Singapore Budget – A Position of Strength

The Singapore Budget 2026 has set a robust backdrop for local investors. For the third consecutive year, the government is operating from a position of immense “dry powder,” with an overall fiscal surplus of $8.5 billion projected for FY2026.

Strategic Spending Enabled by Surplus

What is most encouraging for the SRS fund is the transition from pandemic-era recovery to future-focused investment. Enabled by a massive $15.1 billion surplus in FY2025, the government has announced a significant 10% hike in total expenditure to $137.3 billion.

Capital Availability: With $1.5 billion added to the Anchor Fund to support local listings, the macro environment is increasingly supportive of the mid-to-large-cap Singapore companies we hold.

AI & Tech Focus: The budget’s heavy emphasis on AI—including the new “National AI Missions”—perfectly validates the SRS fund’s heavy tilt toward the technology and semiconductor sectors.

AEM Holdings: The Multi-Year Upcycle

The SRS Fund investment in AEM Holdings reached a pivotal inflection point this month. While it has been a volatile journey, the thesis we built around HBM4 (High Bandwidth Memory) and customer diversification is now delivering.

Deep Dive: Margin Expansion & Execution

The market has correctly identified AEM’s potential for HBM4 testing, but the real story for 2026 is margin expansion.

- The HBM4 Edge: Traditional testing cannot handle the thermal complexity of next-gen AI chips. AEM’s proprietary thermal control and “Test Cell Solutions 2.0” allow for asynchronous testing, which carries significantly higher margins than standard commoditized testing.

- The New Customer (AMD): Securing a second major customer (widely understood to be AMD) alongside their original customer (Intel) is the single biggest de-risking event in years.

- The Micron Catalyst: Unlike the logic-chip giants, Micron represents AEM’s entry into the high-volume memory testing market. AEM is currently in the late stages of customer validation for its memory test solutions, with initial production shipments slated for late FY2026.

- HBM4 Margin Expansion: Traditional testing cannot handle the thermal complexity of HBM4. AEM’s proprietary thermal control technology allows for higher testing yields. As Micron ramps up its $9.5 billion HBM facility in Singapore, AEM is perfectly positioned as the local “on-shore” testing partner.

- FY2026: The Year of Execution: With revenue guidance set at $460M–$510M, the economies of scale will finally allow AEM to convert a larger slice of revenue into bottom-line profit.

