green up 2.34% year to date. I took the opportunity of the selloff in Sembmarine to buy more shares taking it up to 3.4% of the portfolio. The month saw rises across the board in particularly in REITs and Banks. After a lagging 2022, the fund is finally ahead of its benchmark the STI by a full 2%.

With REITs rebounding somewhat I may take the opportunity to trim some of the fund REITs holding to position the portfolio for greater interest rate volatility ahead. Banks are expected to do well for the year and I may put more cash to this sector when opportunity arises.

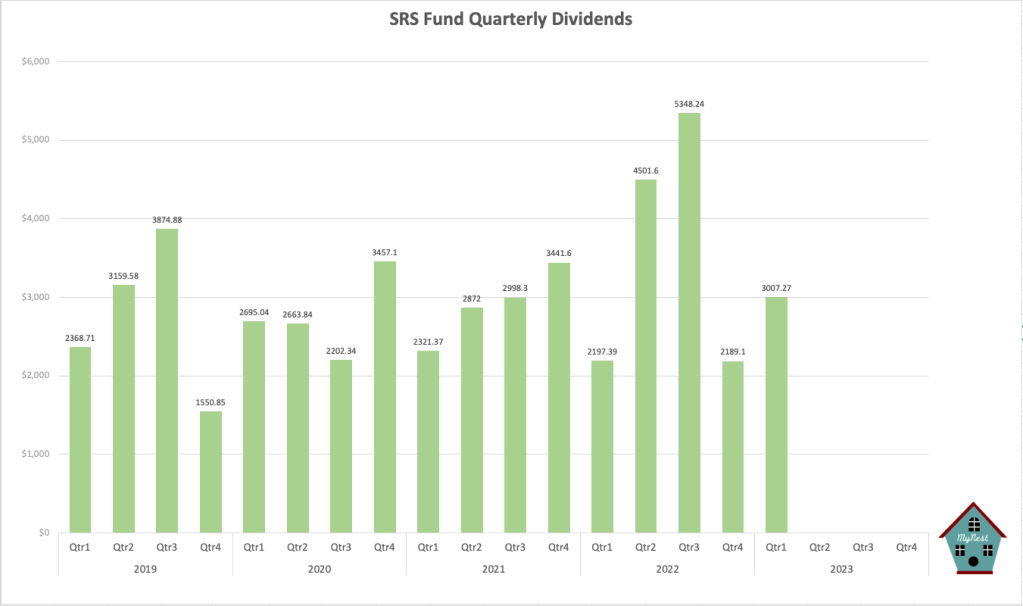

The SRS Fund see another record dividend inflow for Q1 with $3007.27. With a host of AGMs and quarterly earnings upcoming the dividend inflow is likely to continue in Q2. I am inclined to build up the SRS Fund cash position such as to prepare for any unforeseen volatility ahead.

