Portfolio Optimisation

September was a rather non-eventful month in the stock market. However, I have continued to optimise the SRS Fund in its transition from a finance and REIT-heavy fund to an all-weather fund with less volatility.

The SRS Fund is up 4.75% year to date versus the STI negative 1%. With the normalisation of the yield curve especially on the long end starting to work its way up, I expect volatility to heighten as we enter into October.

The SRS fund recorded 2 notable transactions in the month of September. First, is a new foray into the manufacturing segment with Venture Corp. Venture is not a new name on the scene and has a proven track record of delivering respectable high return on invested capital. With a strong balance sheet and an experienced management team, I trust that Venture’s investment me

Second, I have cut half of the Funds position in SATS. Despite being bullish on the revenge travel theme, I quickly realised a mistake was made in position sizing. Statistically most mergers fail and this is especially so for a company that made an acquisition that is much bigger than itself.

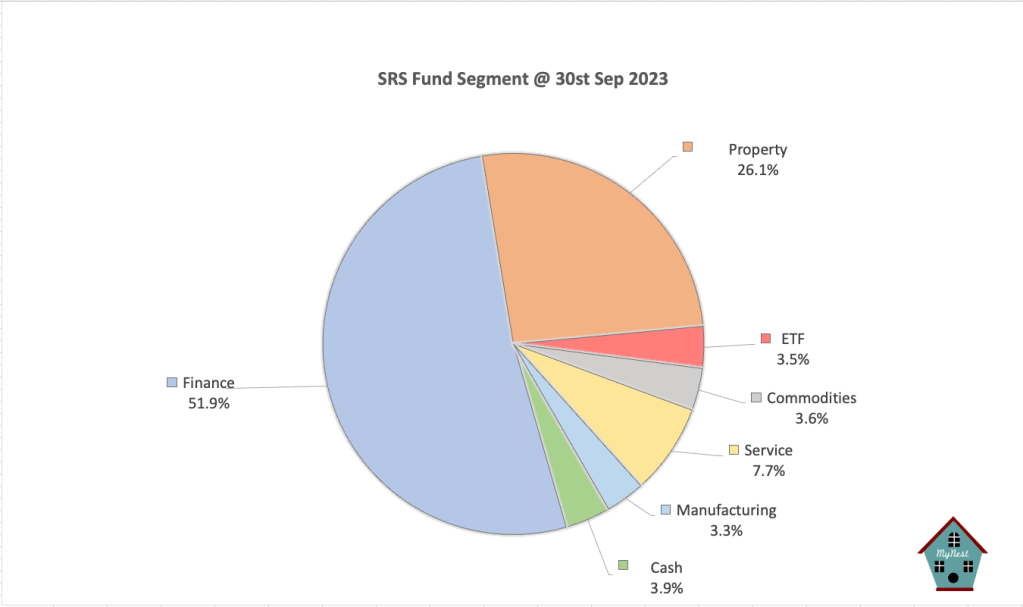

Portfolio Segments

Investors can see the diversification in the works. Despite being heavily invested in local banks, the SRS fund managed to trim its REITs position decisively when Mr Market was in a good mood. This reduced the REITs composition to less than 20% of the SRS Fund under the property segment thus reducing the drag on performance.

