Dear Investors,

March shattered any lingering market complacency, pivoting sharply from the localized damage of the “SaaS-pocalypse” to a systemic shock driven by the war in Iran. The blockage of the Strait of Hormuz triggered immediate, cascading supply disruptions across oil, natural gas, helium, and fertilizers. With crude prices violently spiking from the mid-$60s to near $120 in a matter of days, the market’s overly optimistic consensus for imminent interest rate cuts has been decisively crushed. Predictably, this abrupt repricing of capital costs has rippled across all sectors, punishing interest rate-sensitive and property-related equities the hardest.

Portfolio Changes

This macro regime shift dictated our portfolio maneuvers. We liquidated our Airbnb position to secure a modest gain. In an environment where $120 oil inevitably pressures airline margins and squeezes consumer discretionary spending, holding a travel-dependent asset through the uncertainty of a protracted Middle Eastern conflict presents an asymmetrical risk we are unwilling to take.

Conversely, we aggressively added to our positions in Brookfield (BN) and Brookfield Asset Management (BAM). While it may seem counterintuitive to buy into the very sectors—property and private lending—that are currently under siege, this is exactly where the alpha lies. The current sentiment shock in private credit is shaking out weaker hands. Alternative managers like Brookfield, armed with massive dry powder and structural resilience, are uniquely positioned to capitalize on the distress of forced sellers. We are buying the dislocation, not the panic.

Fair Isaac Corporation

We initiated a new position in Fair Isaac Corporation (FICO). Critics might question adding a highly valued software and data firm immediately following a sector-wide tech sell-off. However, FICO is not speculative tech; it is an entrenched monopoly.

In an environment where the cost of capital is structurally higher and macroeconomic uncertainty is peaking, we are prioritizing assets with absolute pricing power and exceptionally high-quality, recurring earnings.

FICO’s indispensable role as a toll-bridge in the credit ecosystem provides a predictable, high-margin cash flow stream that heavily insulates our capital from broader market volatility.

Our Investment Philosophy: Owing Great Businesses

We as the owners of phenomenal businesses, our steadfast focus on business fundamentals over macro timing will periodically lead to short-term underperformance when violent shocks indiscriminately punish equities.

However, we do not merely tolerate short-term market panic; we actively rely on it. It is precisely these irrational, fear-driven drawdowns that allow us to acquire shares in world-class businesses at fair, or even discounted, prices. The exceptional companies we own possess fortress balance sheets, definitive pricing power, and superior return on invested capital. While the market obsesses over the immediate trajectory of oil and interest rates, our businesses are quietly expanding their moats.

Near-term volatility is not as a threat to mitigate, but as a net positive for the portfolio and the primary engine for long-term wealth creation. Macro-driven fear dictates the short-term stock price, but securing superior business economics at a fair price dictates our long-term results.

