I made this investment at the time when the biggest mainland property firm China Evergrande defaulted on its offshore debt. From then on the Chinese property sector took a dive bringing many property related companies stock to new lows. Sensing an opportunity I did some research and zoom in on this company called Sunac.

Sunac was considered the next to fall as its offshore bond value wobble along as the property crisis unfolded. From a price of HK$30 just 3 months ago it fell to less than HK$15 in record speed. Subsequently, the company did a placement at $HK$15.18 which was well received. My entry price was HK$14.30 with the following thesis

- China cannot afford to have 2 of its biggest property players in default risking contagion to its financial sector. (This obviously did not hold since Evergrade, Sunac, Shimao, and many small players defaulted)

- Sunac Chairman Mr Sun Hongbin had personally loan to the company $450m interest free gave me comfort that there is indeed much value in the company.

- Sunac had their assets in mostly tier 1 and tier 2 cities which make their assets more liquid and they had one of the most dynamic sales team in the country to sell these assets.

- At the price of HK$14.30 it was trading at just 50% of their book value at the point in time

Despite all the above considerations, the property crisis continued to worsen to the point where Sunac’s auditor is unable to give an opinion on its financial results. So in accordance to Hong Stock Exchange rule, the counter was suspended on 1st Apr 2022 joining Evergrade and Shimao in a growing list of troubled property developers.

Fast forward to 2023. Giving credit to the management, the company is able to get its financials together after changing its auditors and publish its long awaited result for FY2021 & FY2022. Obviously the results published confirmed my worst fear as Sunac incur losses of more than RMB$60b in 2 years bringing its book value down to around HK$16 per share.

Sunac resume trading on 13th Apr 2023 after a little more than a year of suspension. Uncertainty still surrounds the stock as the company actively tries to restructure its debt with a skew of complicated debt to equity scheme.

The stock price bore the brunt of disappointed investors as they sold Sunac’s shares to regain the little value of what is left. It recently touch a low of HK$1.09 but since rebounded to about HK$1.43. This investment has lost 90% of its value over a period of less than 2 years. It will have to 10x just to breakeven on cost basis.

The saving grace for this failed investment was that I had follow the rules of diversification and the investment only constitue less than 5% of my portfolio. Nevertheless, it was a painful experience but I am hopeful some value can be realise after China property market normalise.

