Singapore Budget – A Position of Strength

The Singapore Budget 2026 has set a robust backdrop for local investors. For the third consecutive year, the government is operating from a position of immense “dry powder,” with an overall fiscal surplus of $8.5 billion projected for FY2026.

Strategic Spending Enabled by Surplus

What is most encouraging for the SRS fund is the transition from pandemic-era recovery to future-focused investment. Enabled by a massive $15.1 billion surplus in FY2025, the government has announced a significant 10% hike in total expenditure to $137.3 billion.

Capital Availability: With $1.5 billion added to the Anchor Fund to support local listings, the macro environment is increasingly supportive of the mid-to-large-cap Singapore companies we hold.

AI & Tech Focus: The budget’s heavy emphasis on AI—including the new “National AI Missions”—perfectly validates the SRS fund’s heavy tilt toward the technology and semiconductor sectors.

AEM Holdings: The Multi-Year Upcycle

The SRS Fund investment in AEM Holdings reached a pivotal inflection point this month. While it has been a volatile journey, the thesis we built around HBM4 (High Bandwidth Memory) and customer diversification is now delivering.

Deep Dive: Margin Expansion & Execution

The market has correctly identified AEM’s potential for HBM4 testing, but the real story for 2026 is margin expansion.

- The HBM4 Edge: Traditional testing cannot handle the thermal complexity of next-gen AI chips. AEM’s proprietary thermal control and “Test Cell Solutions 2.0” allow for asynchronous testing, which carries significantly higher margins than standard commoditized testing.

- The New Customer (AMD): Securing a second major customer (widely understood to be AMD) alongside their original customer (Intel) is the single biggest de-risking event in years.

- The Micron Catalyst: Unlike the logic-chip giants, Micron represents AEM’s entry into the high-volume memory testing market. AEM is currently in the late stages of customer validation for its memory test solutions, with initial production shipments slated for late FY2026.

- HBM4 Margin Expansion: Traditional testing cannot handle the thermal complexity of HBM4. AEM’s proprietary thermal control technology allows for higher testing yields. As Micron ramps up its $9.5 billion HBM facility in Singapore, AEM is perfectly positioned as the local “on-shore” testing partner.

- FY2026: The Year of Execution: With revenue guidance set at $460M–$510M, the economies of scale will finally allow AEM to convert a larger slice of revenue into bottom-line profit.

