Dear Investors,

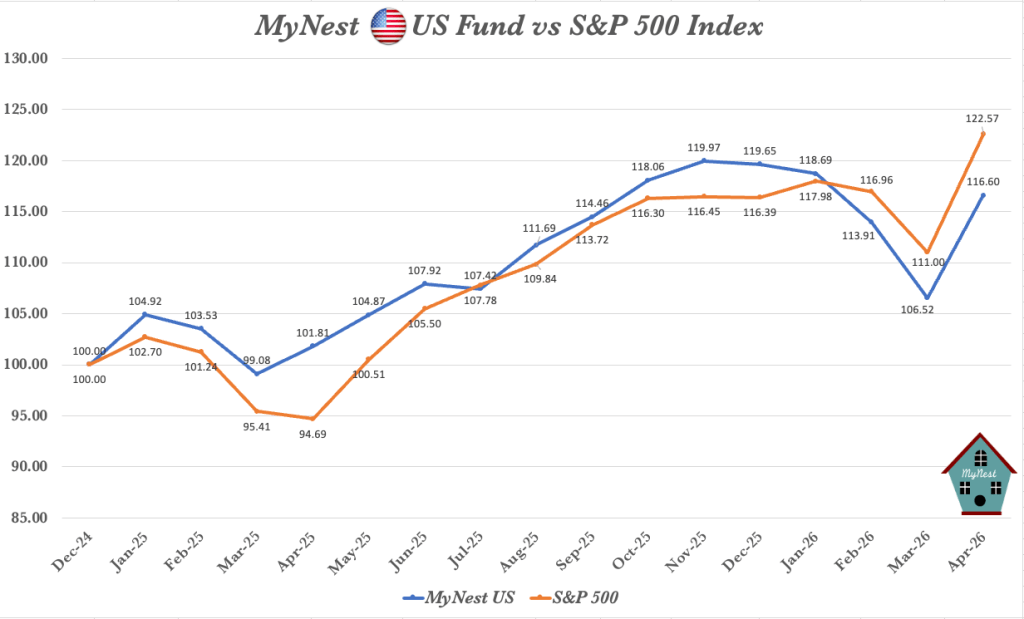

The market rebounded strongly in April as investors appeared to look past geopolitical uncertainty and renewed their focus on earnings, artificial intelligence, and the long-term growth prospects of quality businesses. The MyNest US Fundrose by approximately 10% from March, almost matching the strong rebound in the S&P 500.

Despite this recovery, the Fund remains down by around 3% year to date, while the S&P 500 is up by close to 3%. Based on our review, the main source of underperformance has been our relatively limited exposure to semiconductor manufacturing and AI infrastructure-related companies. Businesses directly connected to AI chip production have surged, driven by what still appears to be insatiable demand from hyperscalers.

The scale of AI-related capital expenditure continues to be extraordinary. Google, Amazon, Meta and Microsoft are collectively committing hundreds of billions of dollars to data centres, chips, cloud infrastructure and AI capabilities. Google was one of the highlights of this earnings season, with Google Cloud delivering another strong performance. The market has increasingly recognised Alphabet’s ability to compete not only in software and cloud, but also in AI infrastructure through its full-stack approach, including its own TPU offerings.

We continue to believe Alphabet can become one of the most important AI beneficiaries over the coming years. While Nvidia remains the clear leader in GPUs, Google’s combination of search, cloud, data, distribution, AI models and custom chips gives it a unique position in the AI value chain. In our view, Alphabet has the potential to play a leading role in both our portfolio and the broader index for many years to come.

Portfolio Changes

During the month, we added Mastercard, Constellation Software, and more shares of Markel & Uber to the portfolio. These are businesses we admire for their strong competitive positions, durable business models and long-term compounding potential. Mastercard and Constellation Software, in particular, have been trading at valuations that are more attractive relative to their own historical ranges. The continued concern around AI disruption, including fears surrounding tools such as Anthropic’s Claude and other AI coding platforms, has weighed on parts of the software market. We believe this has created selective opportunities to accumulate high-quality companies at more reasonable prices.

