When the facts changed a flexible mind should have the ability to accept the changed facts and adjust accordingly. For some time now, it has become clear to me that the low interest rate environment that we enjoy for the past many decade has come to an end. Inflation will be a beast likely to be fought for many years to come and interest rate will likely be more normalise to prevent inflation from spiking.

In this environment, real estate investment trust (REITs) are likely to experience a painful adjustment with distribution falling as rental reversion slowly catches up to the increasing cost and expenses.

Sure inflation will ensure higher pricing power which will normalise the cost-revenue dynamics. However the path to this normalisation will be difficult, rocky and likely take many years.

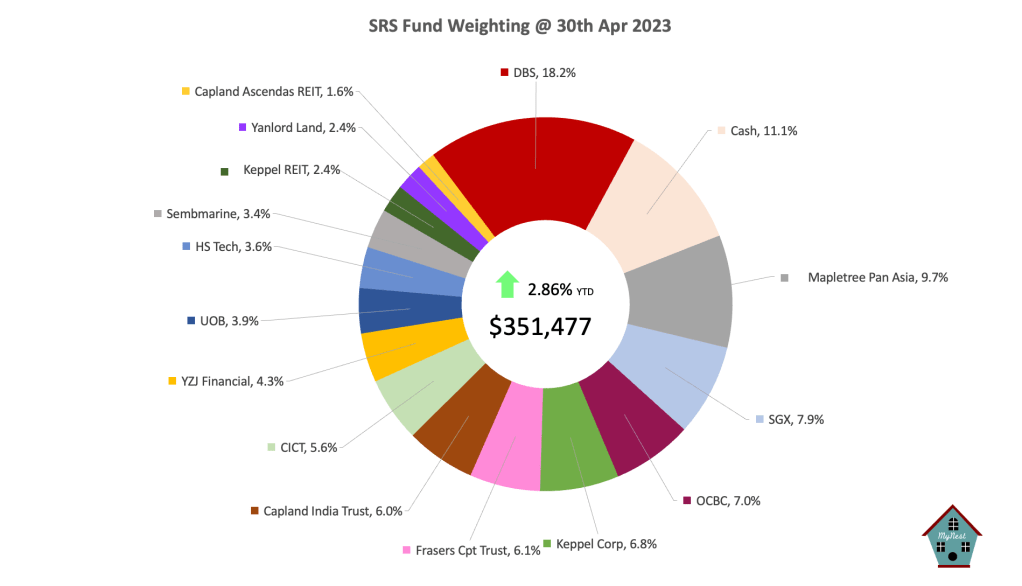

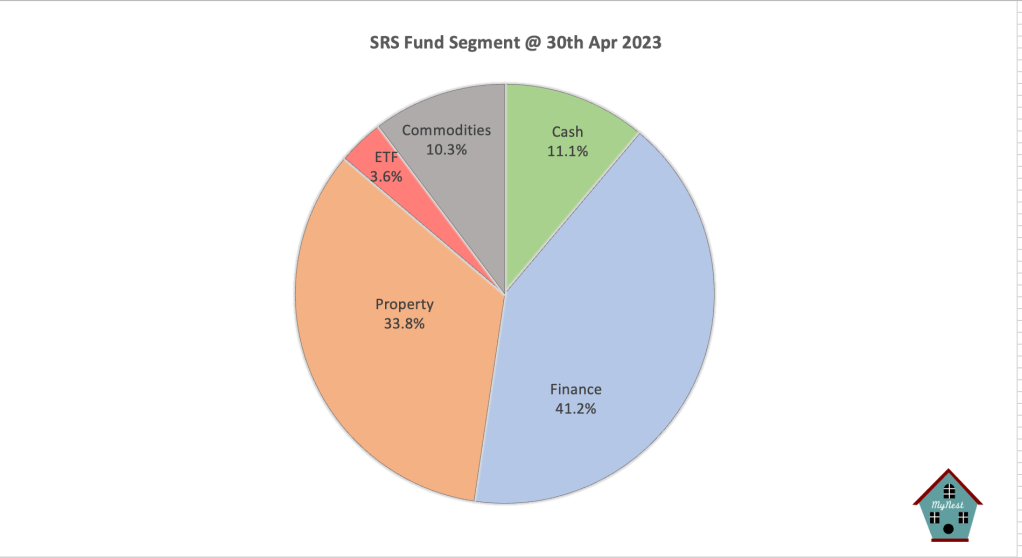

As a result and given the opportunity by the market, I have accordingly able to reduce the REITs exposure in the SRS Fund down to 30%. While I would have prefer to have even lower exposure at 20%, opportunity (to sell at a reasonable price) would have to emerge