SRS Fund Performance vs. Benchmark

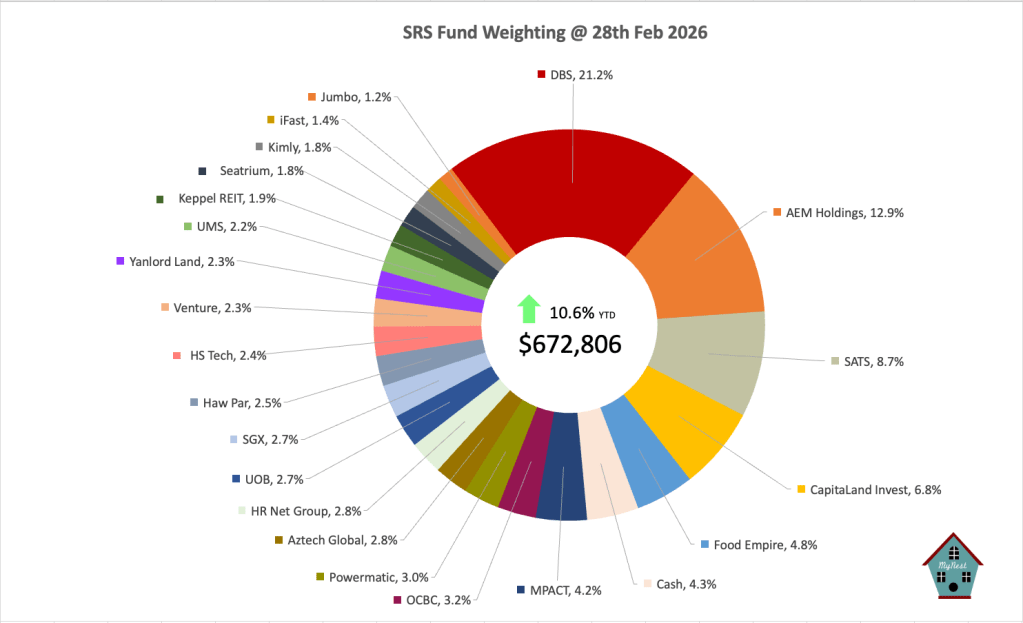

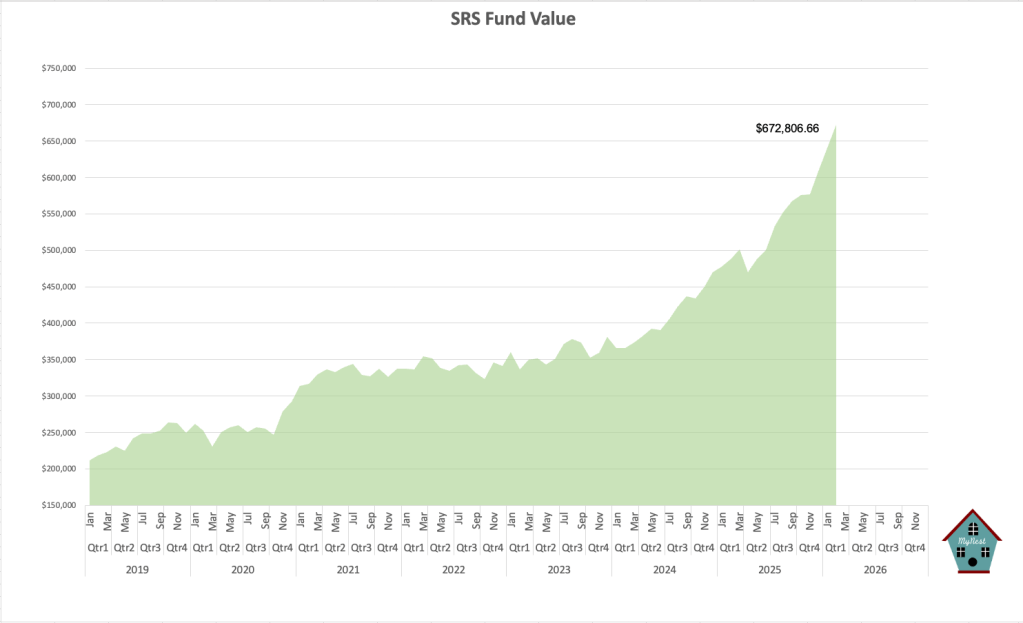

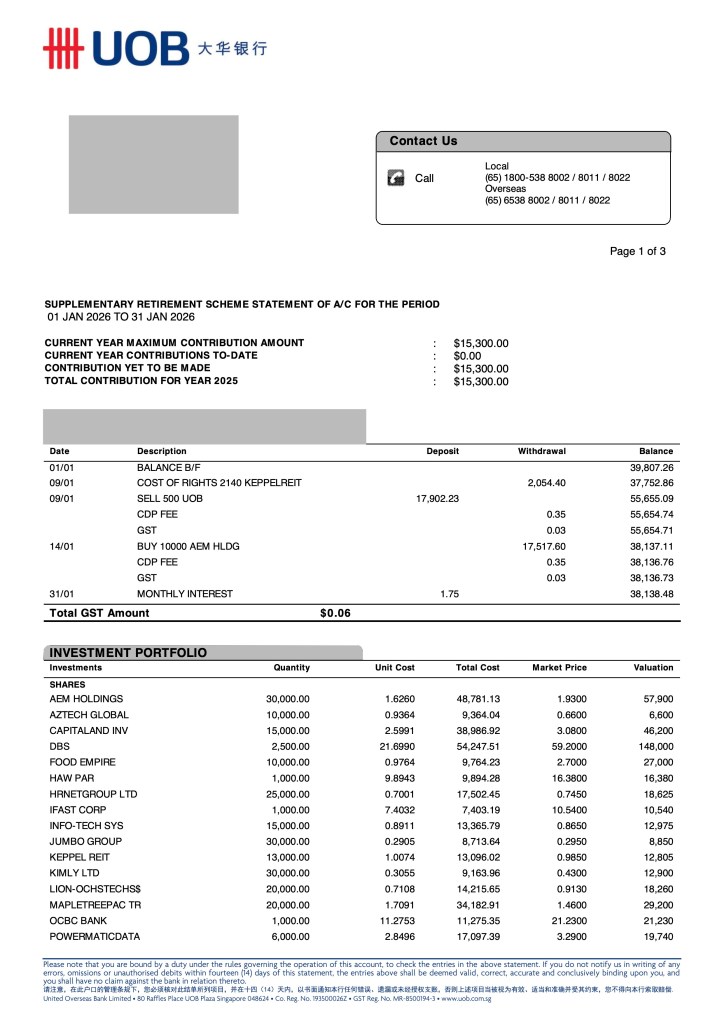

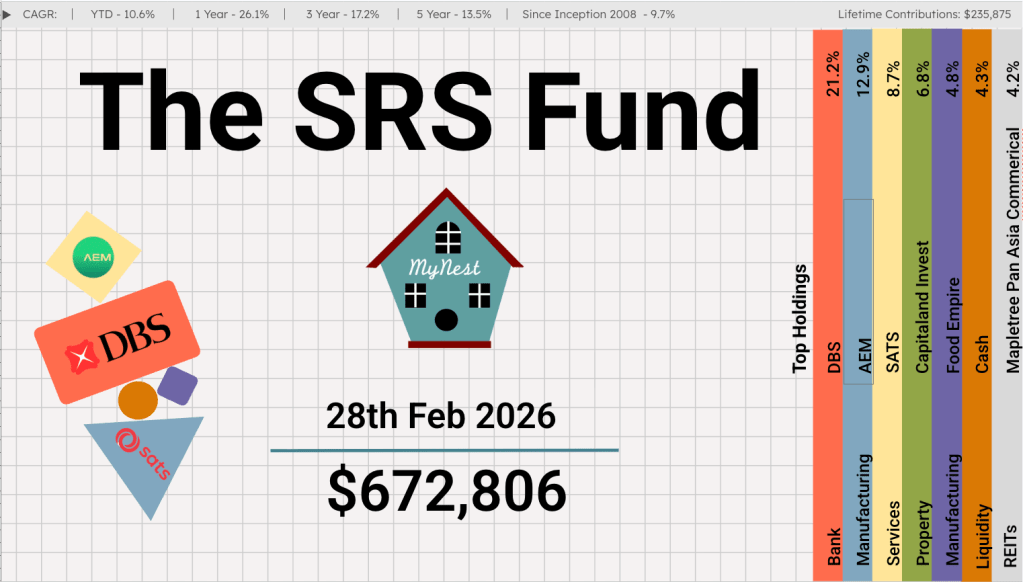

The SRS Fund reached a new milestone this month, with the total value hitting $672,806.

Performance Comparison

I am pleased to report that the fund is currently outperforming the benchmark Straits Times Index (STI). While the STI has had a historic run—crossing the 5,000-point psychological barrier for the first time in February 2026—the SRS Fund’s concentration in high-growth tech has given us the edge.