SRS Fund Performance vs. Benchmark

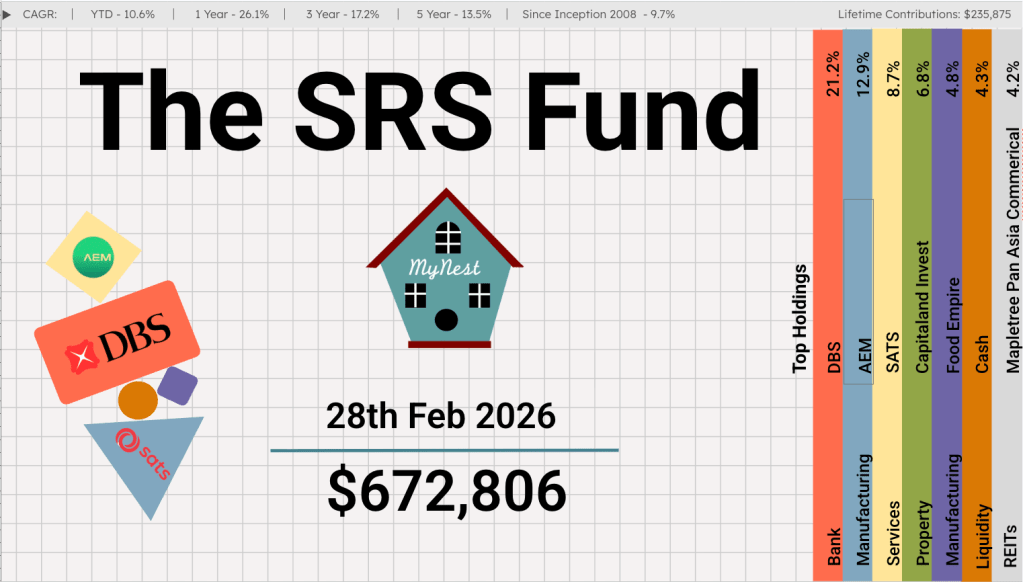

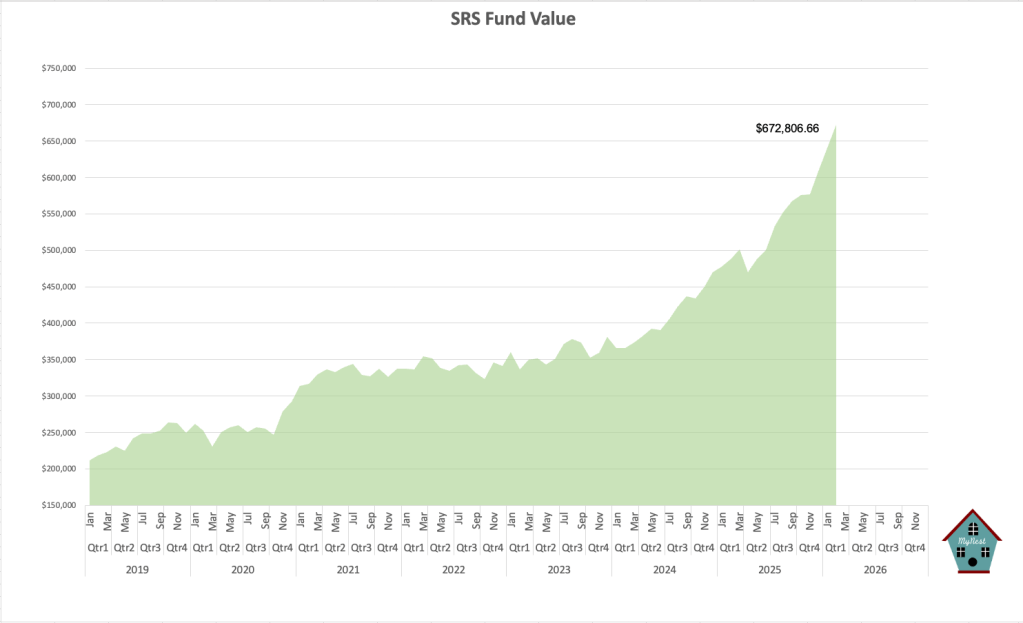

The SRS Fund reached a new milestone this month, with the total value hitting $672,806.

Performance Comparison

I am pleased to report that the fund is currently outperforming the benchmark Straits Times Index (STI). While the STI has had a historic run—crossing the 5,000-point psychological barrier for the first time in February 2026—the SRS Fund’s concentration in high-growth tech has given us the edge.