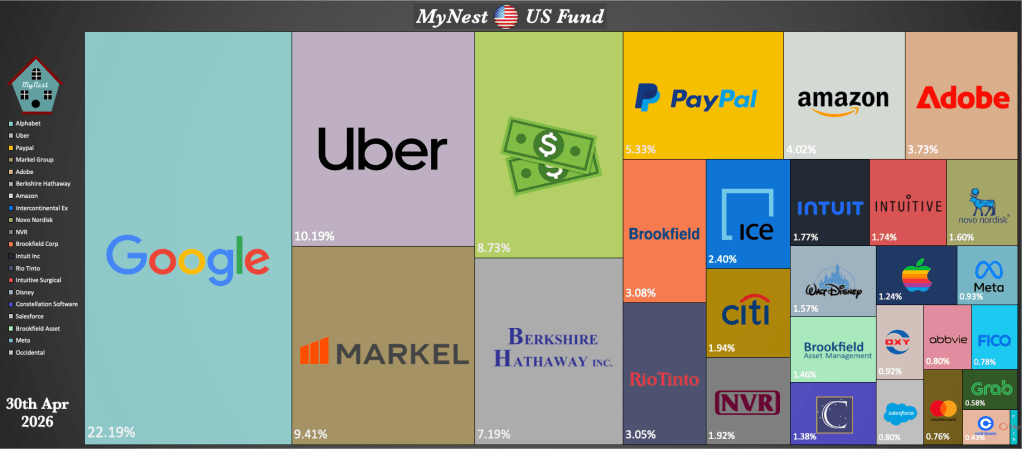

MyNest US Fund Portfolio Compositions

MyNest US Fund Performance

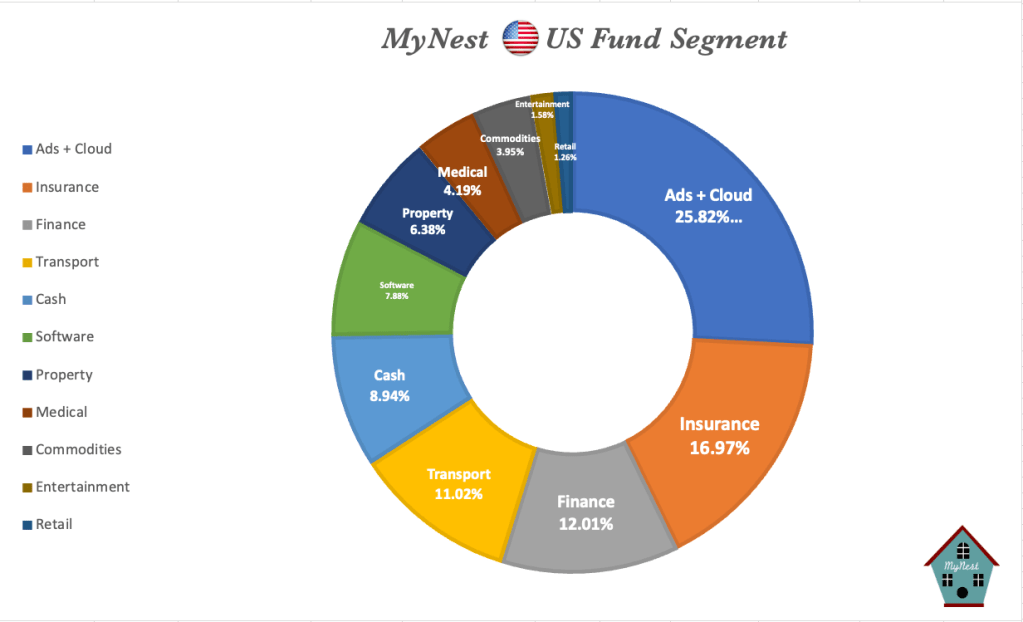

Segment Chart

As shown in our portfolio segment chart, the Fund remains meaningfully exposed to Ads & Cloud, Insurance, Finance, Transport, Cash, and Software. Our largest positions continue to be businesses with strong balance sheets, resilient earnings power and long runways for reinvestment. Alphabet remains our largest holding, followed by Uber, Markel, Berkshire Hathaway and our cash position.

Over time, we expect this collection of quality businesses to outperform our benchmark, the S&P 500, as they continue to create value for shareholders. Short-term underperformance is never pleasant, but it is also part of any long-term investment journey. We remain committed to our strategy of owning durable, high-quality companies at sensible prices.

Lastly we would also like to thank you for your continued trust and for the additional cash contributions made to the MyNest US Fund. Your confidence allows us to stay disciplined, patient and focused on long-term compounding.