| Metric | The SRS Fund | STI Index (Benchmark) |

| YTD Return (Feb 2026) | +10.6% | ~+5.8% |

| Cash Weighting | 4.3% | N/A |

| Top Holding | DBS (21.2%) | DBS (~24.6%) |

Why We Are Outperforming

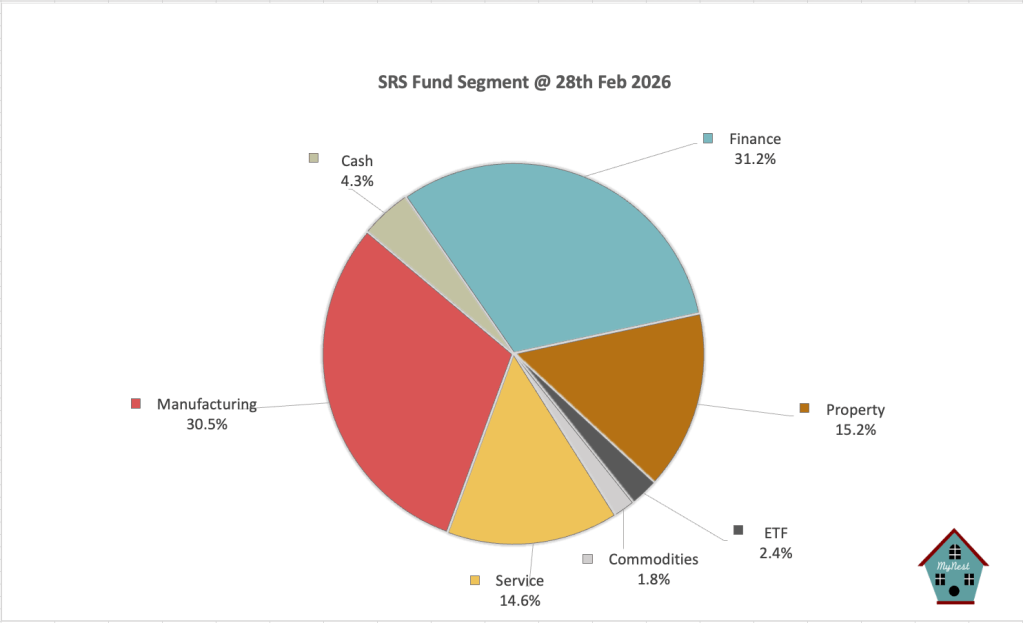

While the STI’s rally has been largely driven by the “Big Three” banks (making up over 50% of the index), our outperformance stems from our Manufacturing segment (30.5%). By holding a larger weight in AEM Holdings and SATS compared to the index, we have captured the extra Alpha that the broader, more bank-heavy STI lacks.

Portfolio Segments

Finance (31.2%): The Resilience of DBS

With the 3-month SORA bottoming near 1.0% in early 2026, the era of easy Net Interest Margin (NIM) expansion for banks is over. However, we remain overweight in DBS (21.2%) for two reasons:

- Fee Income over Interest: DBS is successfully pivotting. Wealth management fees and treasury sales now offset NIM compression. In Q4 2025, wealth AUM hit a record $488 billion, growing 19%.

- Dividend Visibility: Despite “rate headwinds,” DBS has committed to maintaining its $0.15 capital return dividend through 2026 and 2027, providing a yield of ~6%—a massive spread over T-bills.

Manufacturing (30.5%): Our Alpha Engine

This segment, led by AEM Holdings (12.9%), is now our primary driver of capital appreciation. We are seeing a “K-shaped” recovery where tech-heavy manufacturing is far outperforming traditional industrial sectors.

Dividends

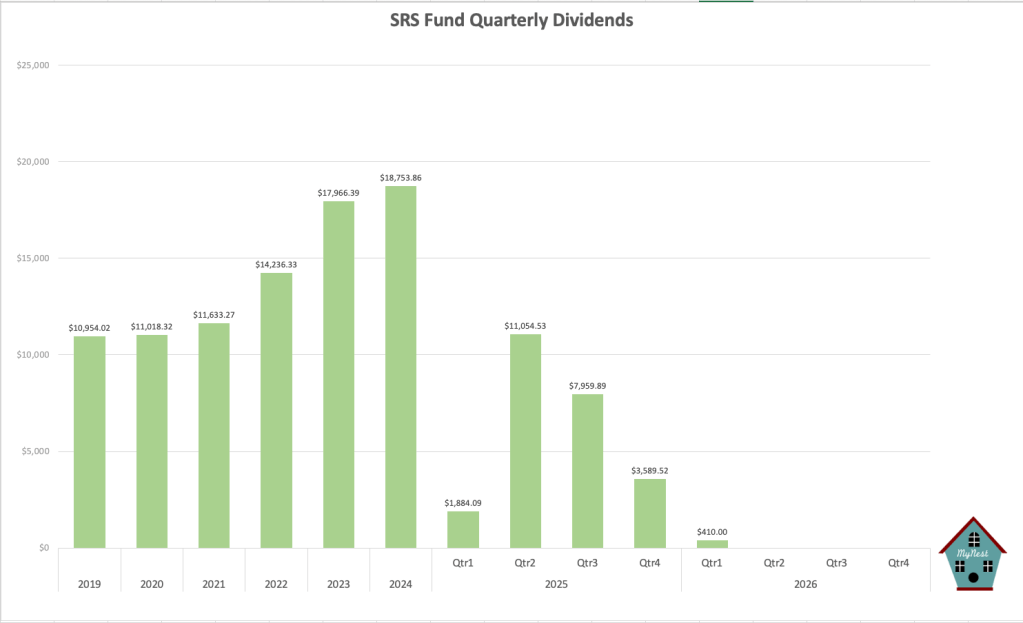

Q1 is generally a slow period for dividend collection. With only $410 so far in the first 2 months of the year. Nevertheless, I look forward to another year of near $20k of dividend for the SRS Fund

