October October

If there is one particular month to deploy cash this would be the month. The SRS Fund was not spared as the traditional blood-letting month lived up to its name bringing the SRS fund back into slight negative territory for the year.

The SRS Fund is down 1.15% year to date versus the STI negative 5.64%. While the fund held onto its lead against the index there is little to celebrate as long-term yield spike during the month threatening to normalise the yield curve.

It was only after the Federal Reserves signaled the likely end to rate hikes that gave much comfort to the market as yields pulled back from their all-time highs. As such, the market began to rally shortly into November with all yield-sensitive stocks like REITs making a strong rebound.

There are however no activities for the SRS Funds in October despite the amount of blood on the street as I aim to start building a reasonable cash buffer for the fund while interest rates remains elevated.

Portfolio Segments

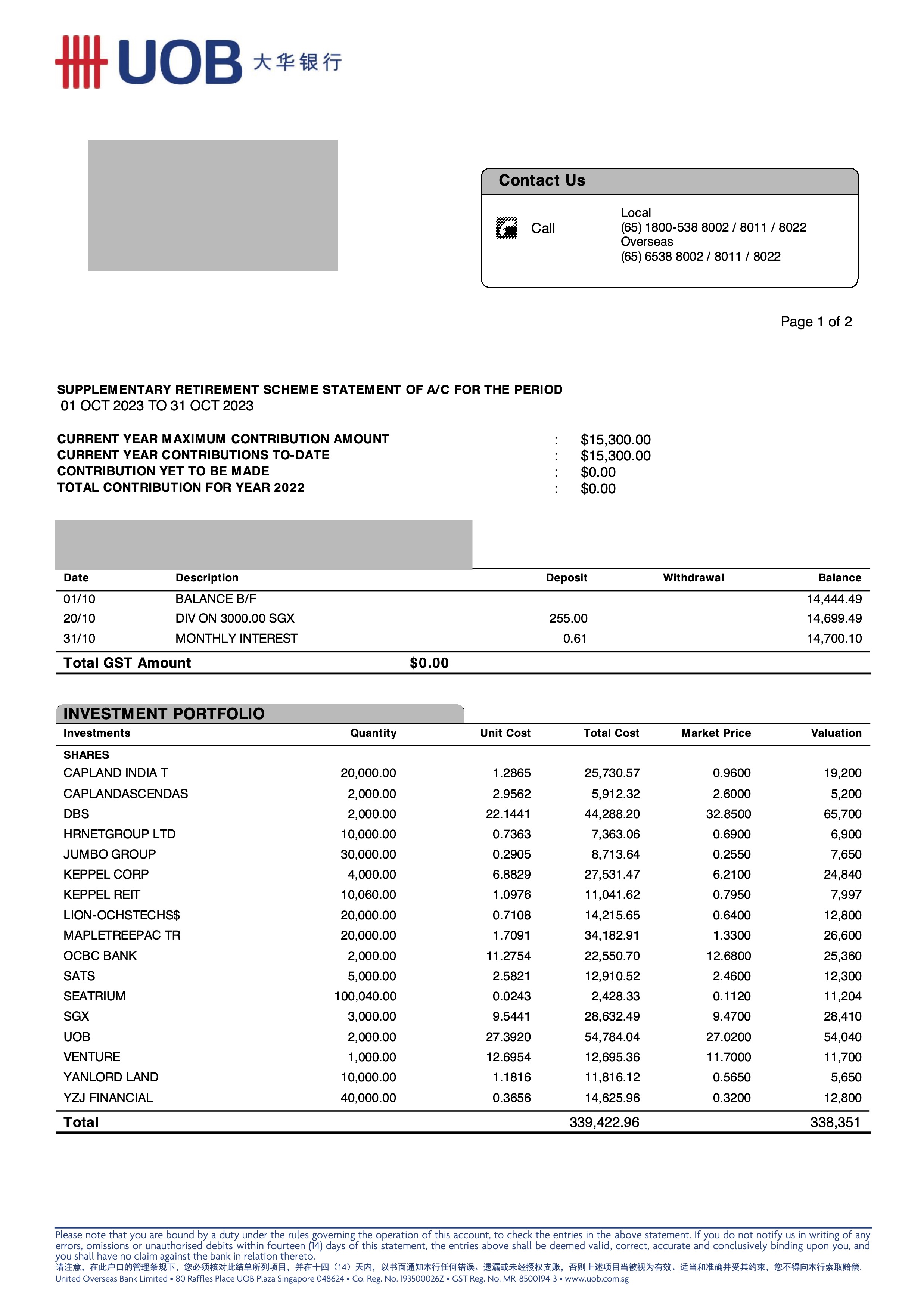

Portfolio allocation remains heavy in the finance sector as the outlook on banks remains much brighter than most other segments. Going forward however cash resources will be allocated towards non finance sector due to this overweighting.