-

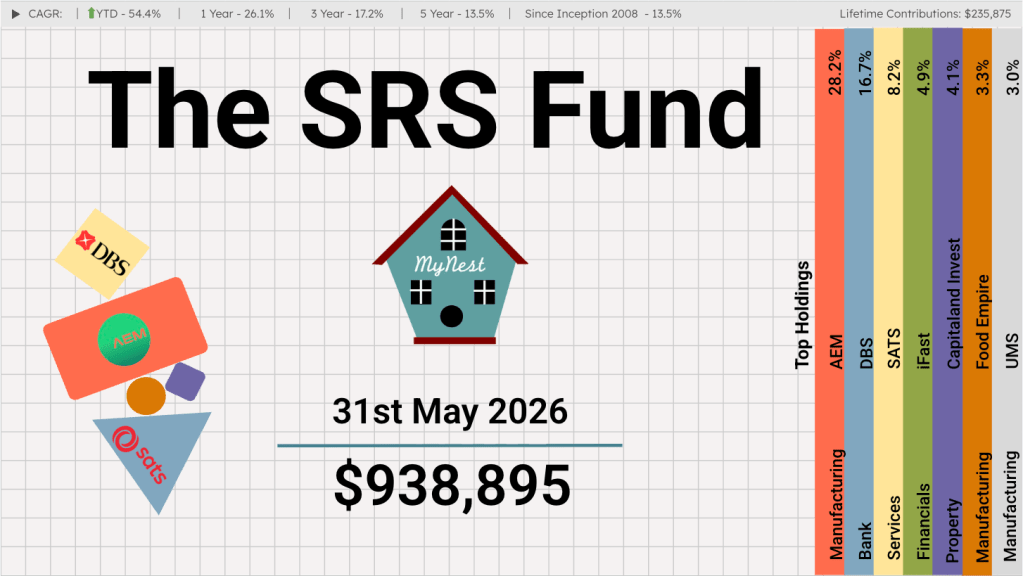

The SRS Fund May 2026

Korea, powered by the worldwide shortage and surge in memory demand, was hit directly by the AI wave, with its stock market more than doubling in a matter of 5 months. Taiwan, already the world’s most important advanced chip manufacturing hub has risen to become one of the largest stock market globally.

-

MyNest US Fund May 26

May has been an incredibly illuminating month for the MyNest US Fund. Looking across the broader landscape, the S&P 500 Index has continued its steady leg up, gaining +5.15% in the month of May alone to push its Year-to-Date (YTD) gain to +10.73%.

-

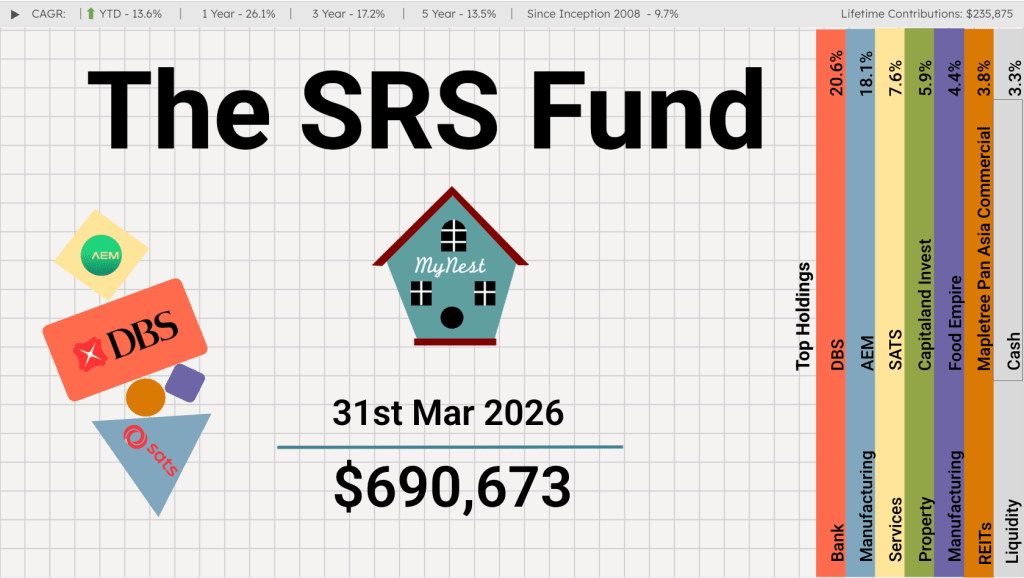

The SRS Fund Apr 2026

In my investment journey, there have been three occasions where I witnessed a company deliver a 10x return.