-

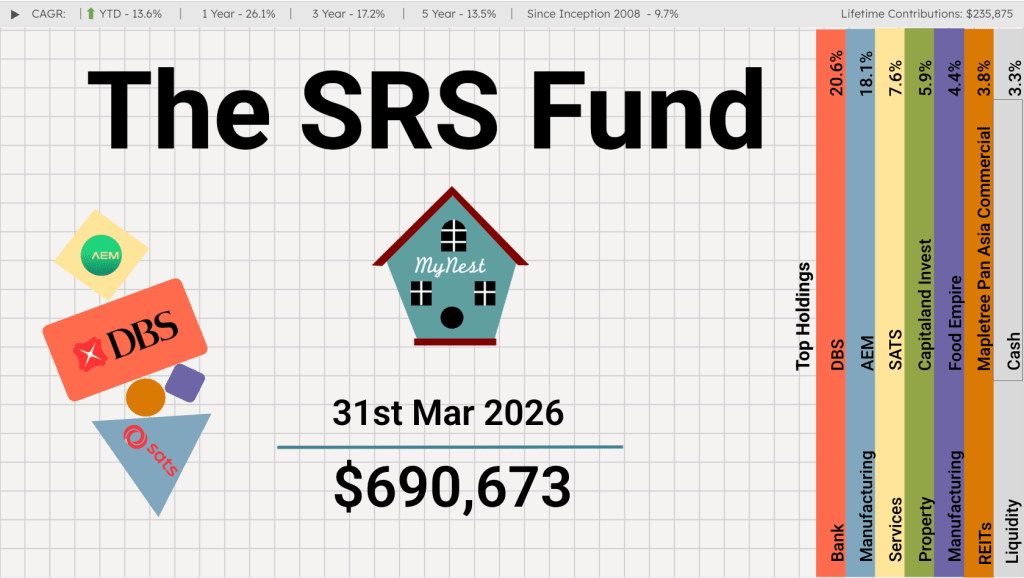

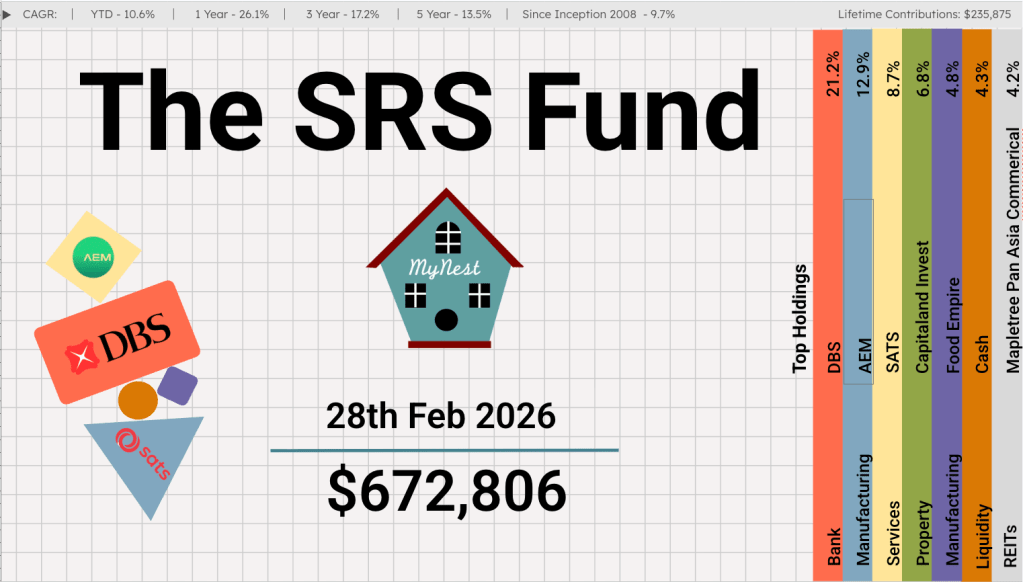

The SRS Fund Mar 2026

It is an enduring market reality that a concentrated minority of holdings drives the vast majority of returns. For years, DBS (currently the largest individual holding at 20.6%) has served as the compounding engine of the SRS Fund.