SRS Fund Value

The SRS Fund has reached a significant milestone, with its total value climbing to $672,806.66 as of February 2026. This performance represents a robust 10.6% YTD return, driven by a strategic pivot toward high-growth manufacturing and resilient financial anchors.

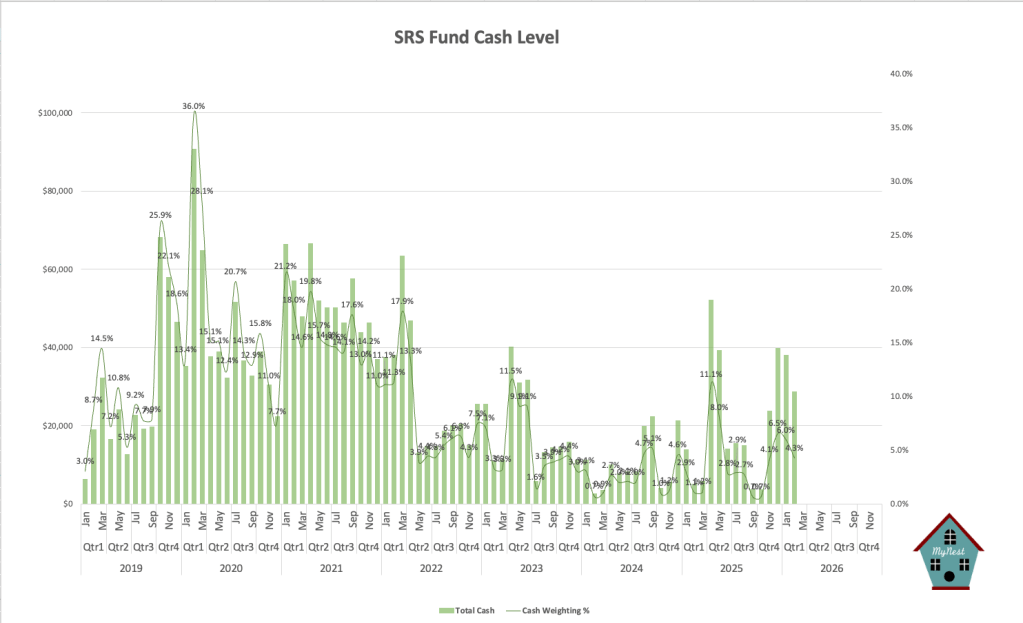

Cash Levels

The SRS Fund currently maintain a lean cash level of 4.3% ($28,738). This “fully loaded” stance allows us to maximize exposure to the ongoing AI and semiconductor upcycle, ensuring our capital is working as hard as possible in a supportive macro environment.

The fund continues to outperform the benchmark STI Index, proving that a concentrated, thematic approach within the SRS framework is a powerful tool for long-term compounding.

-

The SRS Fund Feb 2026

The Singapore Budget 2026 has set a robust backdrop for local investors. For the third consecutive year, the government is operating from a position of immense “dry powder,” with an overall fiscal surplus of $8.5 billion projected for FY2026.