| Metric | The SRS Fund | STI Index (Benchmark) |

| YTD Return (Feb 2026) | +10.6% | ~+5.8% |

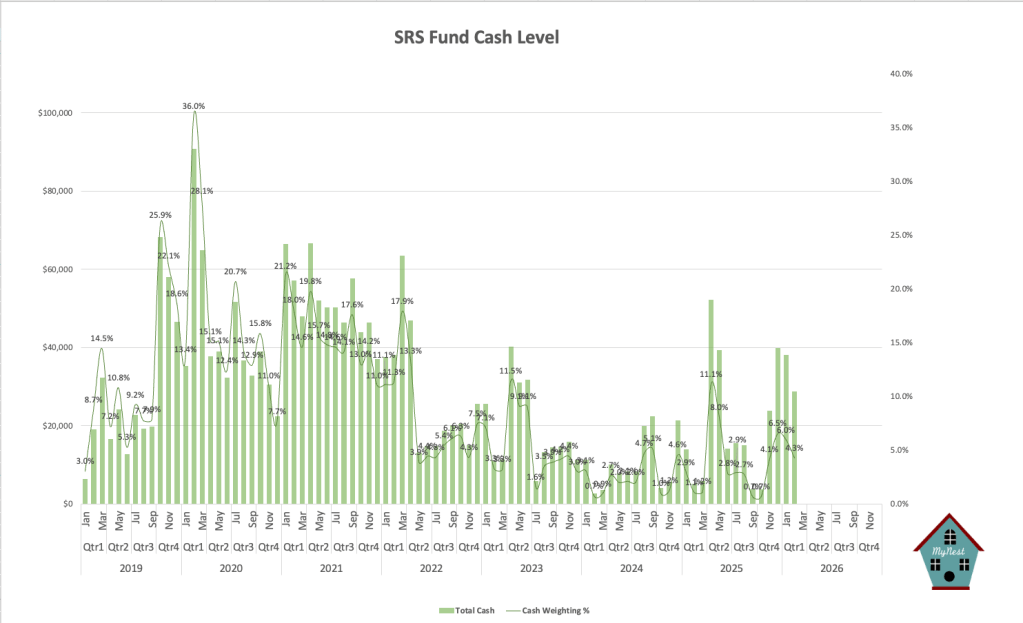

| Cash Weighting | 4.3% | N/A |

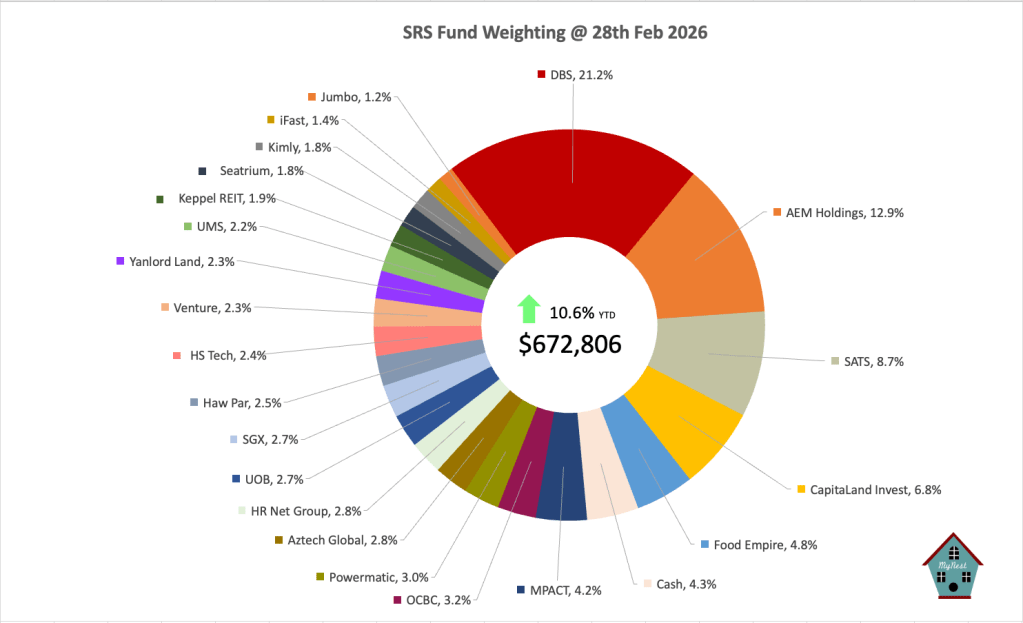

| Top Holding | DBS (21.2%) | DBS (~24.6%) |

Why We Are Outperforming

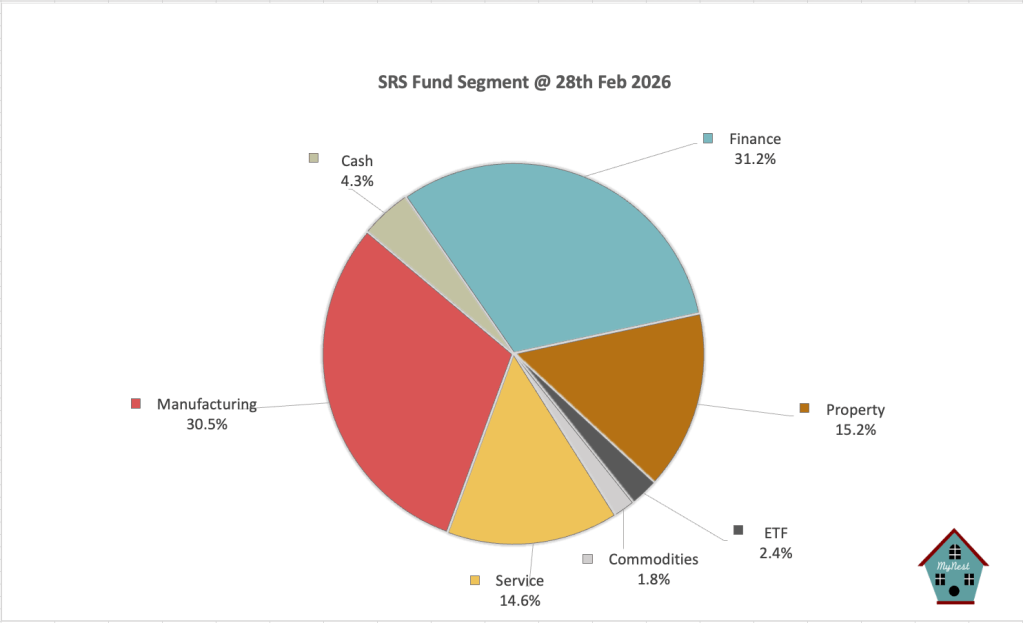

While the STI’s rally has been largely driven by the “Big Three” banks (making up over 50% of the index), our outperformance stems from our Manufacturing segment (30.5%). By holding a larger weight in AEM Holdings and SATS compared to the index, we have captured the extra Alpha that the broader, more bank-heavy STI lacks.

Portfolio Segments

Finance (31.2%): The Resilience of DBS

With the 3-month SORA bottoming near 1.0% in early 2026, the era of easy Net Interest Margin (NIM) expansion for banks is over. However, we remain overweight in DBS (21.2%) for two reasons:

- Fee Income over Interest: DBS is successfully pivotting. Wealth management fees and treasury sales now offset NIM compression. In Q4 2025, wealth AUM hit a record $488 billion, growing 19%.