-

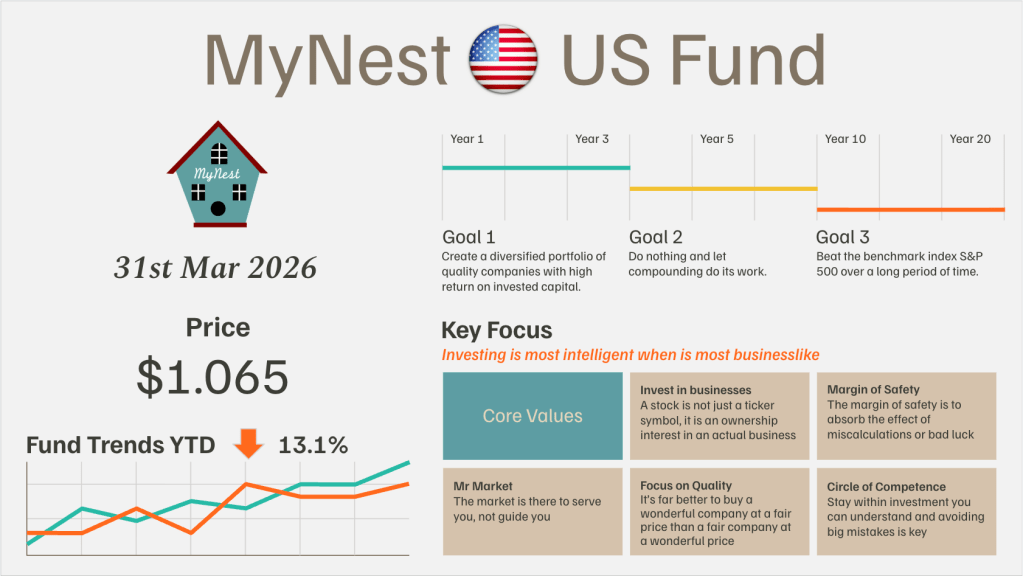

MyNest US Fund Mar 26

March shattered any lingering market complacency, pivoting sharply from the localized damage of the “SaaS-pocalypse” to a systemic shock driven by the war in Iran.

-

The SRS Fund Feb 2026

The Singapore Budget 2026 has set a robust backdrop for local investors. For the third consecutive year, the government is operating from a position of immense “dry powder,” with an overall fiscal surplus of $8.5 billion projected for FY2026.

-

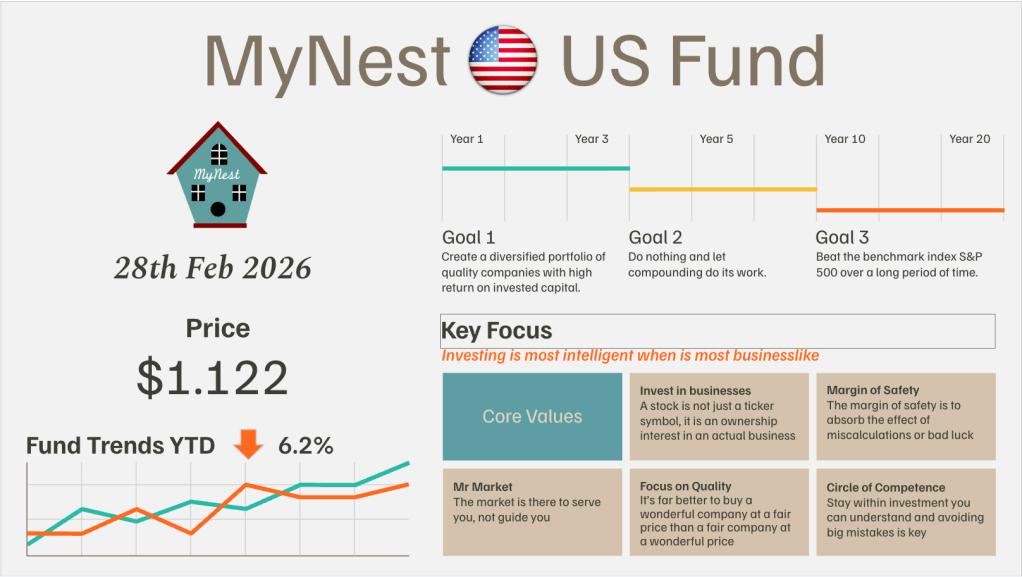

MyNest US Fund Feb 26

February 2026 proved to be one of the most challenging months for our fund since its inception. A wave of “AI anxiety” swept through the Software-as-a-Service (SaaS) sector