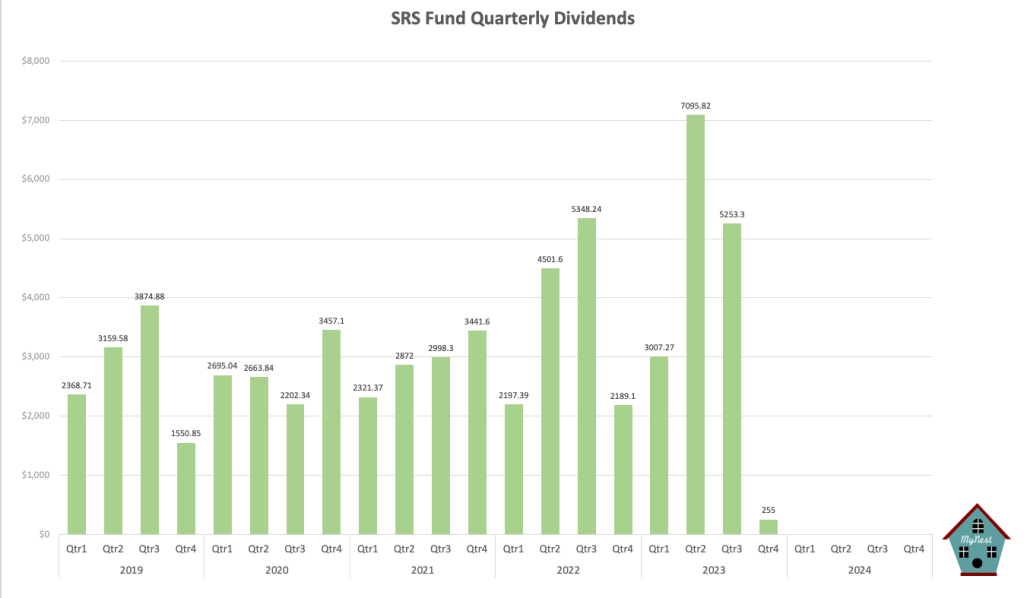

Dividends

A mere $255 of dividend was received in October from SGX. However, I would expect a record Q4 dividend judging by up and coming announced dividends.

SRS Fund Value

The SRS Fund value plummeted to $353,052.28 in the month making this pullback one of the steepest for the fund in the last 5 years.

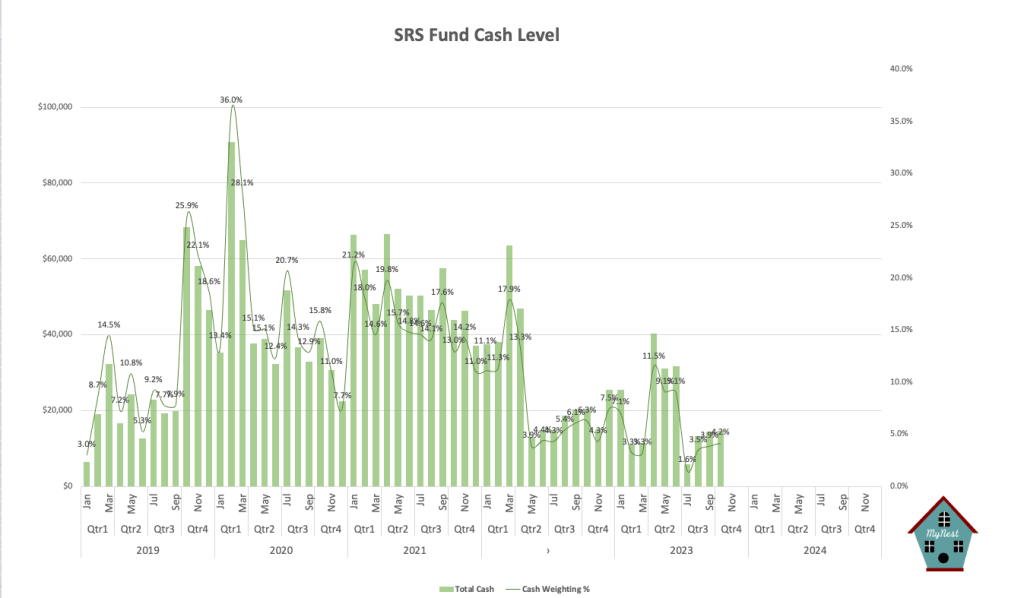

Cash Levels

Cash level should continue to rise as I start to build up a significant cash buffer with a yield in the range of 4%. My initial cash target for the SRS Fund would be in the region of 10% for cash if no good opportunity arises.