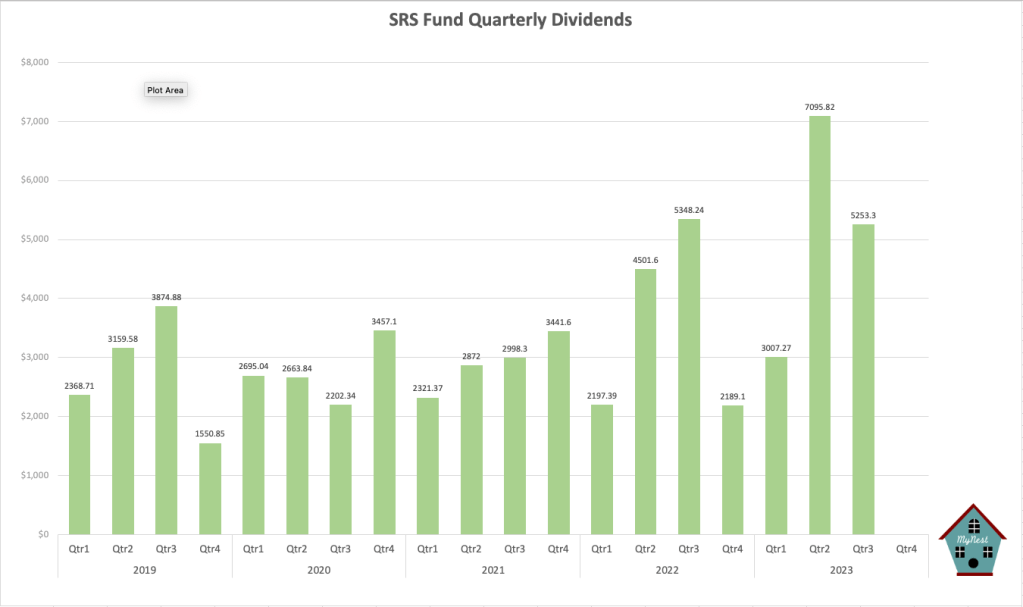

Dividends

The dividend received at the end of Sep stood at $5253.30 and is comparable to the same quarter in 2022. The SRS fund is on course to receive record dividends with no reduction in portfolio value which not many investors can boast about in this climate of rising interest rates.

SRS Fund Value

The SRS Fund shrank slightly to $373,241.15 in the month of September. Weakness in the general market continues to soften the fund as of this writing. I expect the fund value to remain at current levels until the end of the year. With Q3 earnings reporting coming up, I would again expect local banks to announce stellar results with REITs further cutting DPU and businesses trying to pass on cost inflation to their customers.

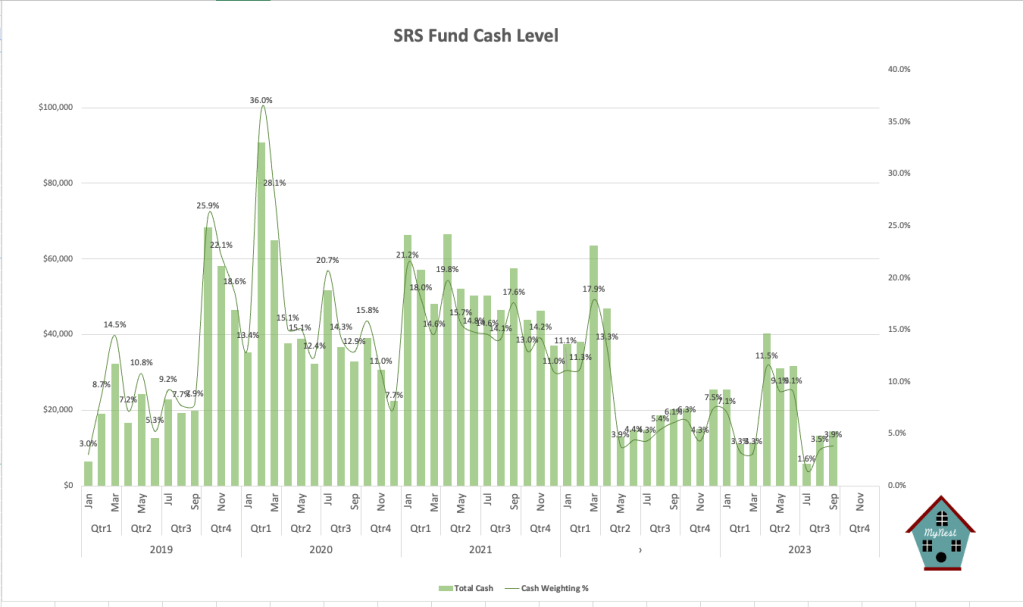

Cash Levels

Cash level rose after selling half of the fund’s position in SATS. I will look out for further opportunities to cash out underperforming positions as the rise in long-term interest rates is starting to offer a compelling alternative like holding cash in the portfolio.

