The stock market rally which begin in Jan of 2023 seem more driven by emotional factors than macro trends. While all signs points to lower inflation (main trigger for last year selloff), I believe several global market trends now makes it unlikely for it to revert to 2% level.

De-Globalisation

As Covid whack havoc on global supply chain companies reacted by diversifying suppliers to several countries which boosted the resilience of supply but at the expense of higher cost.

US Conflict with China

The battle of the 2 giants continue on many fronts from leading edge technology to electric vehicles. US had ban high end chip sales to China which will likely drive up cost for technological products and services.

War

The war which started almost a year ago has no end in sight. Recent development with the West providing tanks will further escalate it. Disruption to oil and other supplies will continue to put pressure on prices to rise.

High Interest Rates

The rally suggested the Federal Reserves will do a U-turn soon and start lowering interest rates. This I feel amounts to wishful thinking as inflation once out is not easy to put back into the can. As such I can see the Fed gradually increasing rate and holding rates high for a substantial amount time (At least 12 months even after paused). While the Fed had been wrong on most occasions in recent years, holding rate above the inflation number seems to be the most rational act any central bank can do.

If interest rate remain high for an extended period of time, consumer and business with excess debt will begin to feel the strain on cost. Revenue growth will slow and a cleansing recession will occur. During this time the stock market will likely reflect the worsening fundamentals and indices will end the year lower in 2023

The SRS Fund Review

While the new year usher in a run up in REITs prices it is my belief that the fund fundamentals does not change materially on a month to month basis. As such I will only be updating the SRS Funds performance on a quarterly basis instead going forward.

-

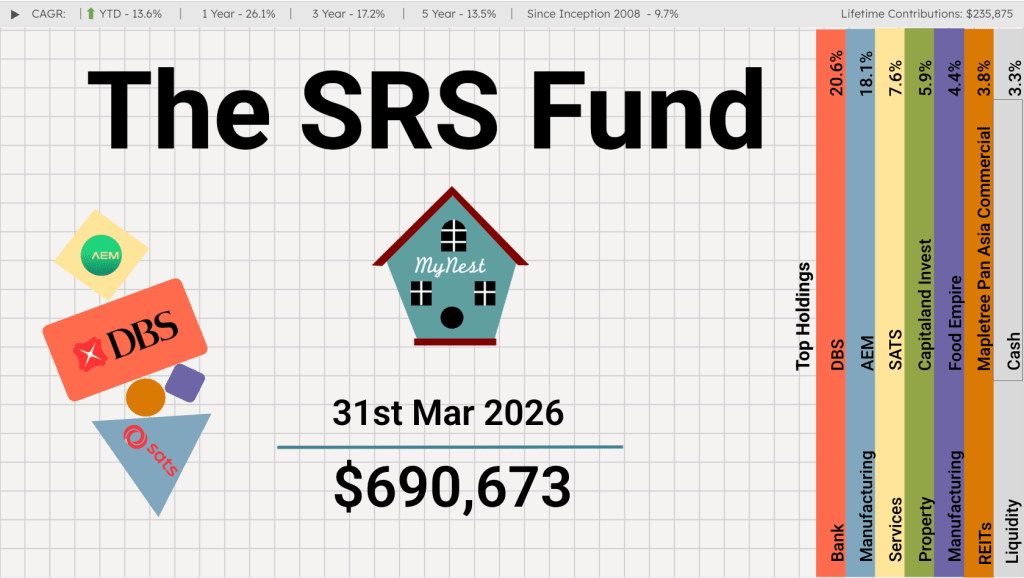

The SRS Fund Mar 2026

It is an enduring market reality that a concentrated minority of holdings drives the vast majority of returns. For years, DBS (currently the largest individual holding at 20.6%) has served as the compounding engine of the SRS Fund.