The SRS Fund Review

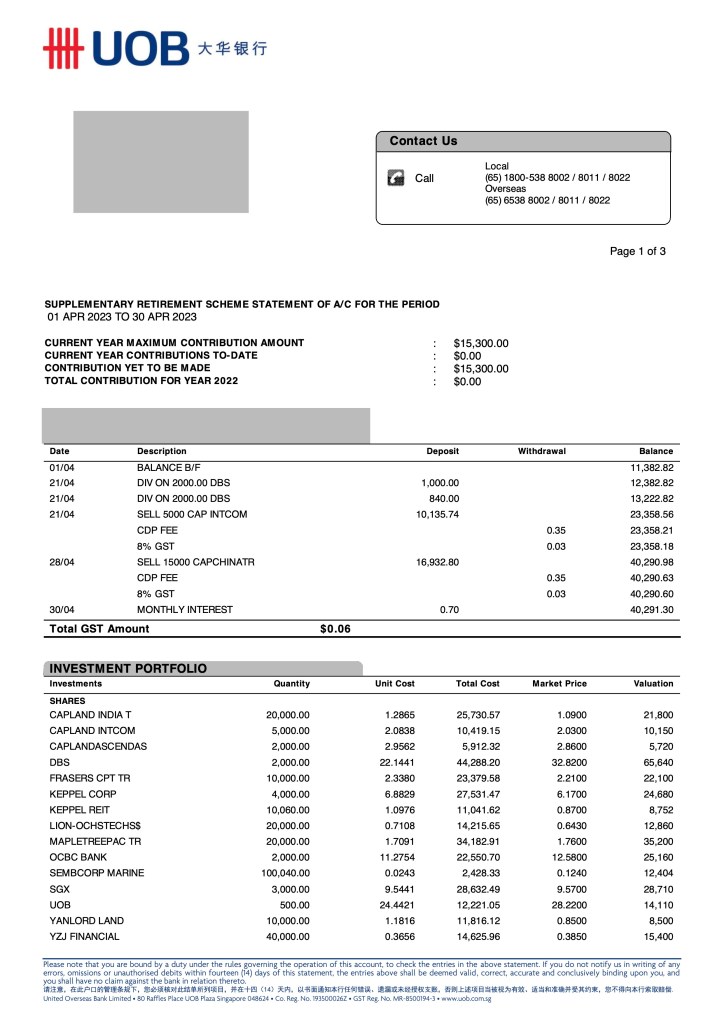

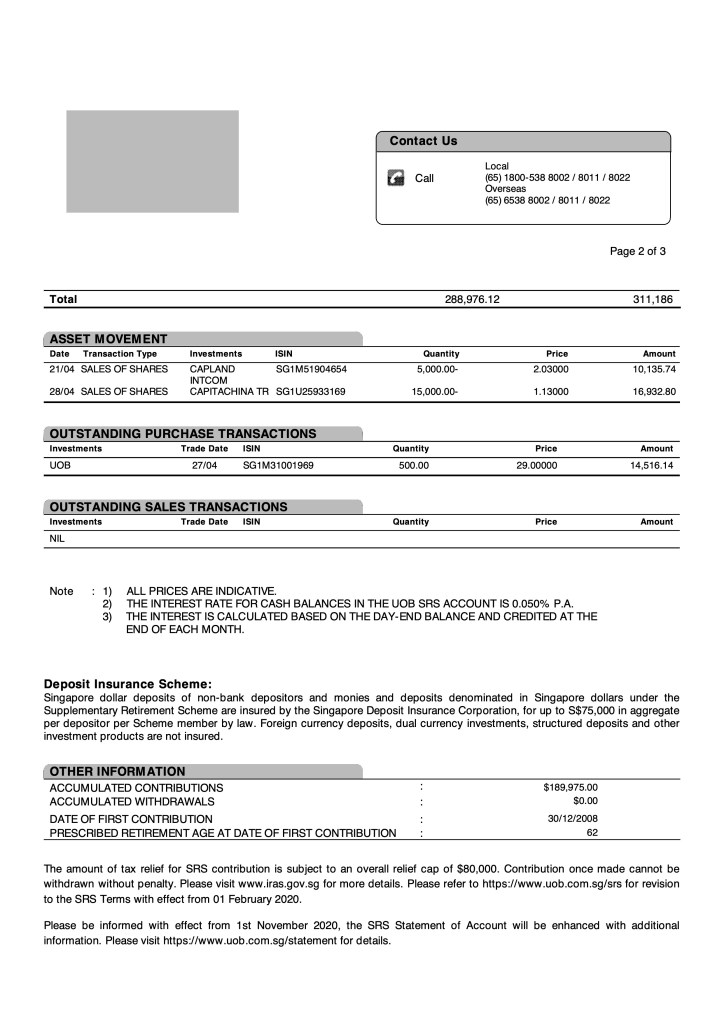

The SRS Fund continue its slight upward trajectory up 2.86% year to date versus the STI return of 0.6%. Keppel Corp and the newly named Seatrium (Sembmarine) leads the charge for the portfolio.

There was also some reposition of the SRS Fund during the month as I completely dispose of Capland China Trust to reduce my exposure to the REIT sector. Together with a reduction in Capland Integrated Commercial Trust, I use the proceeds to add to the Fund’s UOB position analysing that it should out perform