-

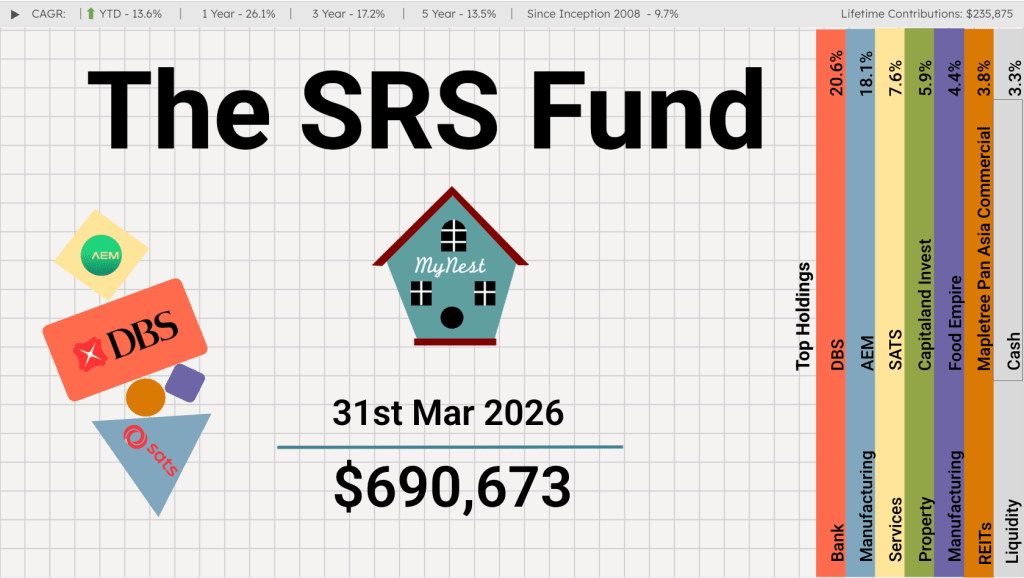

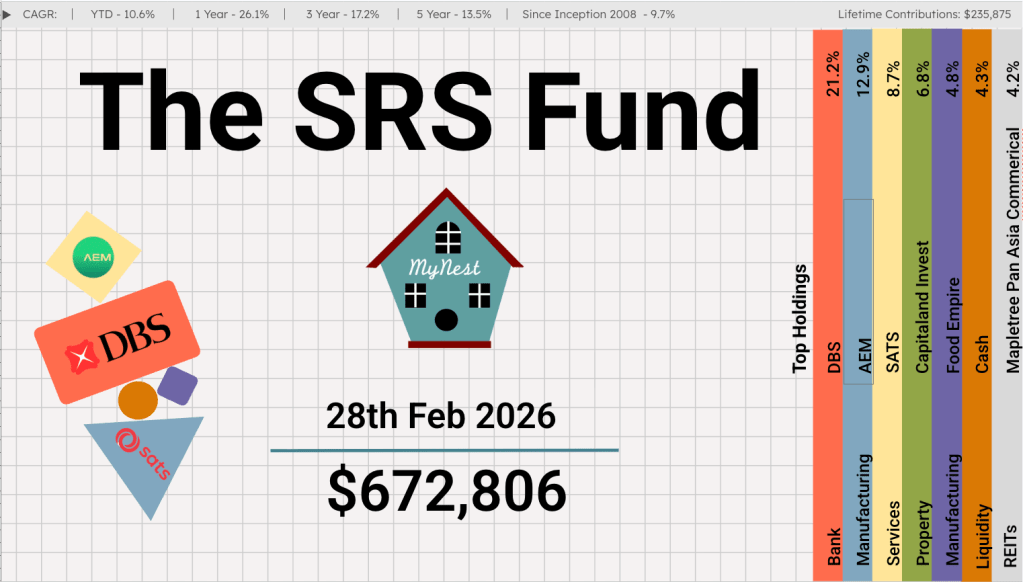

The SRS Fund Mar 2026

It is an enduring market reality that a concentrated minority of holdings drives the vast majority of returns. For years, DBS (currently the largest individual holding at 20.6%) has served as the compounding engine of the SRS Fund.