Many investors will be relieved by the sudden change in yield pressure however, I do not see any upcoming interest rate cut anytime soon. Sure inflation should come down somewhat but one should not expect rates to go back down to ultra-low levels like what we have seen in the past 2 decades.

-

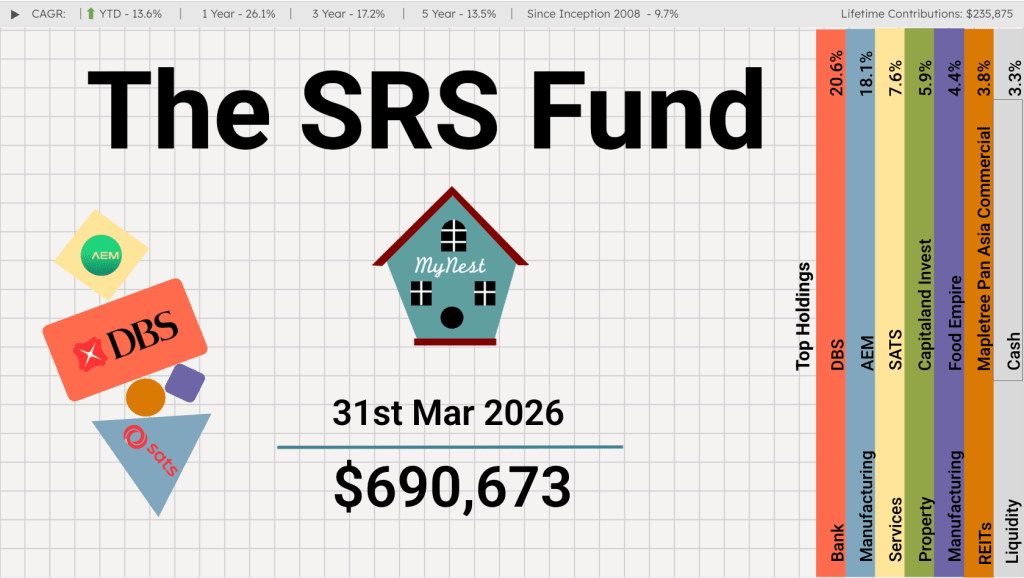

The SRS Fund Mar 2026

It is an enduring market reality that a concentrated minority of holdings drives the vast majority of returns. For years, DBS (currently the largest individual holding at 20.6%) has served as the compounding engine of the SRS Fund.

-

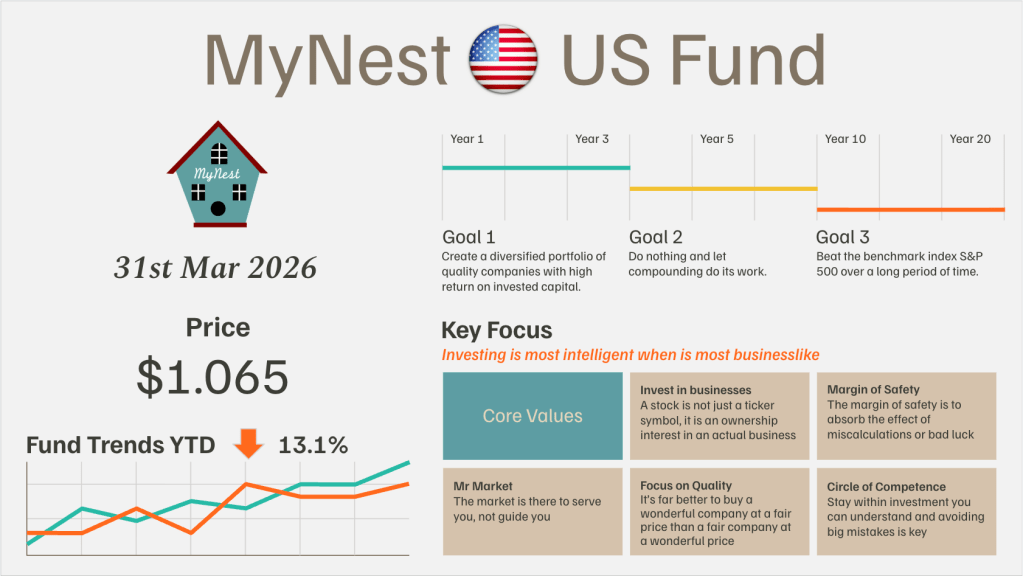

MyNest US Fund Mar 26

March shattered any lingering market complacency, pivoting sharply from the localized damage of the “SaaS-pocalypse” to a systemic shock driven by the war in Iran.