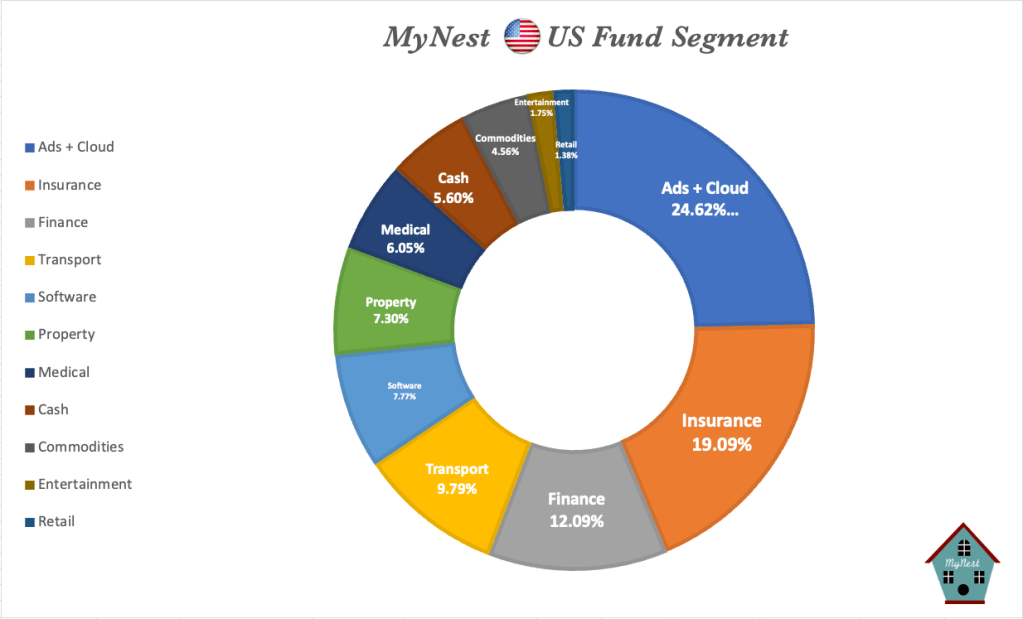

MyNest US Fund Portfolio Compositions

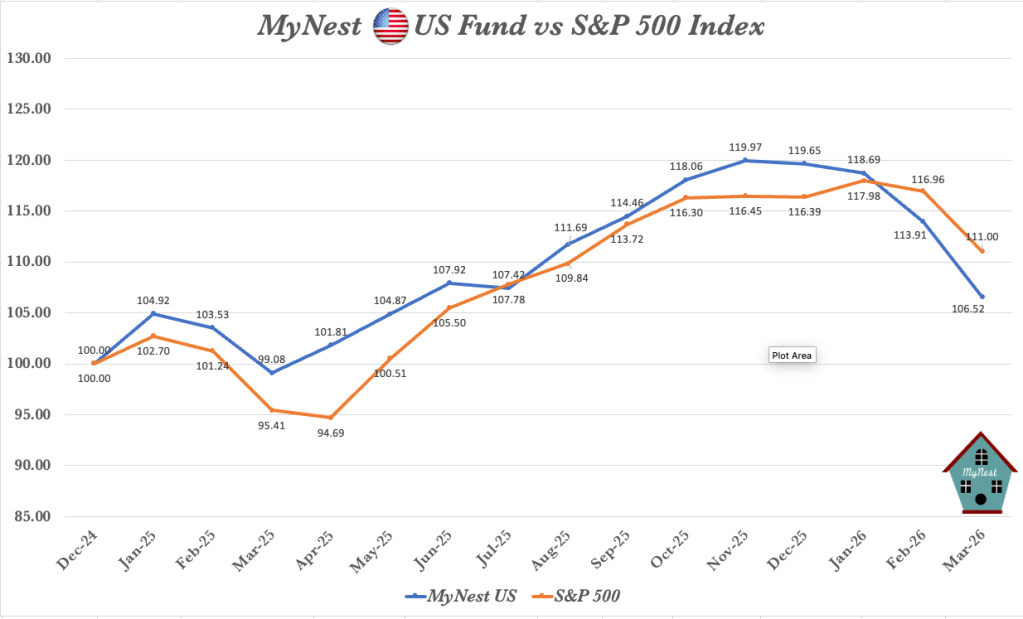

MyNest US Fund Performance

Performance & Alignment

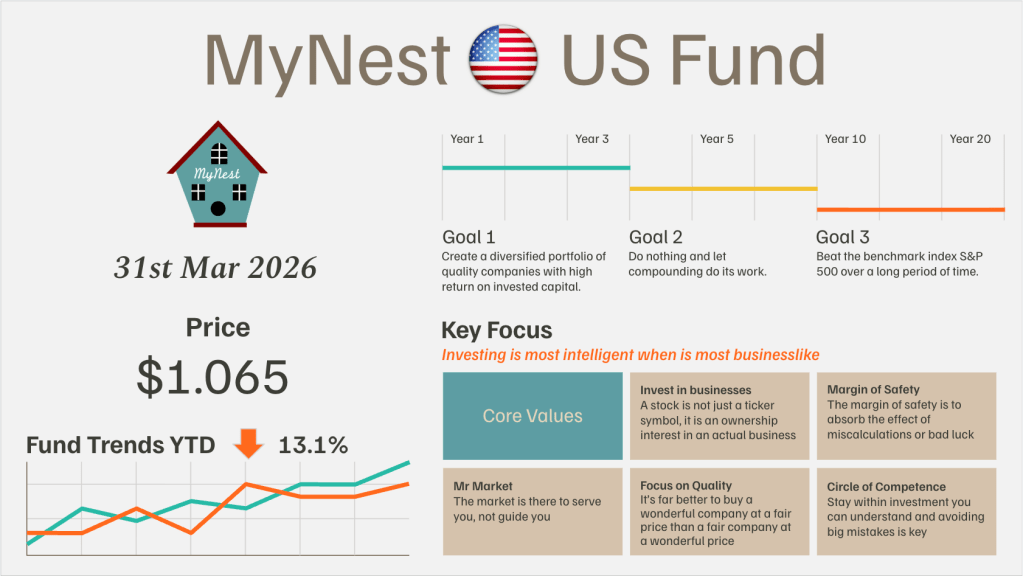

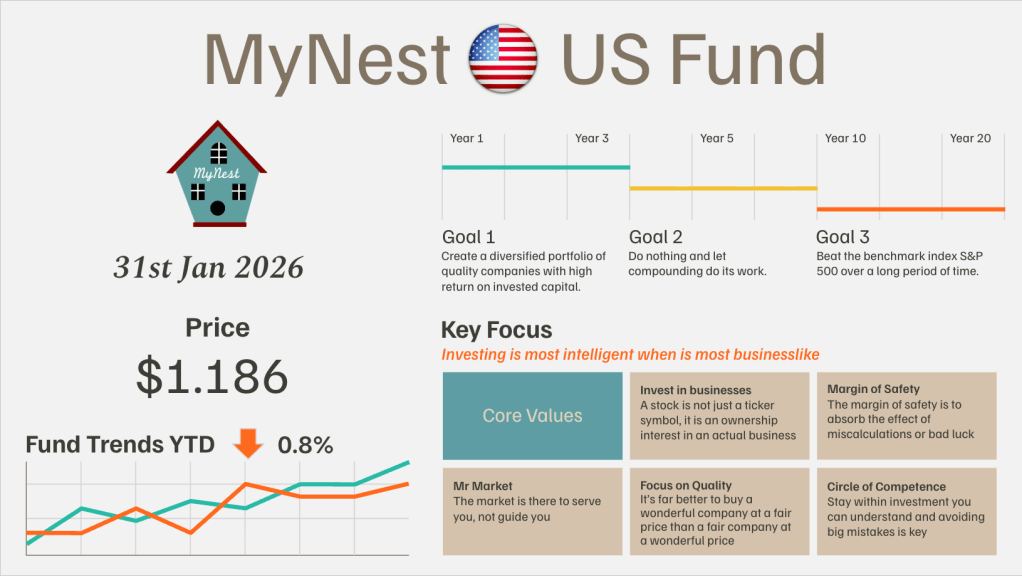

Turning to performance, the accompanying visual data paints a clear, unvarnished picture of the violent market rotation we have just navigated. We closed the first quarter on March 31, 2026, with a fund price of $1.065, reflecting a sharp 13.1% Year-to-Date drawdown. The trajectory on the chart is stark: after consistently generating alpha through 2025 and peaking at $1.19, the systemic shocks of Q1 triggered a disproportionate sell-off in our holdings, leaving us trailing the S&P 500 by 5.3%. We do not hide from this recent underperformance; however we do expect to underperform in the short term from time to time.

Instead of obsessing over a single volatile quarter, investors should look to the stated goals and core values of the MyNest US Fund. We are currently executing the transition from our Year 1 objective—creating a diversified portfolio of companies with exceptionally high Return on Invested Capital (ROIC)—to our Year 3 objective: doing nothing and letting compounding do its work. Our mandate is to beat the benchmark index over a 10-year horizon, not to optimize for quarterly aesthetic appeal.

Segment Chart

-

MyNest US Fund Mar 26

March shattered any lingering market complacency, pivoting sharply from the localized damage of the “SaaS-pocalypse” to a systemic shock driven by the war in Iran.