-

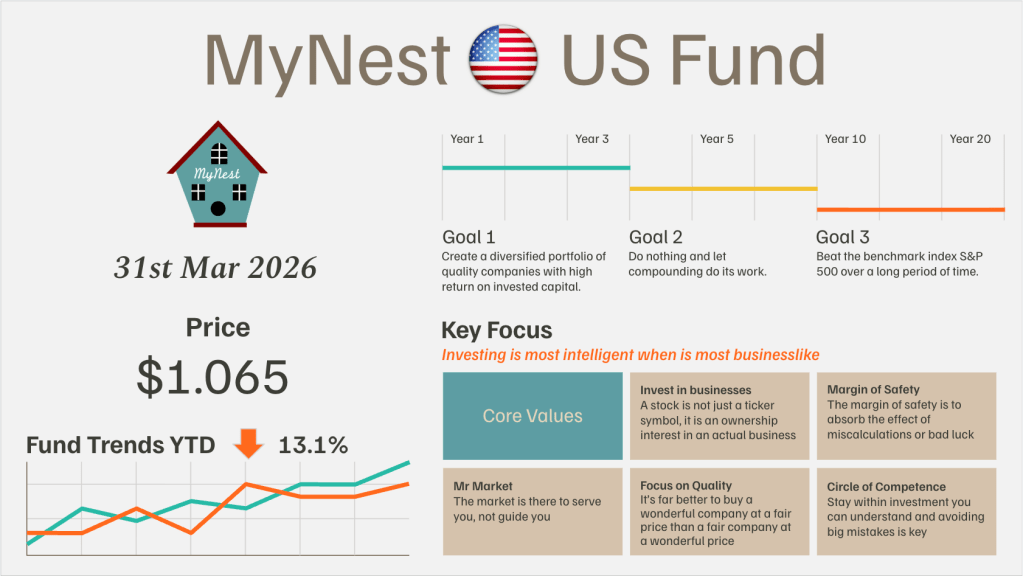

MyNest US Fund Mar 26

March shattered any lingering market complacency, pivoting sharply from the localized damage of the “SaaS-pocalypse” to a systemic shock driven by the war in Iran.

-

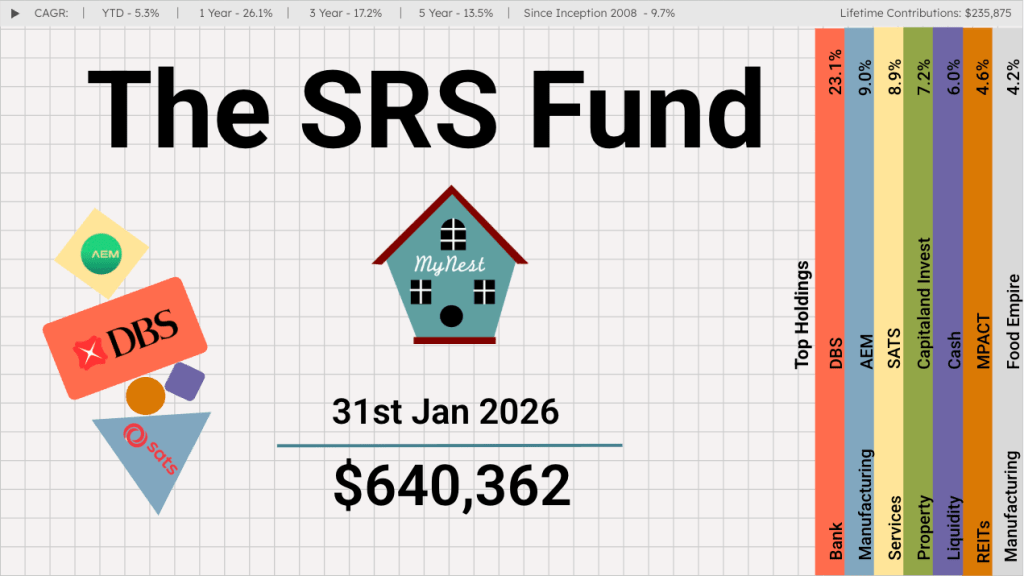

The SRS Fund Feb 2026

The Singapore Budget 2026 has set a robust backdrop for local investors. For the third consecutive year, the government is operating from a position of immense “dry powder,” with an overall fiscal surplus of $8.5 billion projected for FY2026.