-

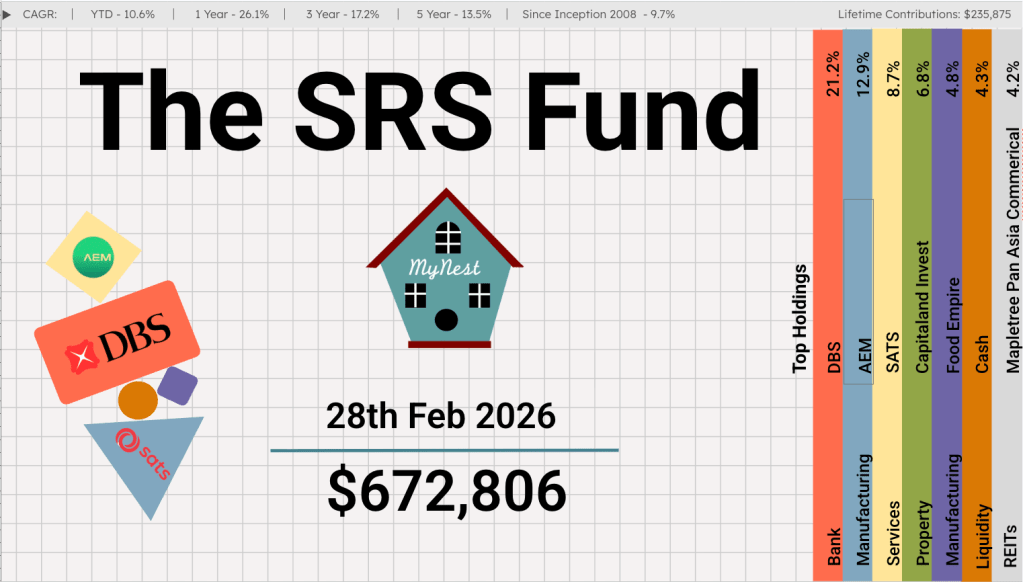

The SRS Fund Feb 2026

The Singapore Budget 2026 has set a robust backdrop for local investors. For the third consecutive year, the government is operating from a position of immense “dry powder,” with an overall fiscal surplus of $8.5 billion projected for FY2026.

-

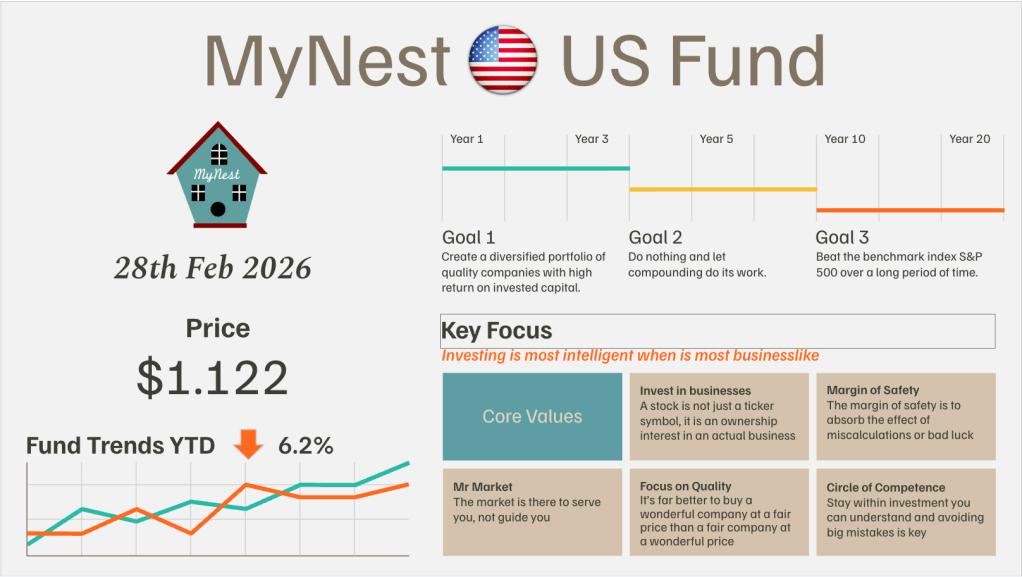

MyNest US Fund Feb 26

February 2026 proved to be one of the most challenging months for our fund since its inception. A wave of “AI anxiety” swept through the Software-as-a-Service (SaaS) sector