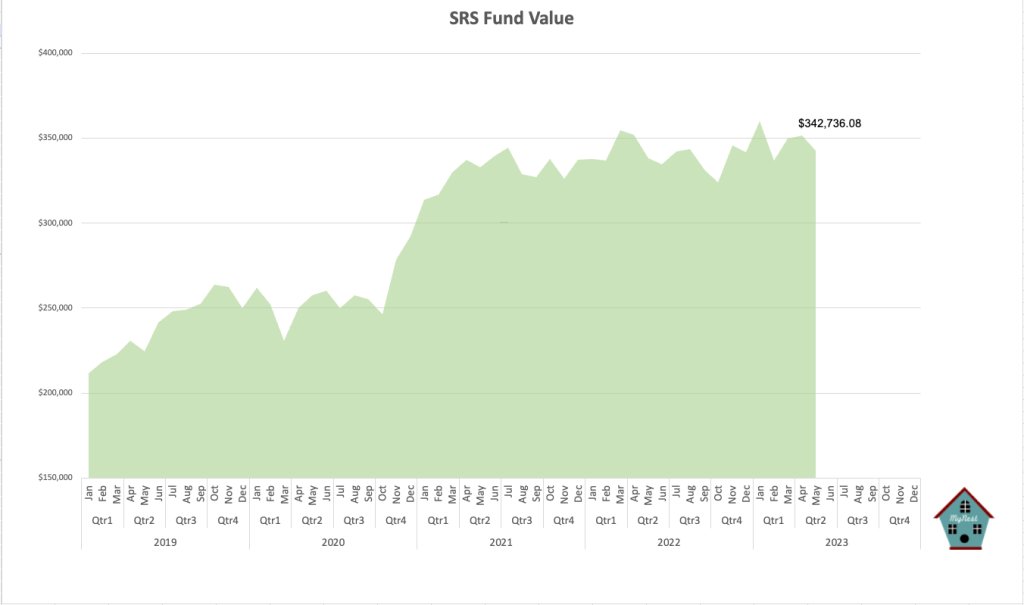

The SRS Fund Review

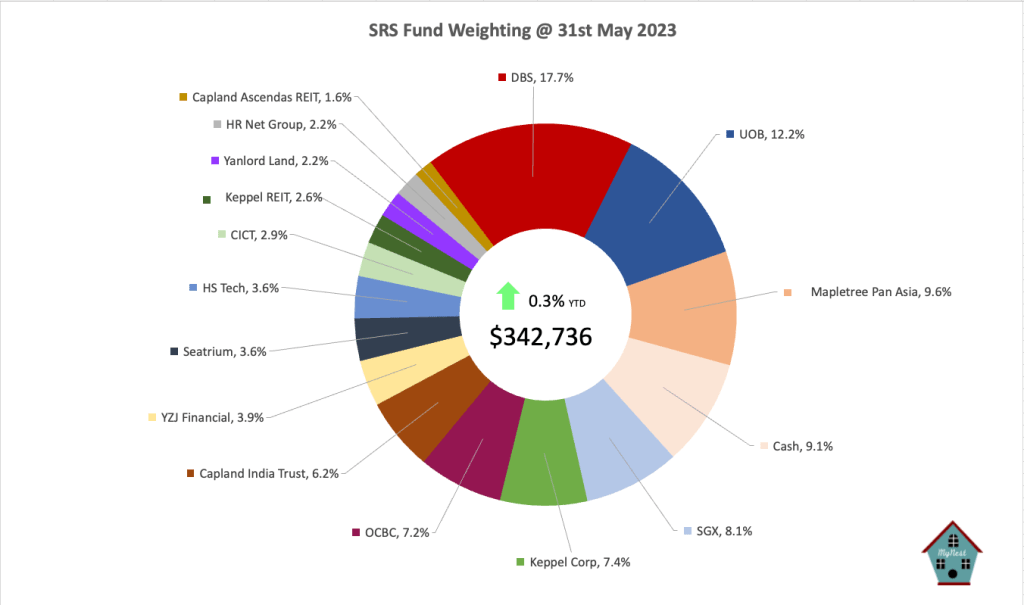

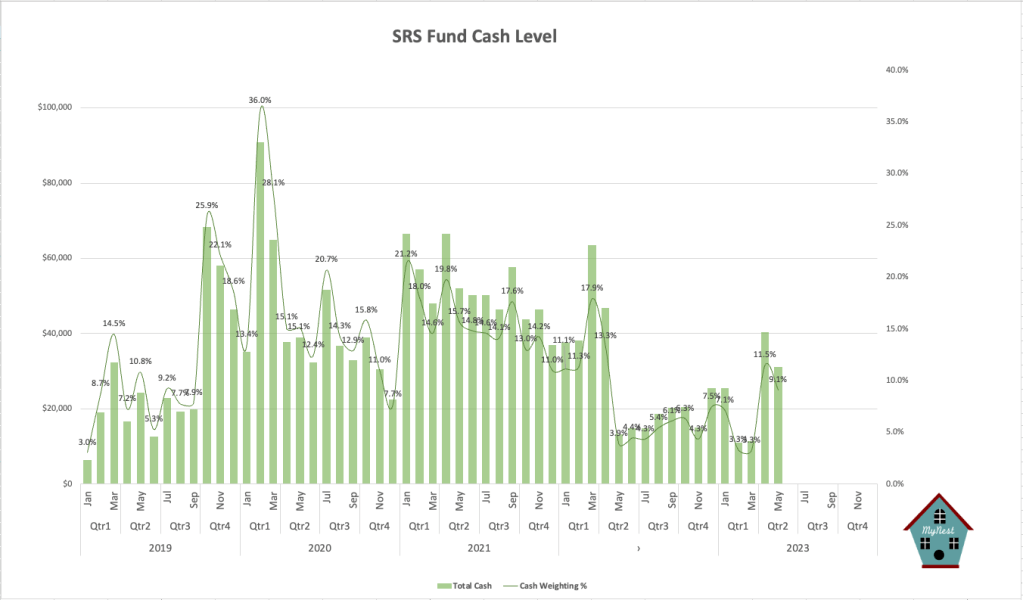

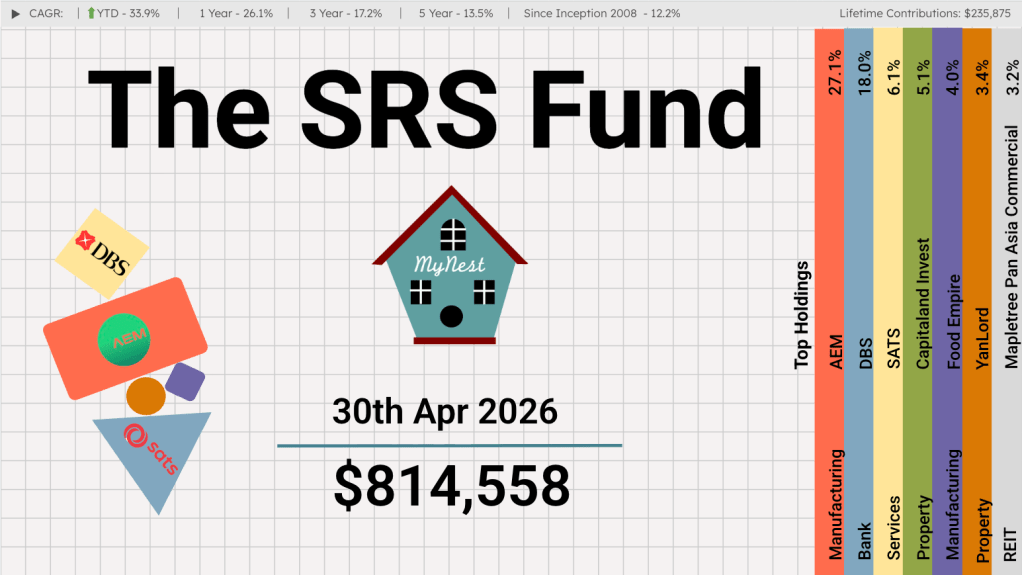

The SRS fund held on within the positive territory for the year as the general market tank in the month of May. STI ended negative down 2.8% for 2023 excluding any dividend. The month had provided me with an opportunity to further rebalance the fund to be less dependent on REITs which is more sensitive to interest rate movements.