-

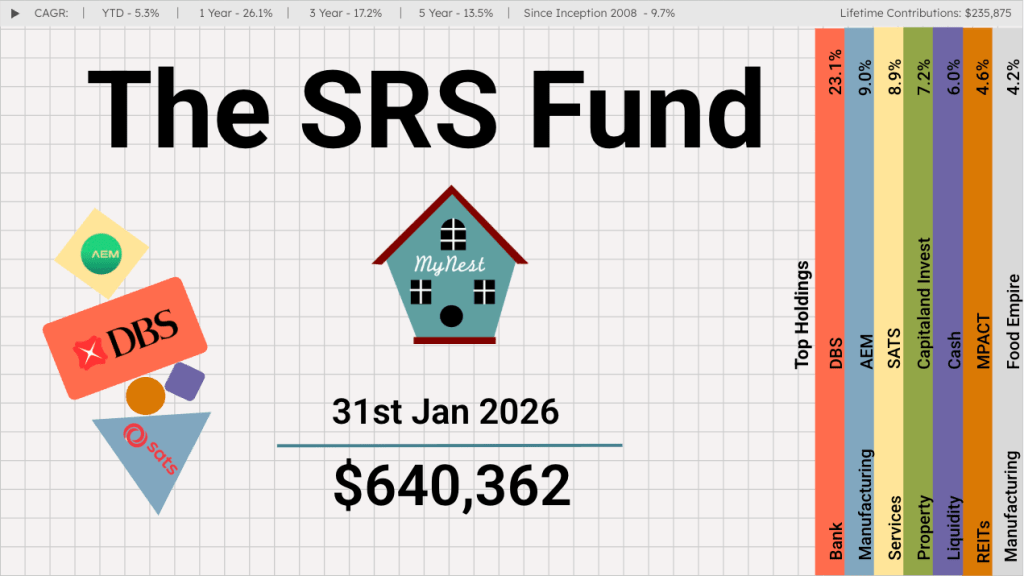

The SRS Fund Jan 2026

After a blockbuster 2025 that saw GDP growth hit a surprise 4.8%, the first month of 2026 has proven that the momentum is far from a fluke. Between record-breaking stock market performance and massive industrial investments, the “Little Red Dot” is making a very big noise.

-

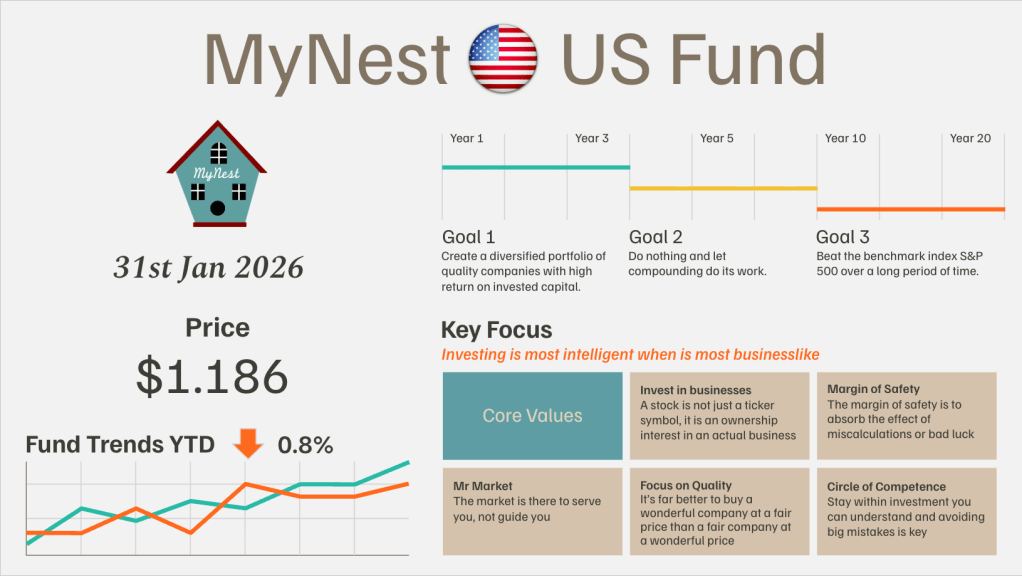

MyNest US Fund Jan 26

I have a confession to make. After reading Chip War at the end of 2022, I fully grasped the strategic importance of TSMC and ASML in the global semiconductor supply chain.