-

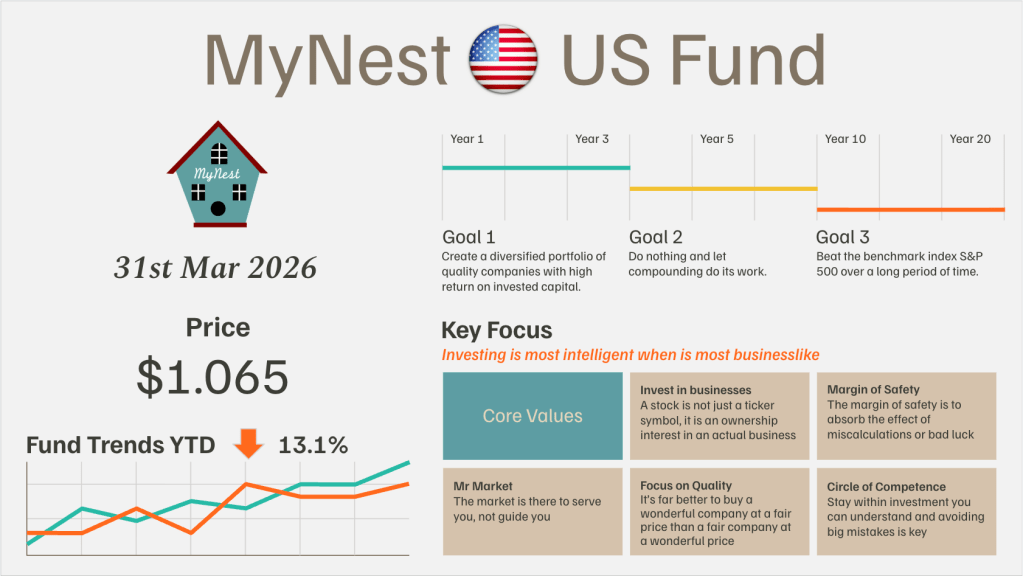

MyNest US Fund Mar 26

March shattered any lingering market complacency, pivoting sharply from the localized damage of the “SaaS-pocalypse” to a systemic shock driven by the war in Iran.

-

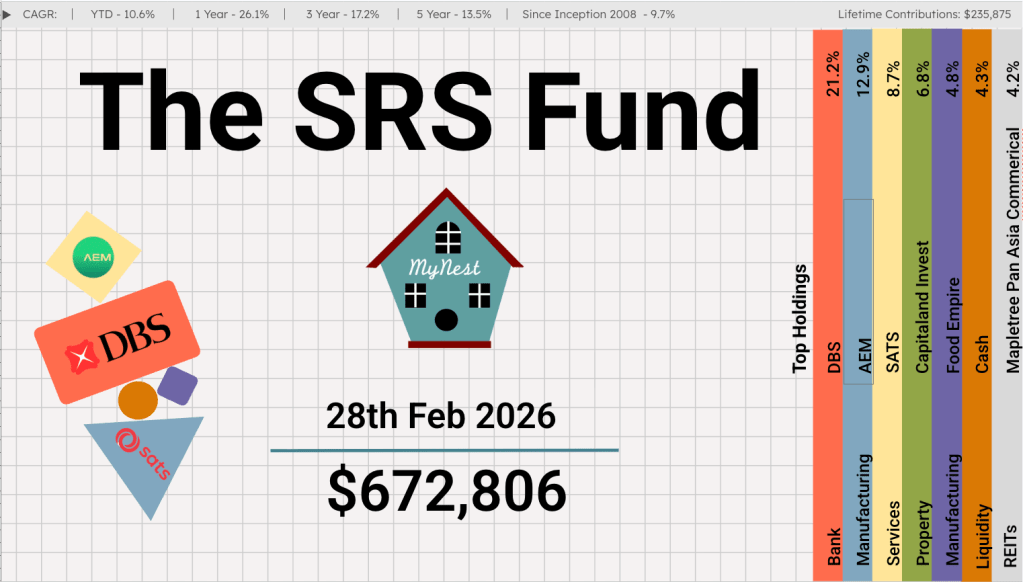

The SRS Fund Feb 2026

The Singapore Budget 2026 has set a robust backdrop for local investors. For the third consecutive year, the government is operating from a position of immense “dry powder,” with an overall fiscal surplus of $8.5 billion projected for FY2026.

-

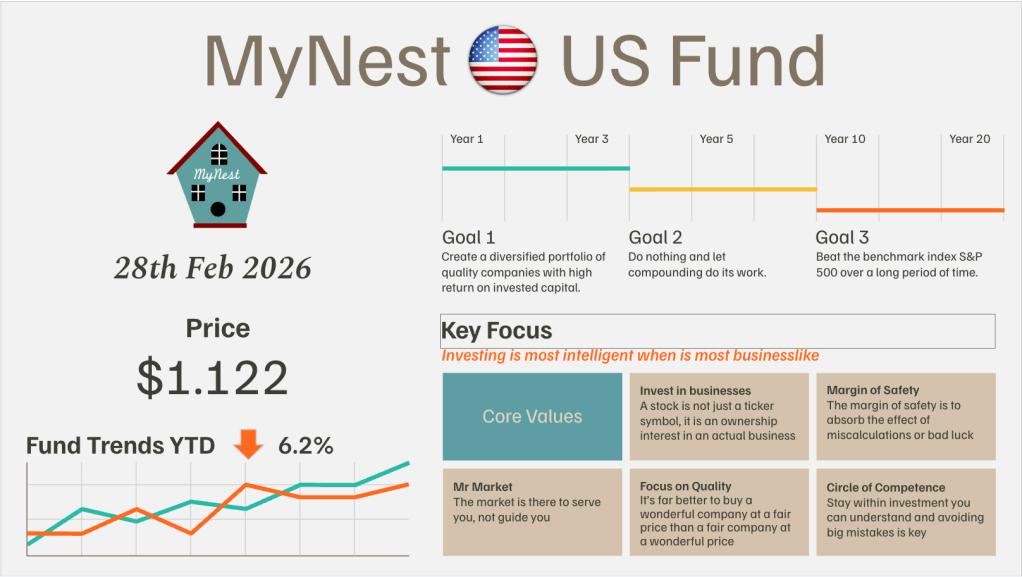

MyNest US Fund Feb 26

February 2026 proved to be one of the most challenging months for our fund since its inception. A wave of “AI anxiety” swept through the Software-as-a-Service (SaaS) sector