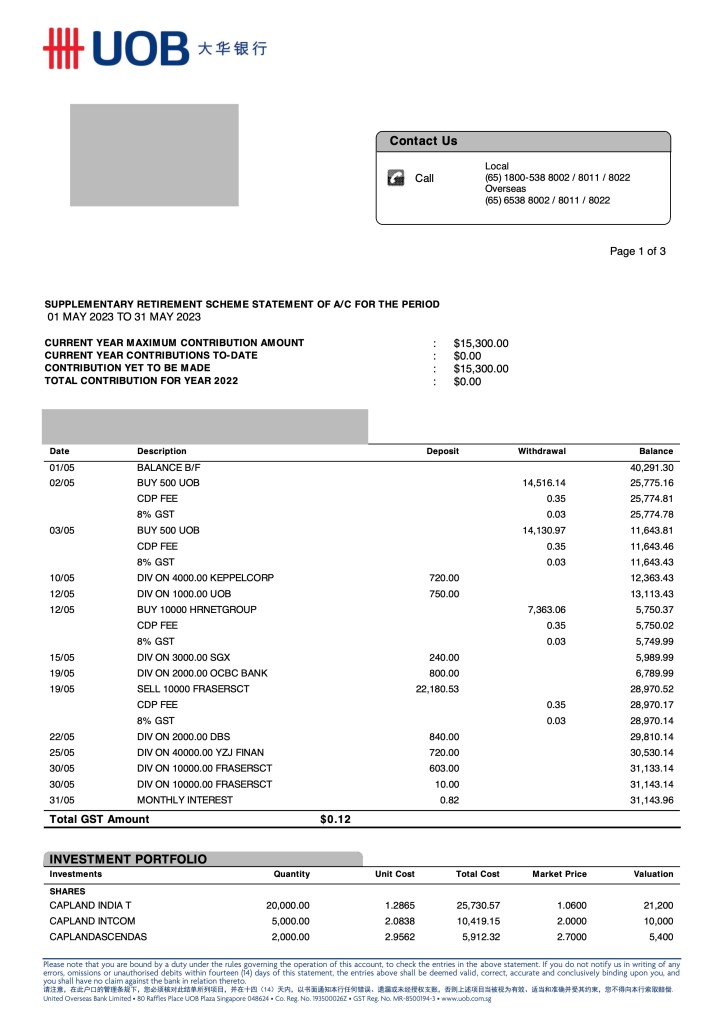

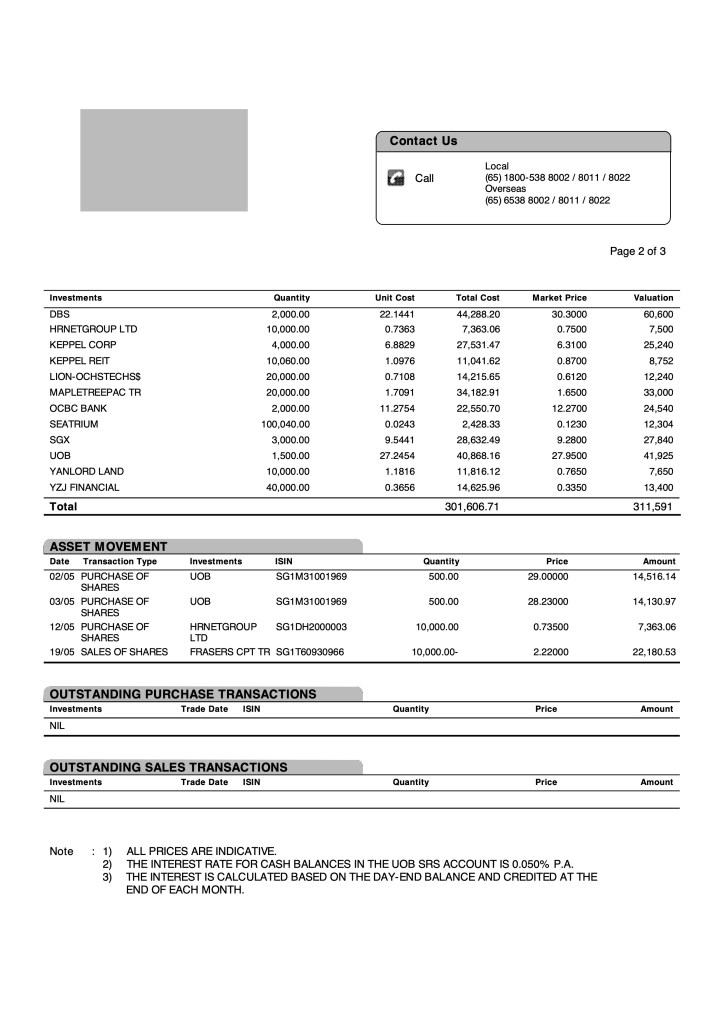

More UOB shares were bought as the banks starts to show weakness with talk of a rate cut around the corner. A new counter HR Net Group was added to the fund to diversify away from REITs. I took the opportunity to dispose Fraser Centrepoint Trust as I see very limited upside with interest rate issue as a hangover to the REIT.