- Dividend Visibility: Despite “rate headwinds,” DBS has committed to maintaining its $0.15 capital return dividend through 2026 and 2027, providing a yield of ~6%—a massive spread over T-bills.

Manufacturing (30.5%): Our Alpha Engine

This segment, led by AEM Holdings (12.9%), is now our primary driver of capital appreciation. We are seeing a “K-shaped” recovery where tech-heavy manufacturing is far outperforming traditional industrial sectors.

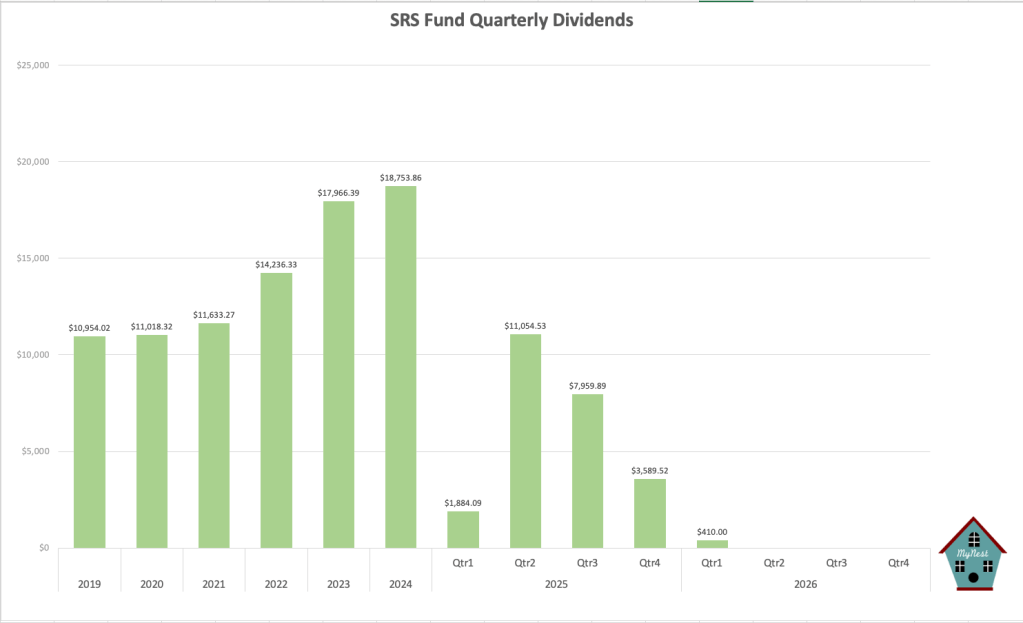

Dividends

Q1 is generally a slow period for dividend collection. With only $410 so far in the first 2 months of the year. Nevertheless, I look forward to another year of near $20k of dividend for the SRS Fund

SRS Fund Value

The SRS Fund has reached a significant milestone, with its total value climbing to $672,806.66 as of February 2026. This performance represents a robust 10.6% YTD return, driven by a strategic pivot toward high-growth manufacturing and resilient financial anchors.

Cash Levels

The SRS Fund currently maintain a lean cash level of 4.3% ($28,738). This “fully loaded” stance allows us to maximize exposure to the ongoing AI and semiconductor upcycle, ensuring our capital is working as hard as possible in a supportive macro environment.