-

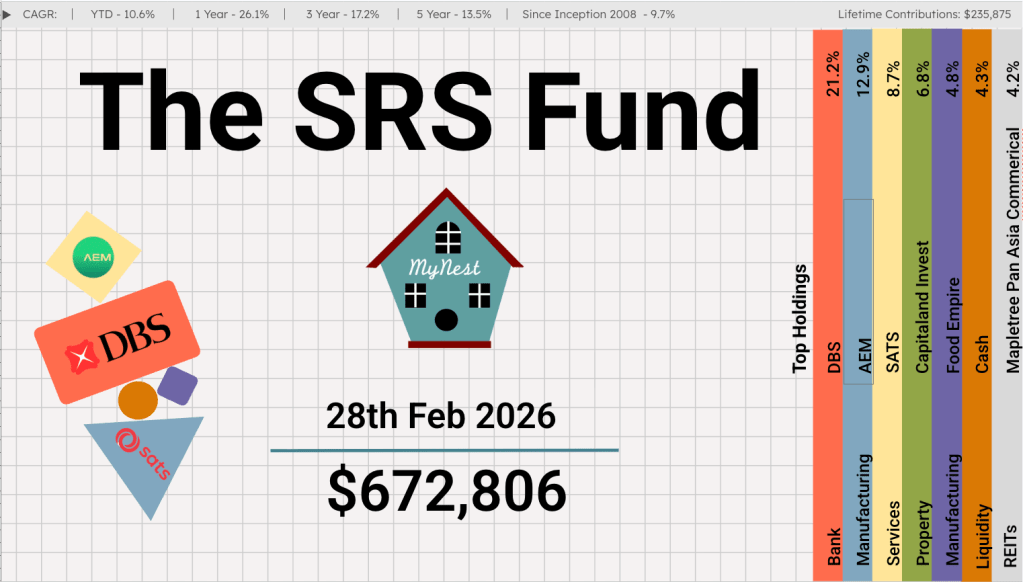

The SRS Fund Feb 2026

The Singapore Budget 2026 has set a robust backdrop for local investors. For the third consecutive year, the government is operating from a position of immense “dry powder,” with an overall fiscal surplus of $8.5 billion projected for FY2026.

-

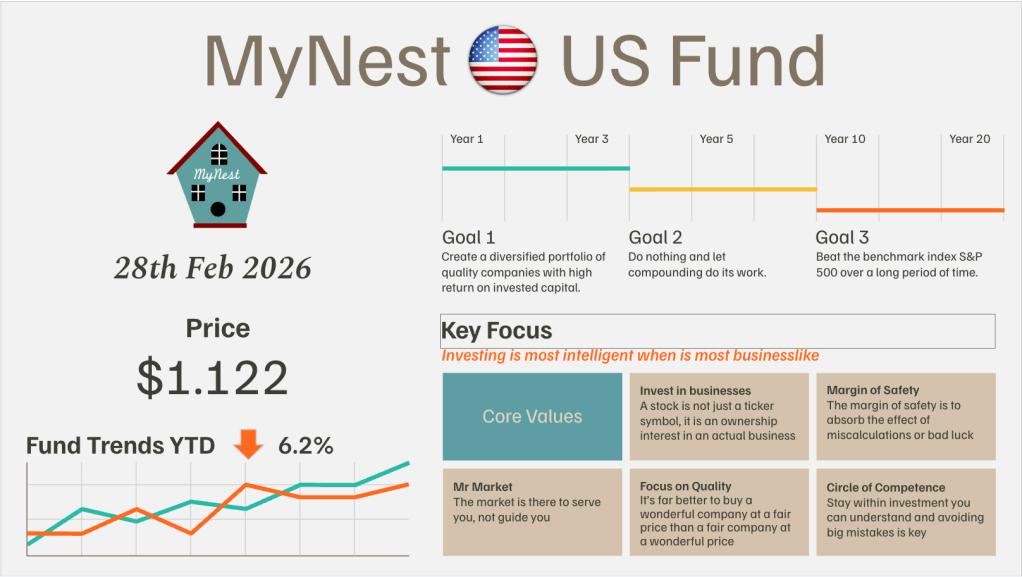

MyNest US Fund Feb 26

February 2026 proved to be one of the most challenging months for our fund since its inception. A wave of “AI anxiety” swept through the Software-as-a-Service (SaaS) sector