after its completion of the purchase of retail banking business from Citi in the medium term.

One should be able to see it in the update in May of these changes as it was done toward the end of April.

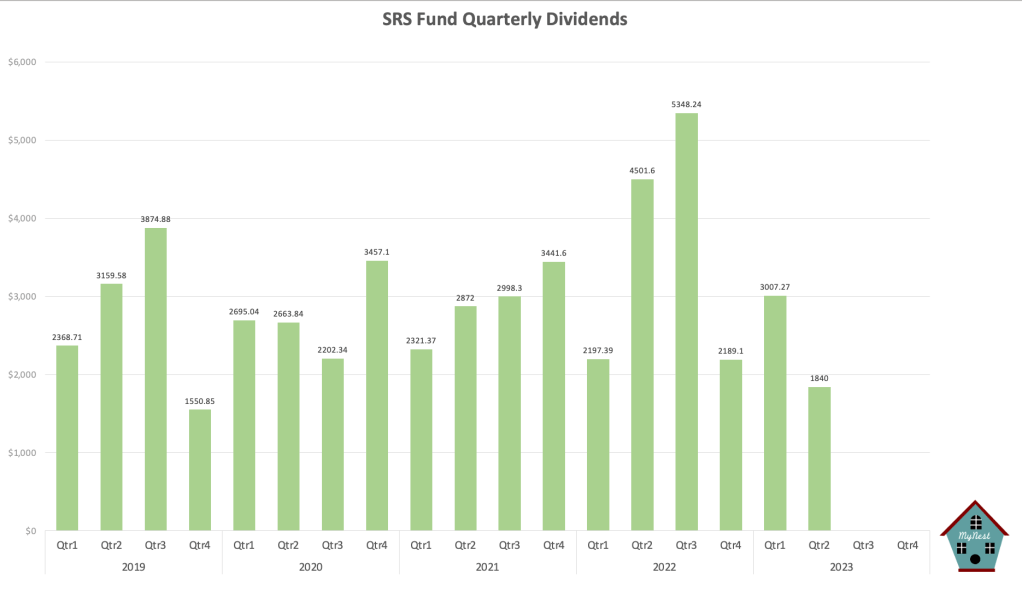

Only the DBS year end dividend was recorded for the month of Apr despite the number of companies going ex dividend. We should however see another record quarter in Q2 in terms of dividends. Overall with the economy doing well and rebalancing of the Fund away from REITs, the Fund should see steady growth and continue to outperform the index in the medium term.