The fund continues to outperform the benchmark STI Index, proving that a concentrated, thematic approach within the SRS framework is a powerful tool for long-term compounding.

-

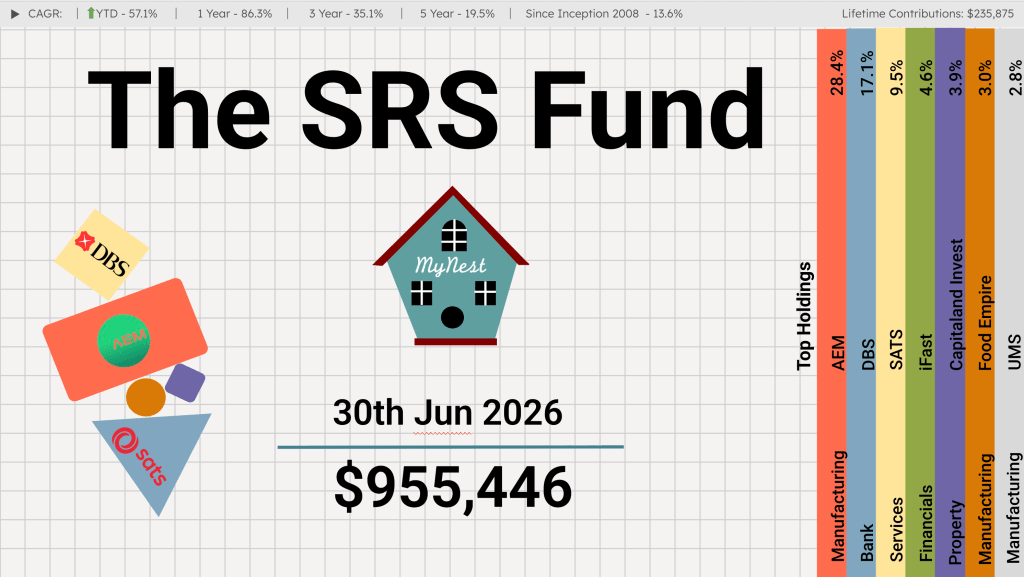

The SRS Fund Jun 2026

The month of Jun provided an important milestone in the Iran conflict. The agreement between the United States and Iran marked a significant step towards reducing geopolitical tension and reopening a clearer path for global energy flows

-

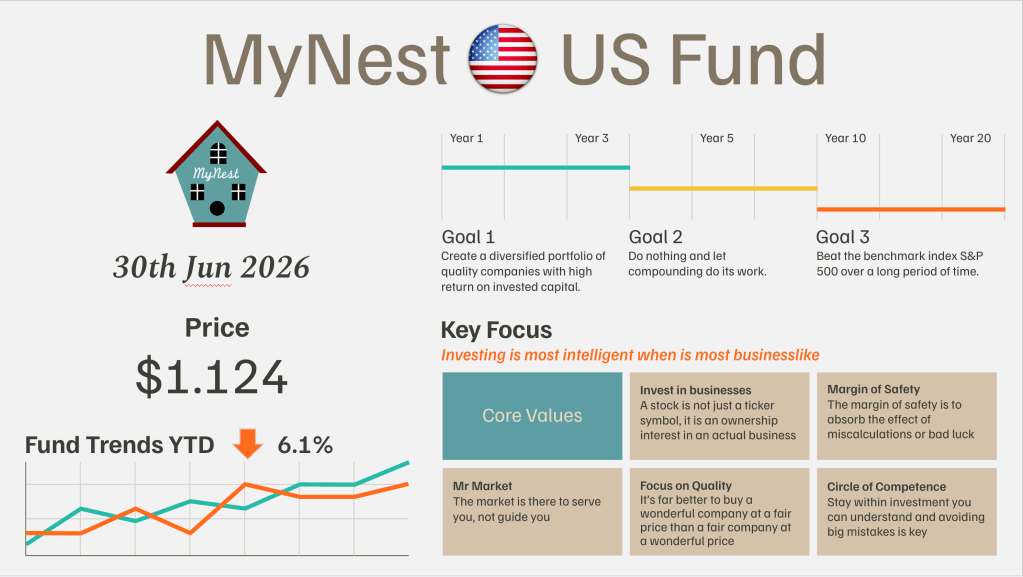

MyNest US Fund Jun 26

June was another remarkable month in the evolution of the global capitalism and the artificial intelligence investment cycle.