-

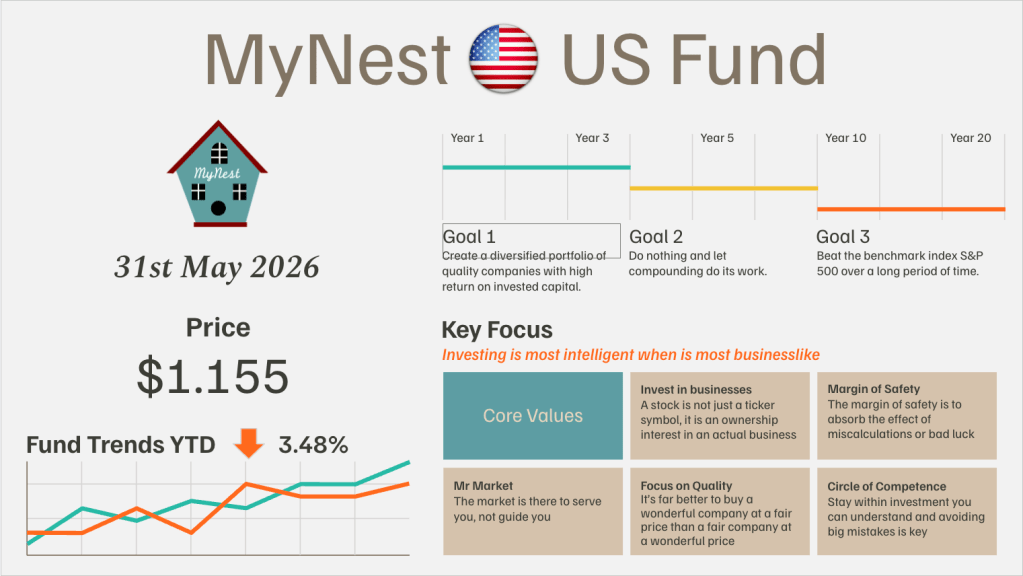

MyNest US Fund Apr 26

The market rebounded strongly in April as investors appeared to look past geopolitical uncertainty and renewed their focus on earnings, artificial intelligence, and the long-term growth prospects of quality businesses.

-

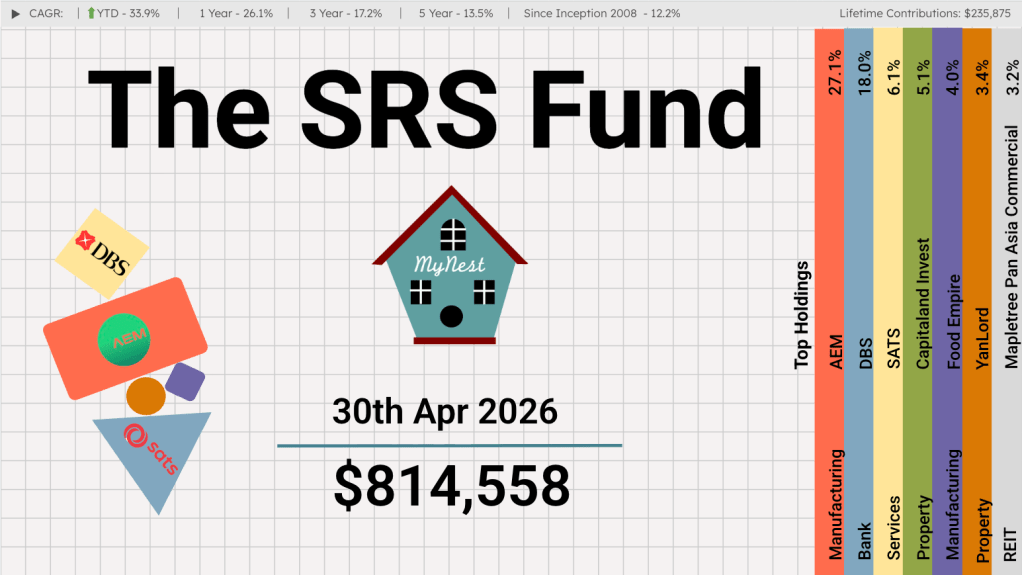

The SRS Fund Mar 2026

It is an enduring market reality that a concentrated minority of holdings drives the vast majority of returns. For years, DBS (currently the largest individual holding at 20.6%) has served as the compounding engine of the SRS Fund.