-

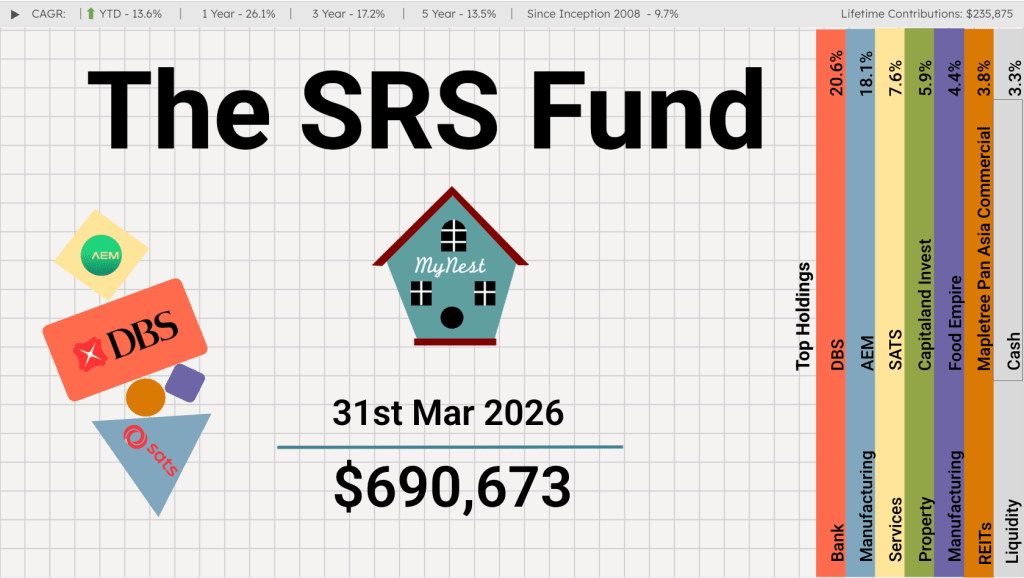

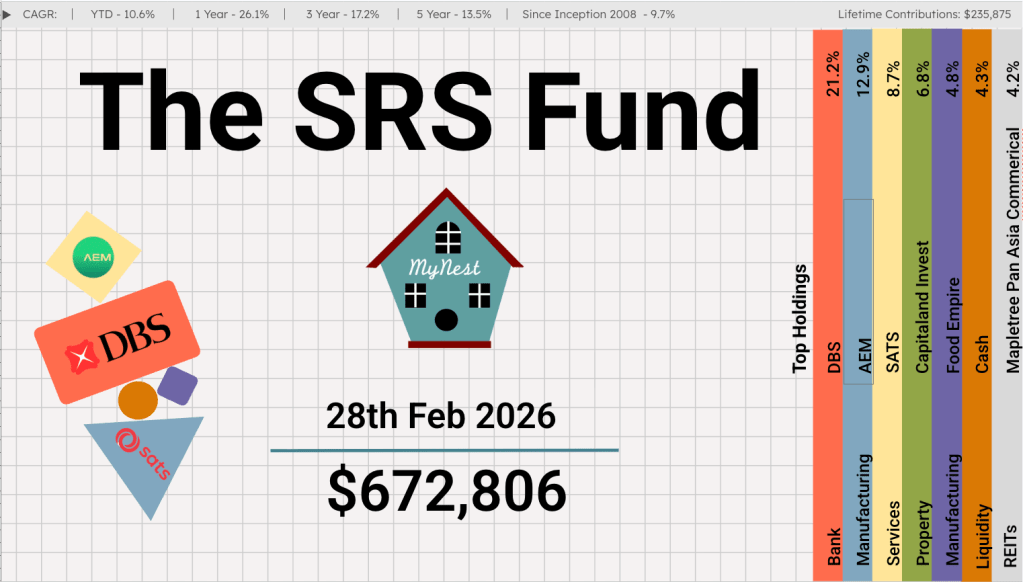

The SRS Fund Mar 2026

It is an enduring market reality that a concentrated minority of holdings drives the vast majority of returns. For years, DBS (currently the largest individual holding at 20.6%) has served as the compounding engine of the SRS Fund.