-

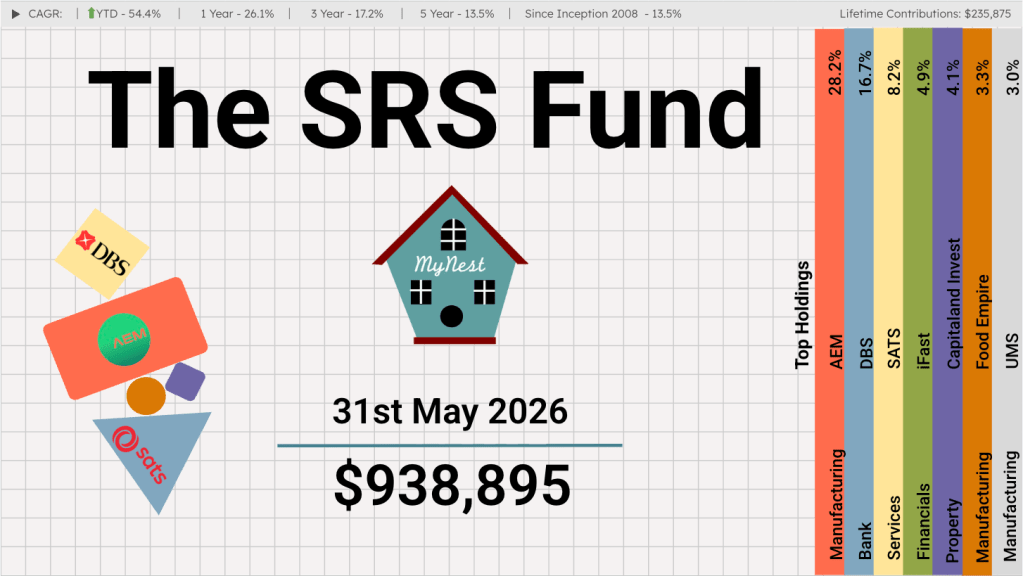

The SRS Fund May 2026

Korea, powered by the worldwide shortage and surge in memory demand, was hit directly by the AI wave, with its stock market more than doubling in a matter of 5 months. Taiwan, already the world’s most important advanced chip manufacturing hub has risen to become one of the largest stock market globally.

-

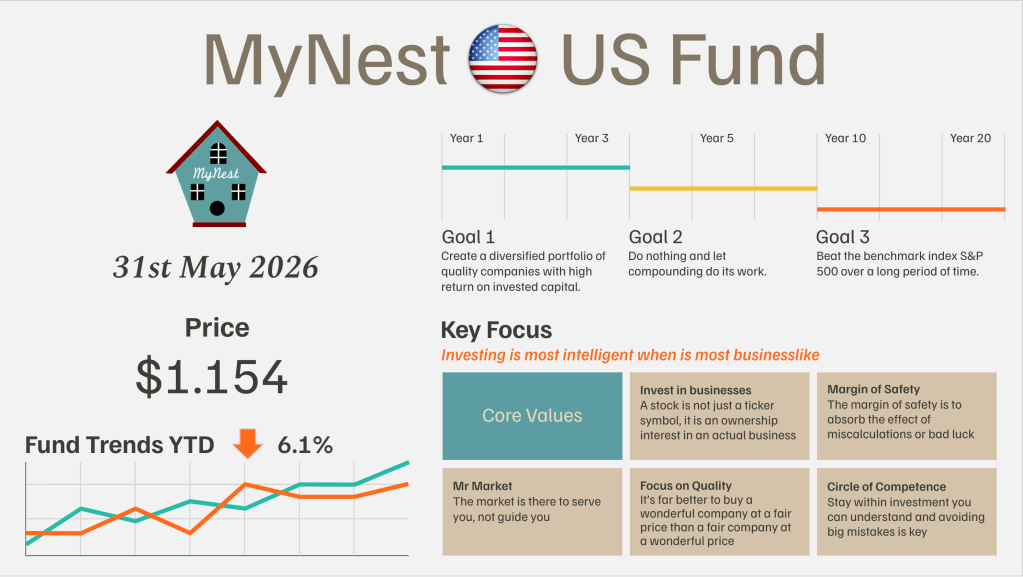

MyNest US Fund May 26

May has been an incredibly illuminating month for the MyNest US Fund. Looking across the broader landscape, the S&P 500 Index has continued its steady leg up, gaining +5.15% in the month of May alone to push its Year-to-Date (YTD) gain to +10.73%.