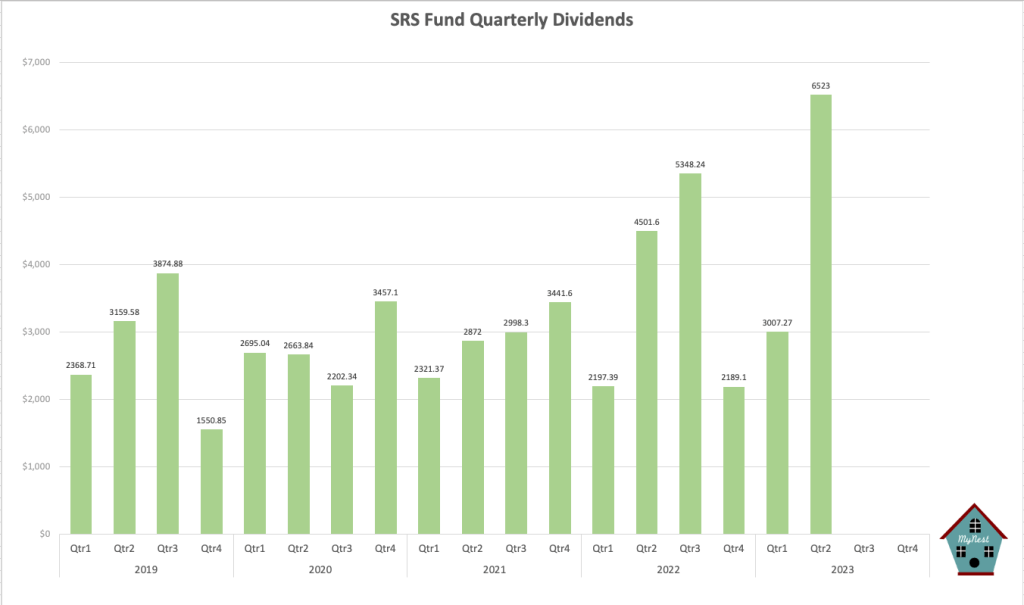

Dividend shot through the roof in Q2 as the underlying companies especially the banks deliver record profits. In fact I had to adjust the scale of the above graph just to allow the number to be visible. It was also this record dividend that allow the SRS fund to remain positive despite a difficult market.

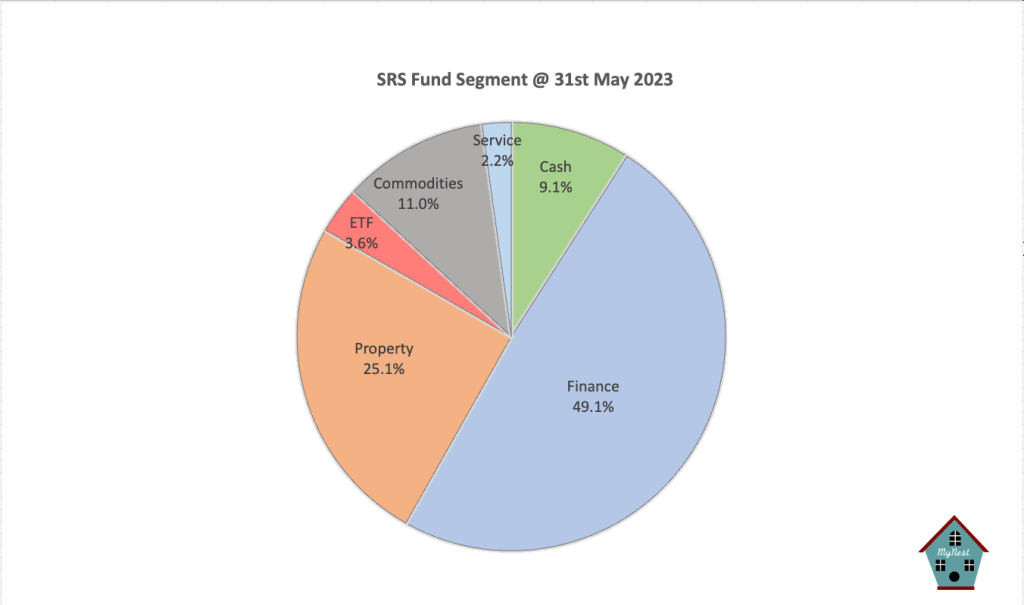

After much rebalancing, the properties segment now account for only 25% of the fund. Much of these rebalancing is done and I am confident the SRS fund will be a more resilient all weather portfolio.