-

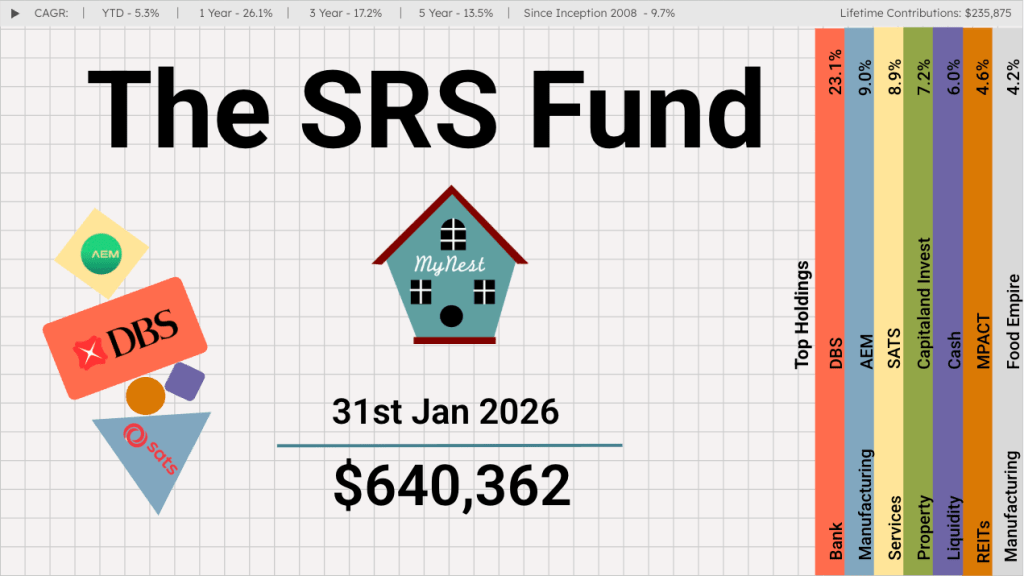

The SRS Fund Jan 2026

After a blockbuster 2025 that saw GDP growth hit a surprise 4.8%, the first month of 2026 has proven that the momentum is far from a fluke. Between record-breaking stock market performance and massive industrial investments, the “Little Red Dot” is making a very big noise.

-

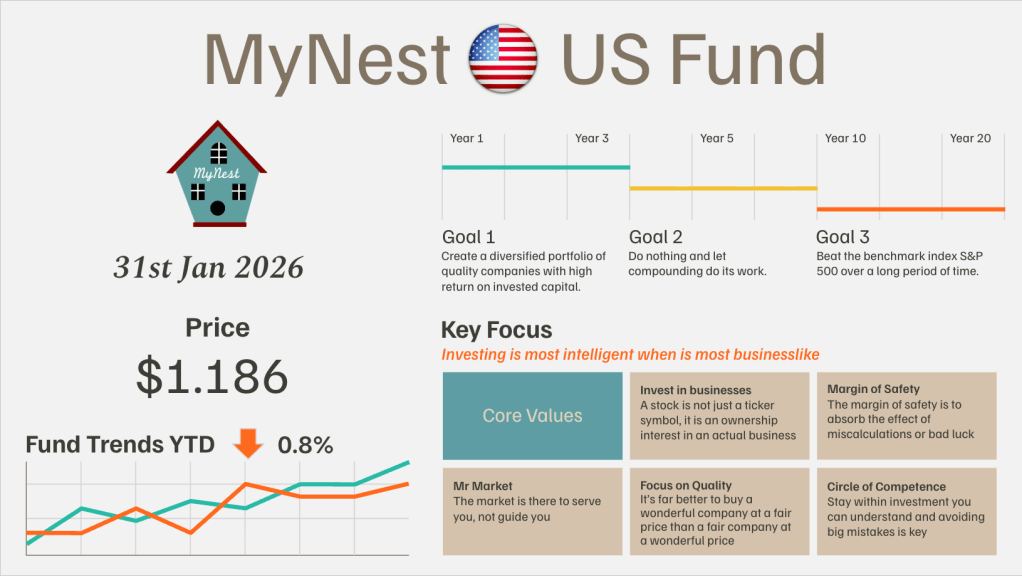

MyNest US Fund Jan 26

I have a confession to make. After reading Chip War at the end of 2022, I fully grasped the strategic importance of TSMC and ASML in the global semiconductor supply chain.