-

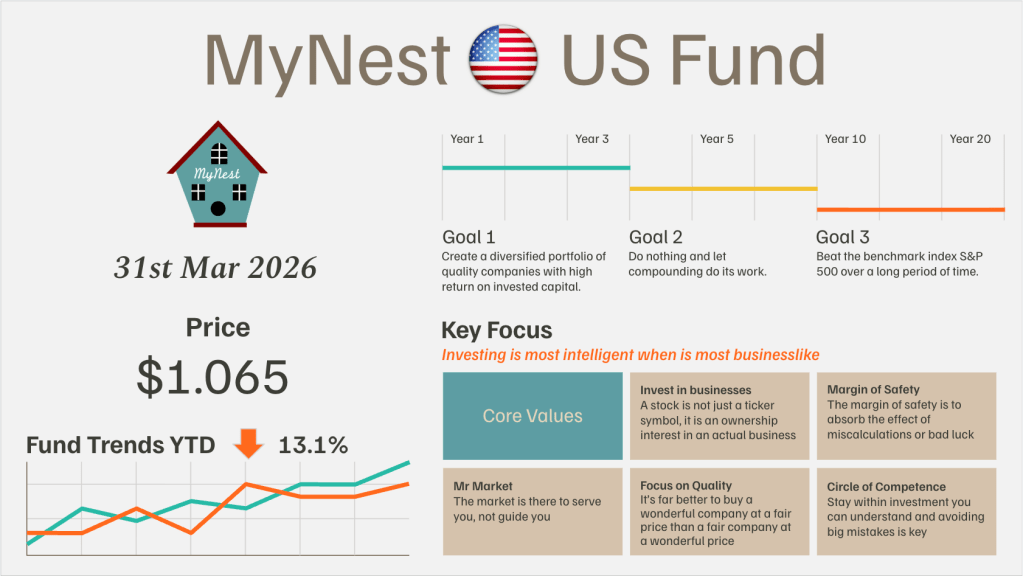

MyNest US Fund Mar 26

March shattered any lingering market complacency, pivoting sharply from the localized damage of the “SaaS-pocalypse” to a systemic shock driven by the war in Iran.

-

The SRS Fund Feb 2026

The Singapore Budget 2026 has set a robust backdrop for local investors. For the third consecutive year, the government is operating from a position of immense “dry powder,” with an overall fiscal surplus of $8.5 billion projected for FY2026.

-

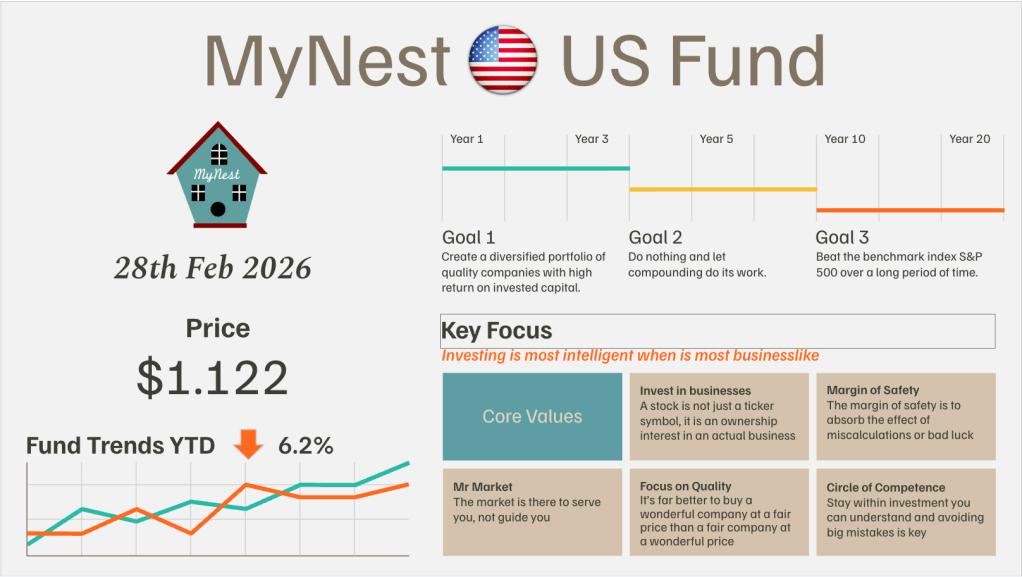

MyNest US Fund Feb 26

February 2026 proved to be one of the most challenging months for our fund since its inception. A wave of “AI anxiety” swept through the Software-as-a-Service (SaaS) sector