-

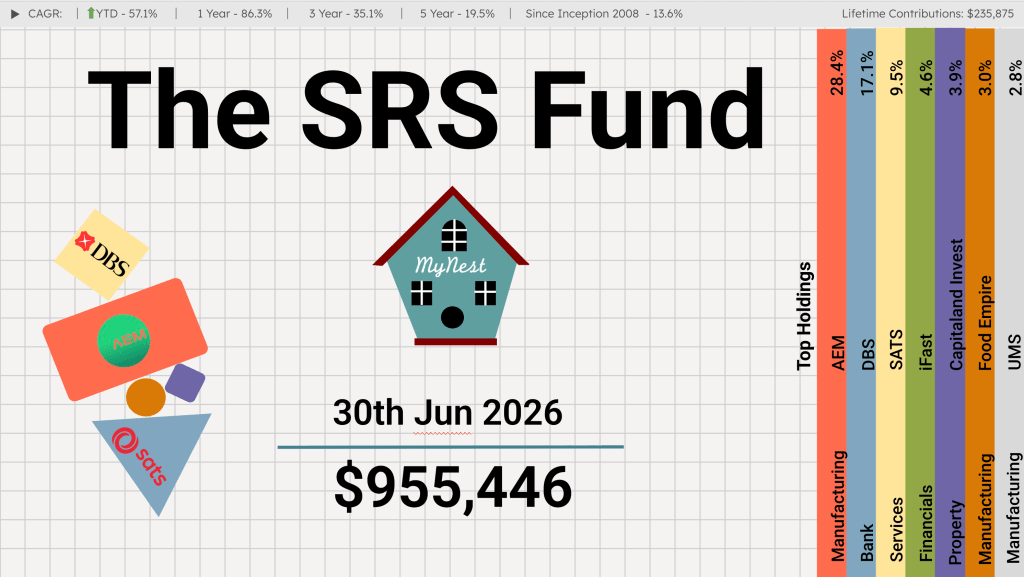

The SRS Fund Jun 2026

The month of Jun provided an important milestone in the Iran conflict. The agreement between the United States and Iran marked a significant step towards reducing geopolitical tension and reopening a clearer path for global energy flows

-

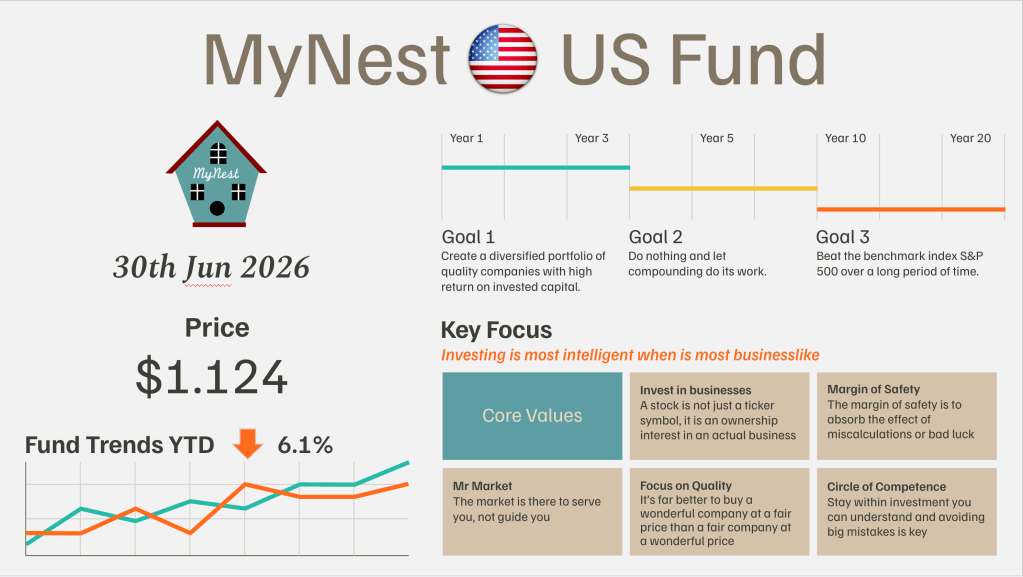

MyNest US Fund Jun 26

June was another remarkable month in the evolution of the global capitalism and the artificial intelligence investment cycle.