-

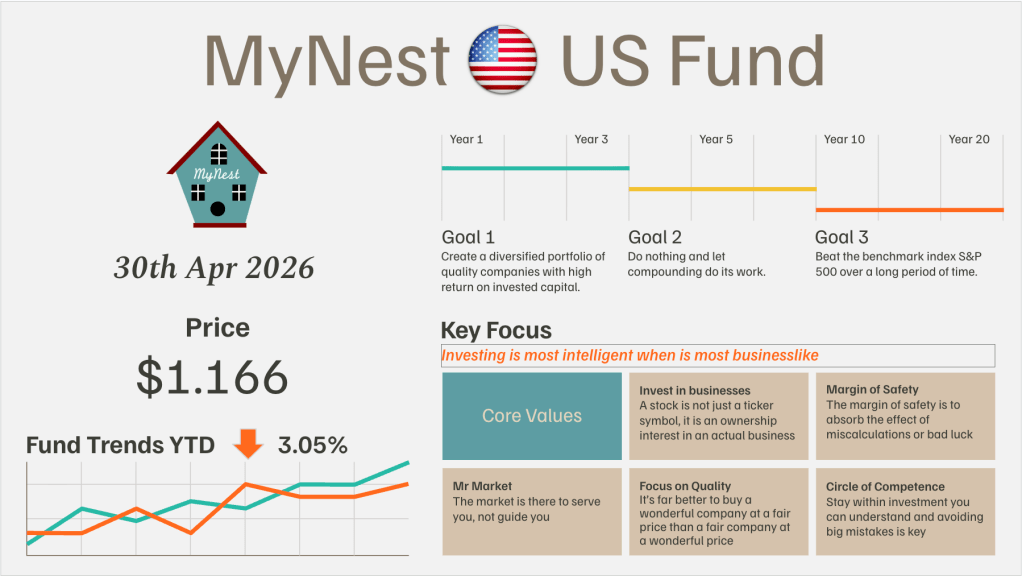

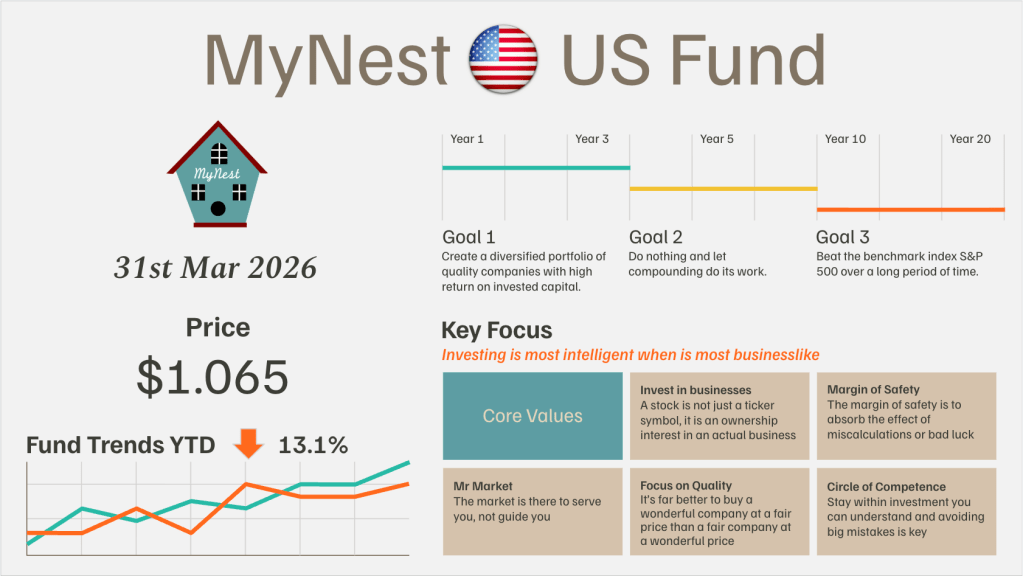

MyNest US Fund Mar 26

March shattered any lingering market complacency, pivoting sharply from the localized damage of the “SaaS-pocalypse” to a systemic shock driven by the war in Iran.