-

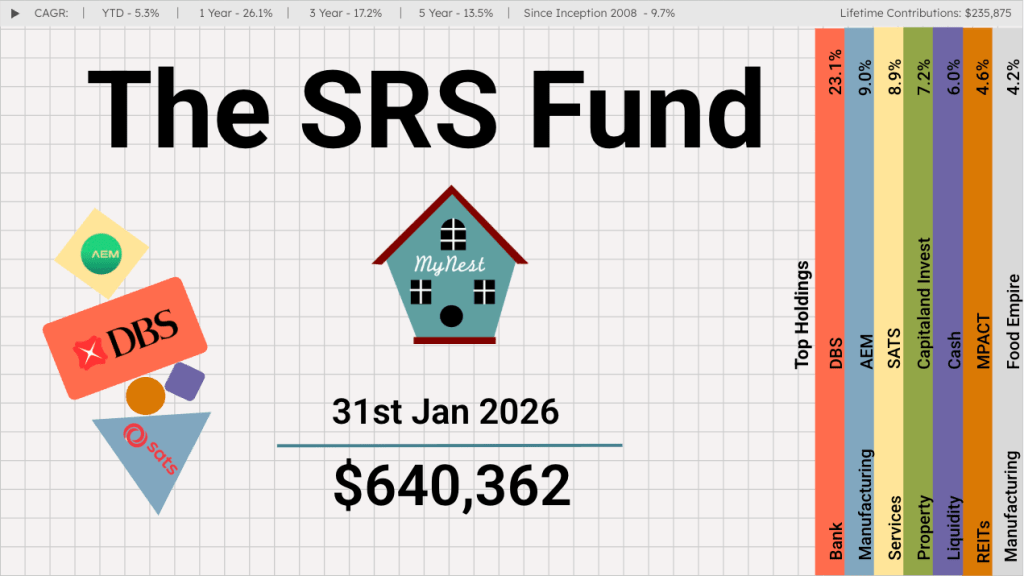

The SRS Fund Jan 2026

After a blockbuster 2025 that saw GDP growth hit a surprise 4.8%, the first month of 2026 has proven that the momentum is far from a fluke. Between record-breaking stock market performance and massive industrial investments, the “Little Red Dot” is making a very big noise.

-

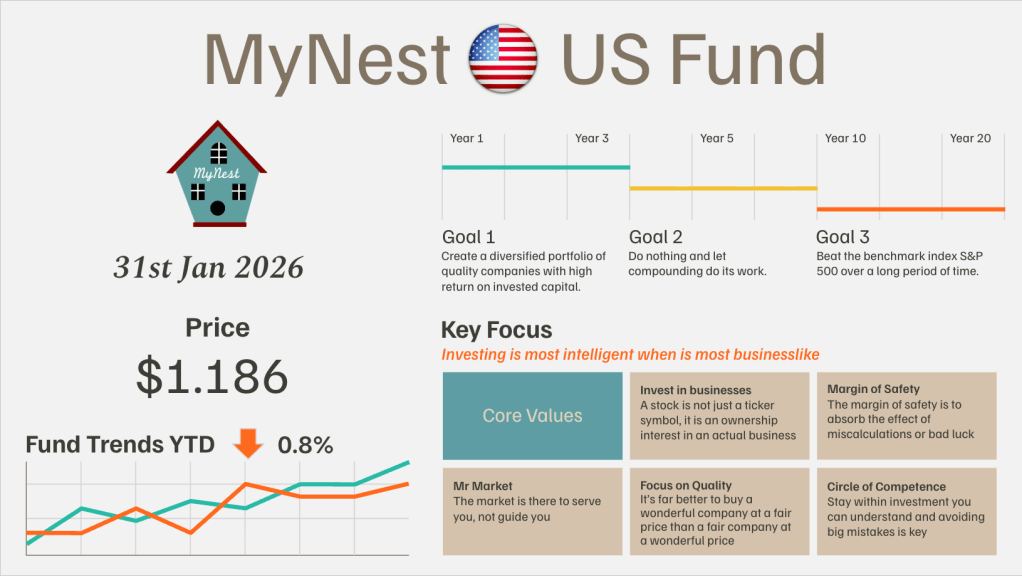

MyNest US Fund Jan 26

I have a confession to make. After reading Chip War at the end of 2022, I fully grasped the strategic importance of TSMC and ASML in the global semiconductor supply chain.