-

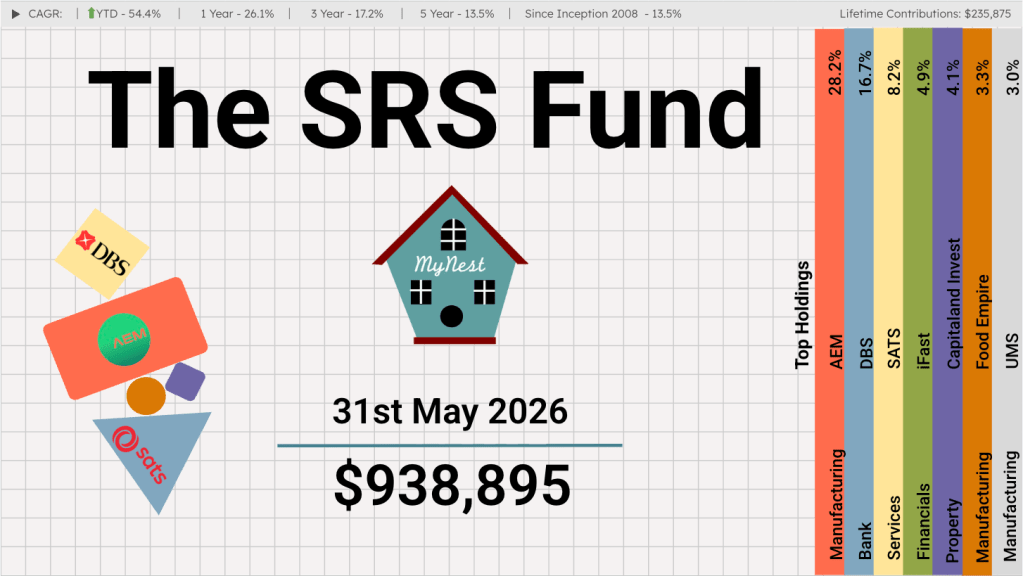

The SRS Fund May 2026

Korea, powered by the worldwide shortage and surge in memory demand, was hit directly by the AI wave, with its stock market more than doubling in a matter of 5 months. Taiwan, already the world’s most important advanced chip manufacturing hub has risen to become one of the largest stock market globally.