-

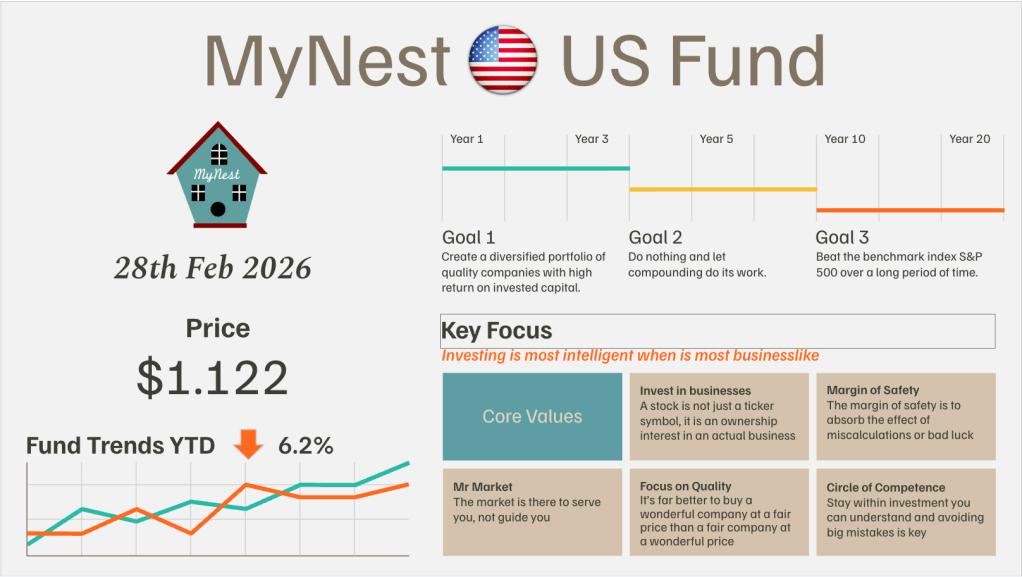

MyNest US Fund Jan 26

February 2026 proved to be one of the most challenging months for our fund since its inception. A wave of “AI anxiety” swept through the Software-as-a-Service (SaaS) sector

-

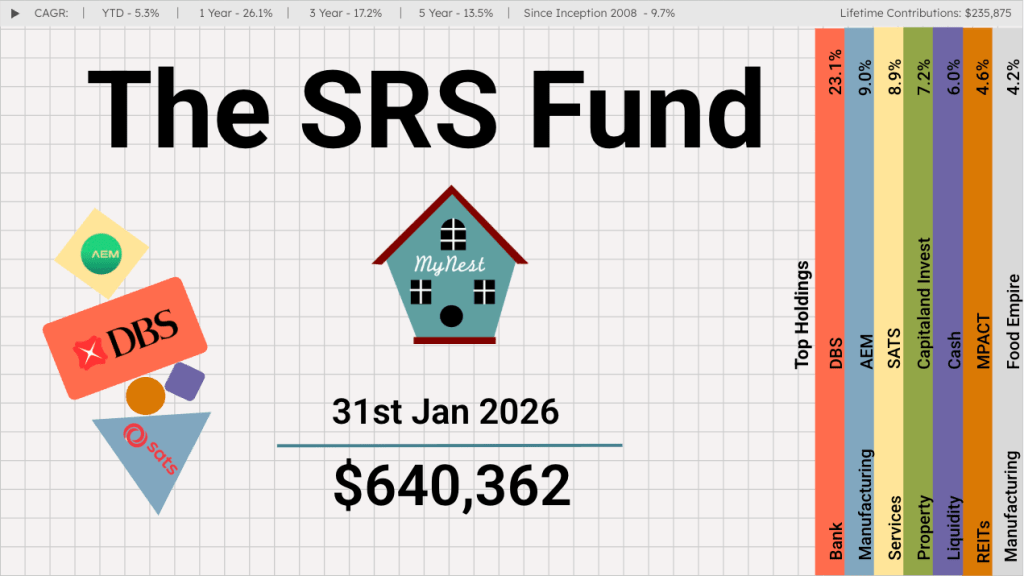

The SRS Fund Jan 2026

After a blockbuster 2025 that saw GDP growth hit a surprise 4.8%, the first month of 2026 has proven that the momentum is far from a fluke. Between record-breaking stock market performance and massive industrial investments, the “Little Red Dot” is making a very big noise.