-

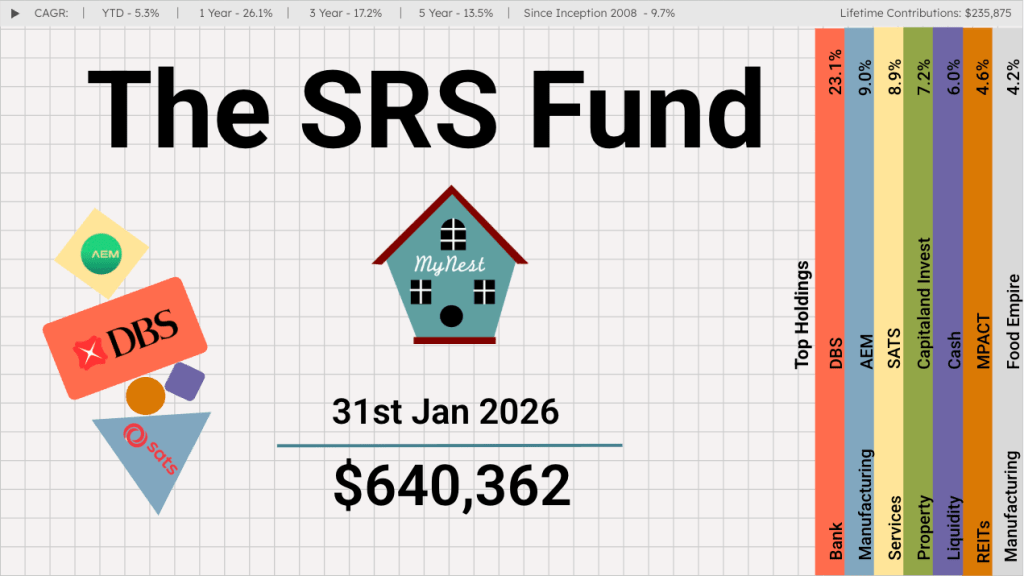

The SRS Fund Jan 2026

After a blockbuster 2025 that saw GDP growth hit a surprise 4.8%, the first month of 2026 has proven that the momentum is far from a fluke. Between record-breaking stock market performance and massive industrial investments, the “Little Red Dot” is making a very big noise.

-

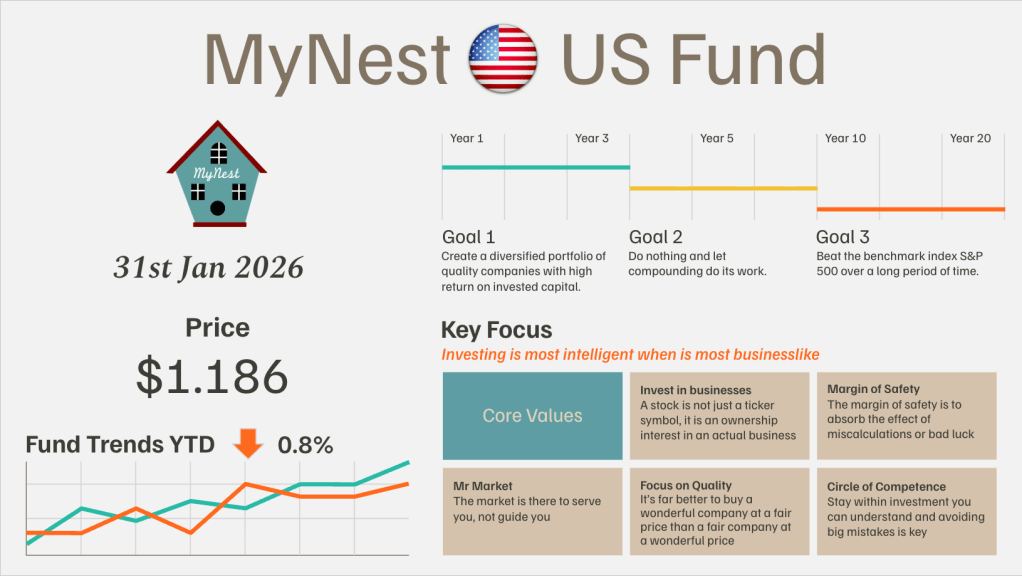

MyNest US Fund Jan 26

I have a confession to make. After reading Chip War at the end of 2022, I fully grasped the strategic importance of TSMC and ASML in the global semiconductor supply chain.