-

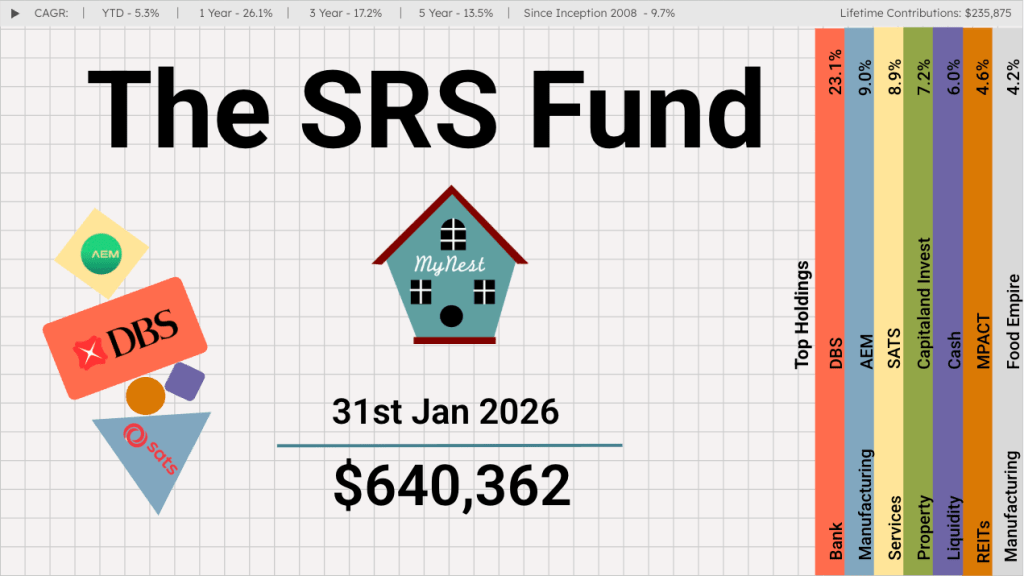

The SRS Fund Jan 2026

After a blockbuster 2025 that saw GDP growth hit a surprise 4.8%, the first month of 2026 has proven that the momentum is far from a fluke. Between record-breaking stock market performance and massive industrial investments, the “Little Red Dot” is making a very big noise.

-

MyNest US Fund Jan 26

I have a confession to make. After reading Chip War at the end of 2022, I fully grasped the strategic importance of TSMC and ASML in the global semiconductor supply chain.

-

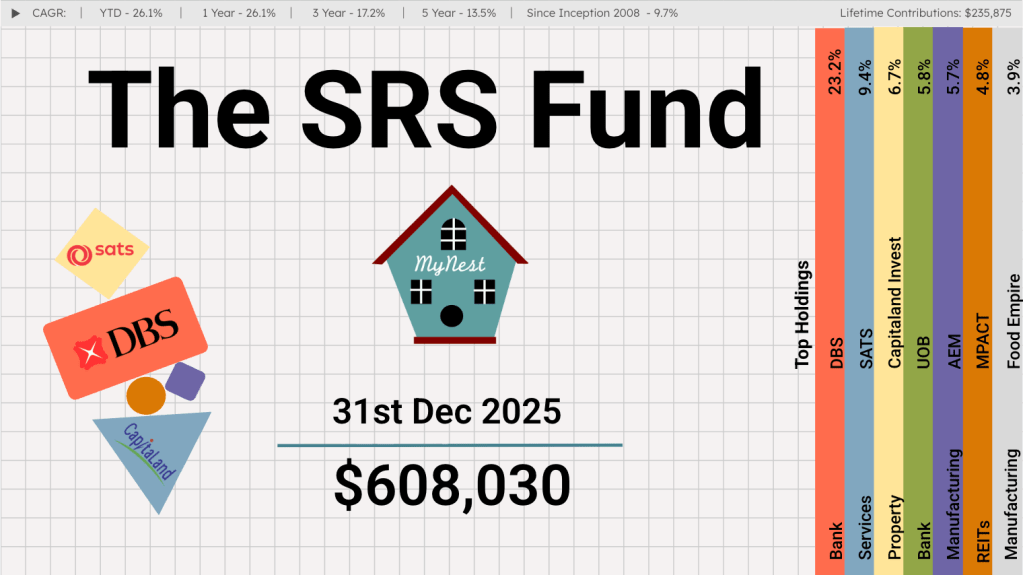

The SRS Fund Dec 2025

If someone had told me at the start of the year that the Singapore stock market would deliver returns in excess of 20%, I would have shrugged it off as wishful thinking.