-

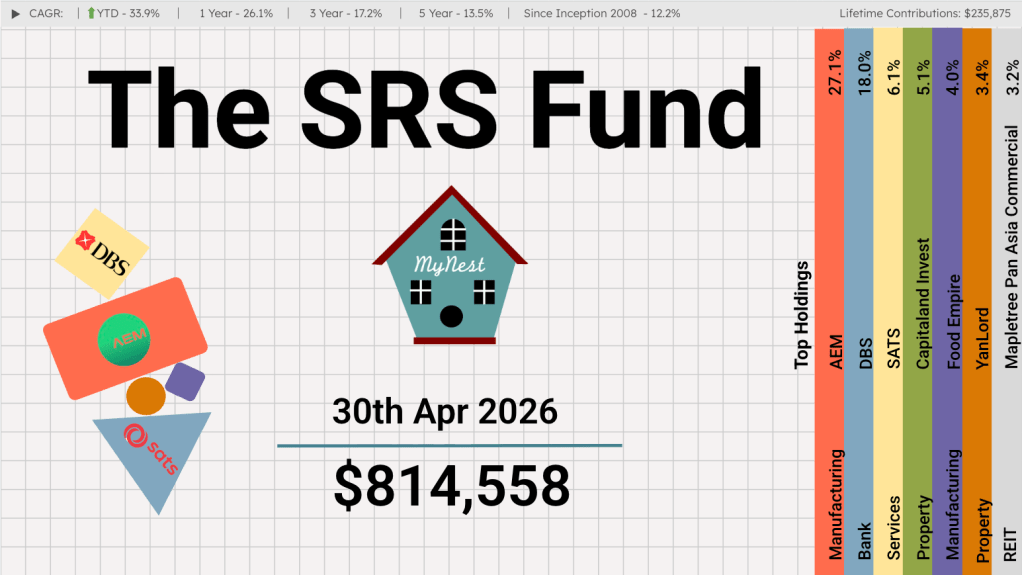

The SRS Fund Apr 2026

In my investment journey, there have been three occasions where I witnessed a company deliver a 10x return.

-

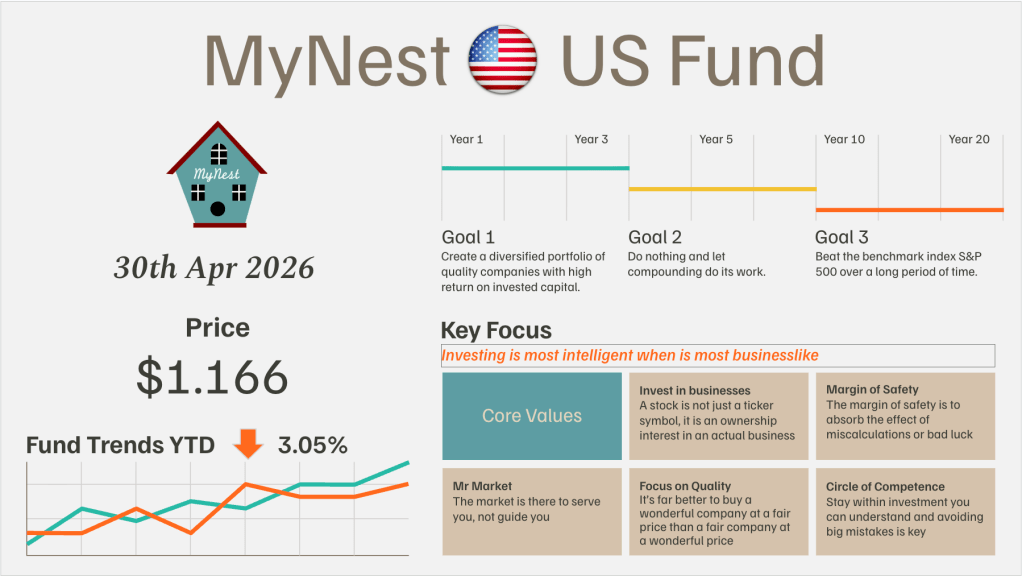

MyNest US Fund Apr 26

The market rebounded strongly in April as investors appeared to look past geopolitical uncertainty and renewed their focus on earnings, artificial intelligence, and the long-term growth prospects of quality businesses.