-

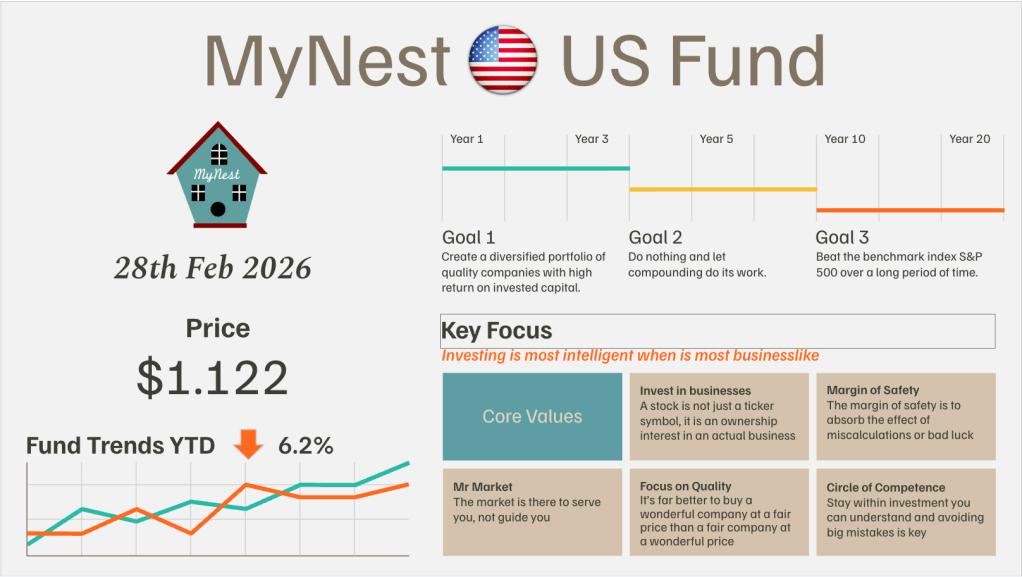

MyNest US Fund Feb 26

February 2026 proved to be one of the most challenging months for our fund since its inception. A wave of “AI anxiety” swept through the Software-as-a-Service (SaaS) sector

-

The SRS Fund Jan 2026

After a blockbuster 2025 that saw GDP growth hit a surprise 4.8%, the first month of 2026 has proven that the momentum is far from a fluke. Between record-breaking stock market performance and massive industrial investments, the “Little Red Dot” is making a very big noise.

-

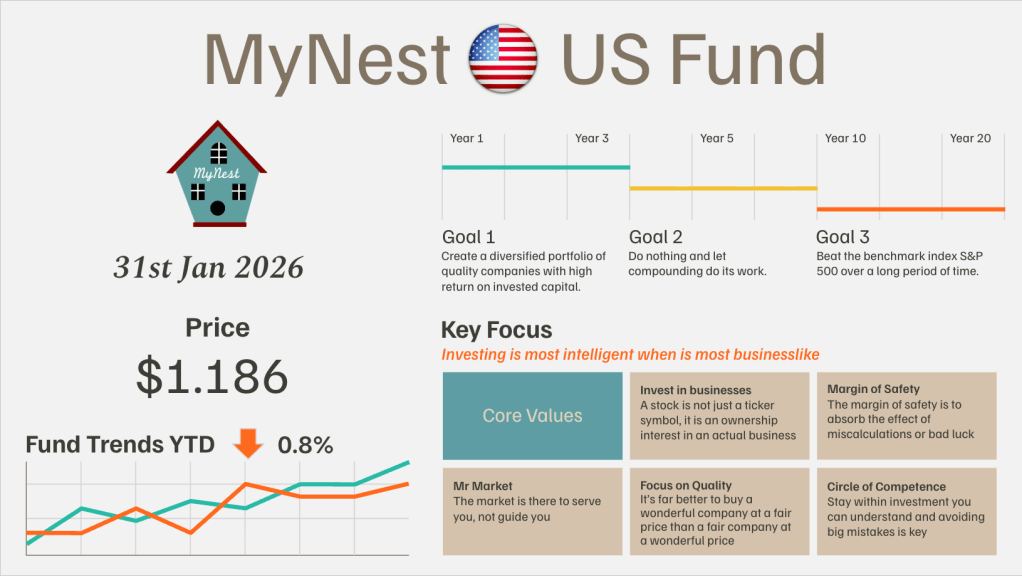

MyNest US Fund Jan 26

I have a confession to make. After reading Chip War at the end of 2022, I fully grasped the strategic importance of TSMC and ASML in the global semiconductor supply chain.