-

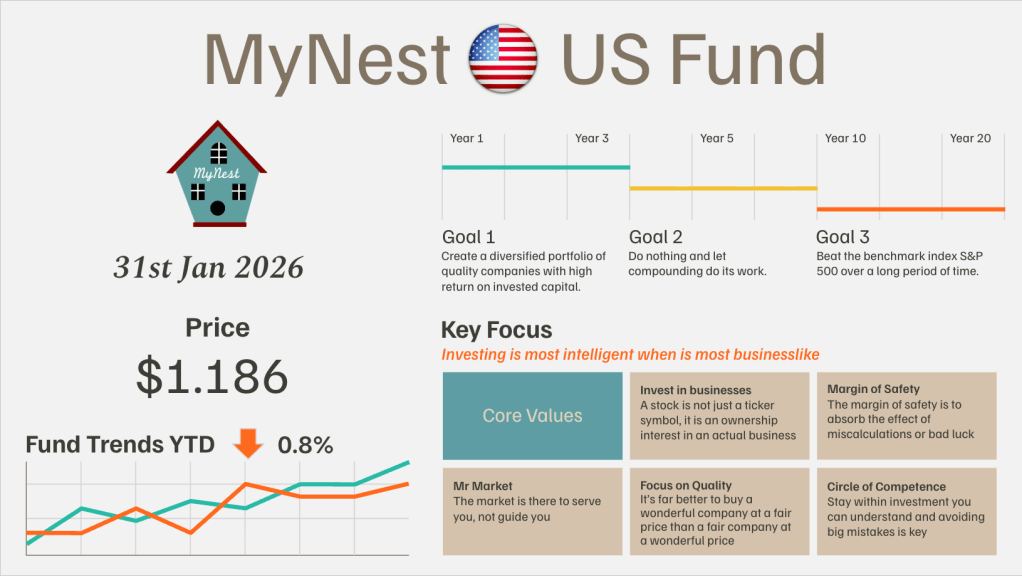

MyNest US Fund Jan 26

I have a confession to make. After reading Chip War at the end of 2022, I fully grasped the strategic importance of TSMC and ASML in the global semiconductor supply chain.

-

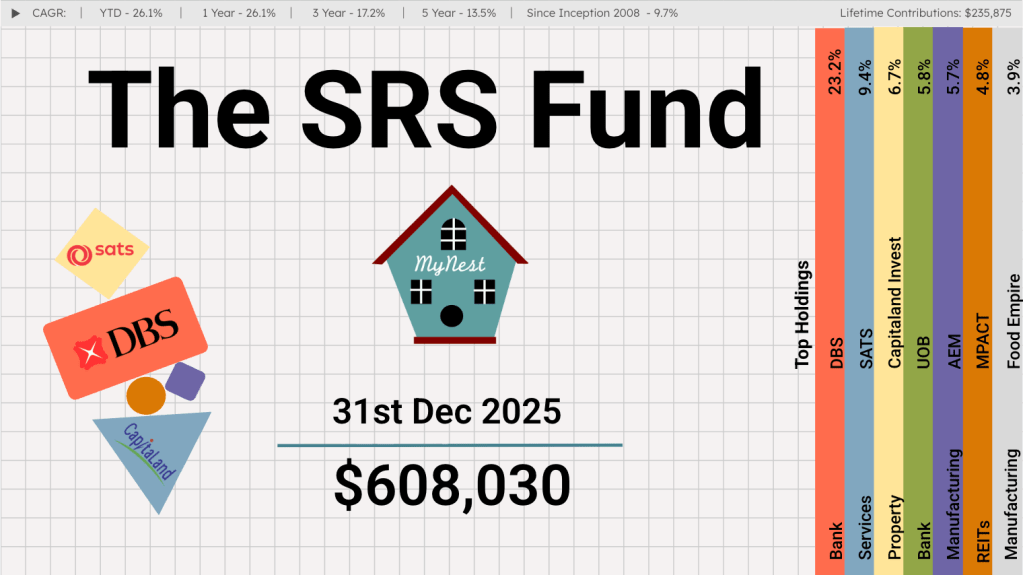

The SRS Fund Dec 2025

If someone had told me at the start of the year that the Singapore stock market would deliver returns in excess of 20%, I would have shrugged it off as wishful thinking.

-

MyNest US Fund Dec 25

MyNest US Fund rounded the first year of inception with a slight outperformance to our benchmark the S&P 500. The first year of operation tested to resolve in knowing what we own as we navigated volatility which started on Trump’s Liberation Day.