-

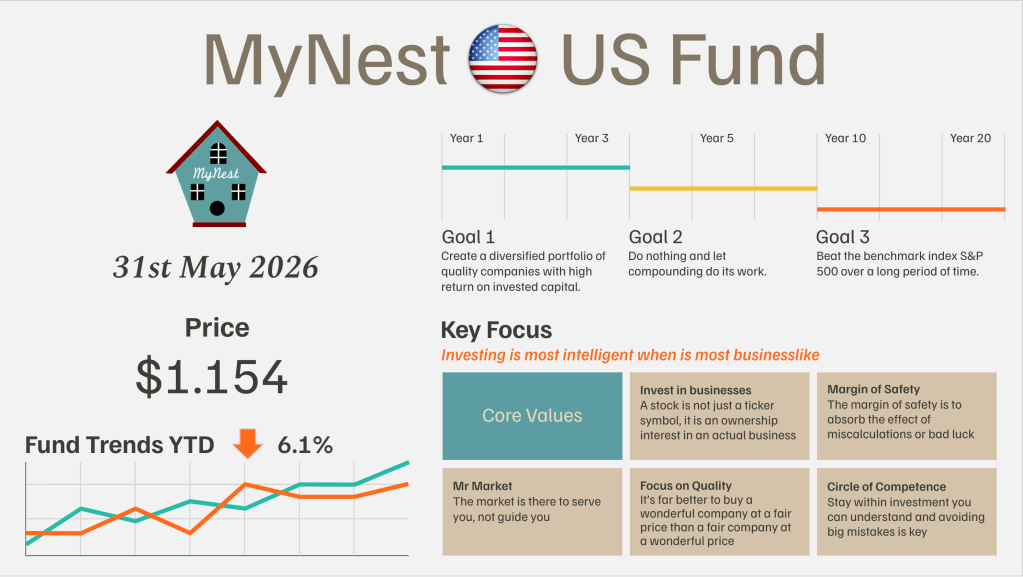

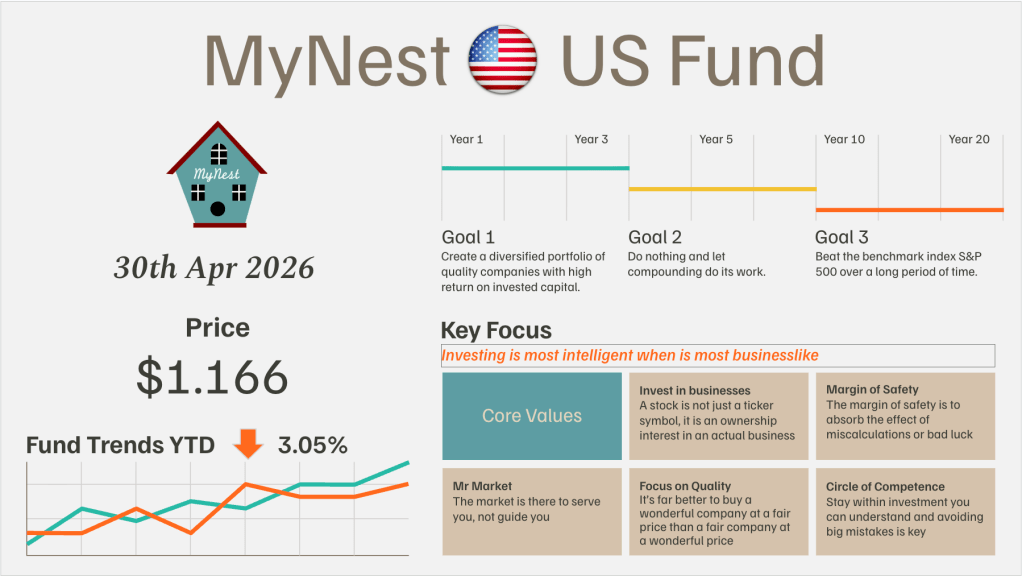

MyNest US Fund May 26

May has been an incredibly illuminating month for the MyNest US Fund. Looking across the broader landscape, the S&P 500 Index has continued its steady leg up, gaining +5.15% in the month of May alone to push its Year-to-Date (YTD) gain to +10.73%.

-

The SRS Fund Apr 2026

In my investment journey, there have been three occasions where I witnessed a company deliver a 10x return.

-

MyNest US Fund Apr 26

The market rebounded strongly in April as investors appeared to look past geopolitical uncertainty and renewed their focus on earnings, artificial intelligence, and the long-term growth prospects of quality businesses.

2 responses to “Worst Investment Ever”

hi,

I think you did well and you do sound like a male and have the strong income so i would have continued contributing to SRS to enjoy tax breaks.

You may wish to revisit the assumption on withdrawal and contribution to SRS funds. Eg withdrawal of your SRS funds can be stretched further even with $1.4m portfolio with tax breaks . Go watch the youtube video from Josh tan on buying annuities using SRS funds. .

If you are a woman with kids, then the child tax breaks and the cap of the tax breaks doesnt make sense anymore for SRS contribution and if that your reason for stopping, then i agree to stop.

LikeLike

Hi C game,

Annuities is really not my thing as they have no residual value after one pass (I can’t even donate to charity). Hence I am just going to withdraw my shares in equal portion over 10 years. With a say $1.4m SRS portfolio (compounded @ 8% per year), withdrawal can hit up to $200k per year which means $100k is subjected to tax. I wouldn’t bet on the government raising tax bracket to $100k and above. That is already assuming I have no income during that time.

I have since found a way to get similar tax breaks by doing voluntary CPF contribution to Medisave and spouse which is more efficient and tax free upon withdrawal.

LikeLike