Historically inversion of the yield curve had forewarned a recession in the making. After 2 decades of low-interest rates, runaway inflation post-Covid had finally pushed the federal reserves to increase the short-term rates at an unprecedented pace, now at over 5.5%.

However long-dated bonds had risen much slower, creating the inverted yield curve as we have known. Since the start of a rate rise in mid-2022 investors have been clamoring that the rising short end of the curve is a temporary measure to curb high inflation. The narrative is always that short-term interest rates will have to come down when inflation becomes subdued or faced with a severe recession.

Historical low-interest rates should not be taken for granted mainly because one cannot simply assume inflation will return to low levels. In fact, trends have been pointing to higher inflation including, deglobalisation, higher sovereign debt levels, and geopolitical instability.

With all the reasons above I would argue that the Normalisation of the Yield Curve would adjust on the long end of the curve rising beyond the short-term interest rates. The normalization process will be painful for financial markets as asset prices readjust and investors come to terms with the “Normalized” level of interest rates.

Howard Marks recently argued for the case of high-yield bond investment over equity upon further thoughts of his “Sea Change” article. While I fully embrace the “Sea Change” article, I beg to differ on his recent conclusion. As we see higher inflation, only quality businesses that are able to pass on the higher costs to end customers will endure and thrive in the new environment.

Bonds regardless of whether high yield or not do not have such defensive characteristics. However, I agree that such high-yield strategies may still outperform many individual stocks that will likely be swept away by this inflationary tsunami.

-

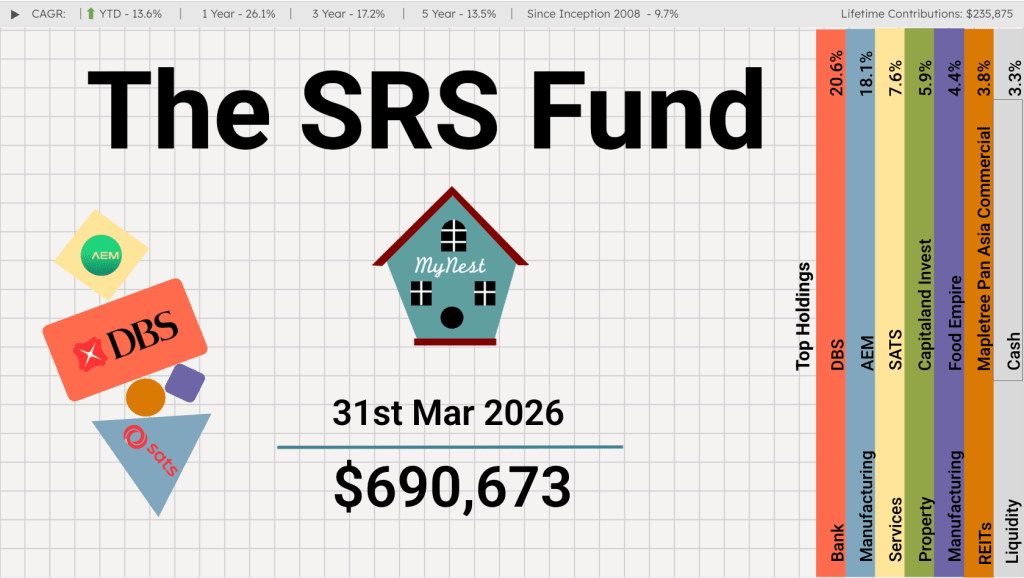

The SRS Fund Mar 2026

It is an enduring market reality that a concentrated minority of holdings drives the vast majority of returns. For years, DBS (currently the largest individual holding at 20.6%) has served as the compounding engine of the SRS Fund.

-

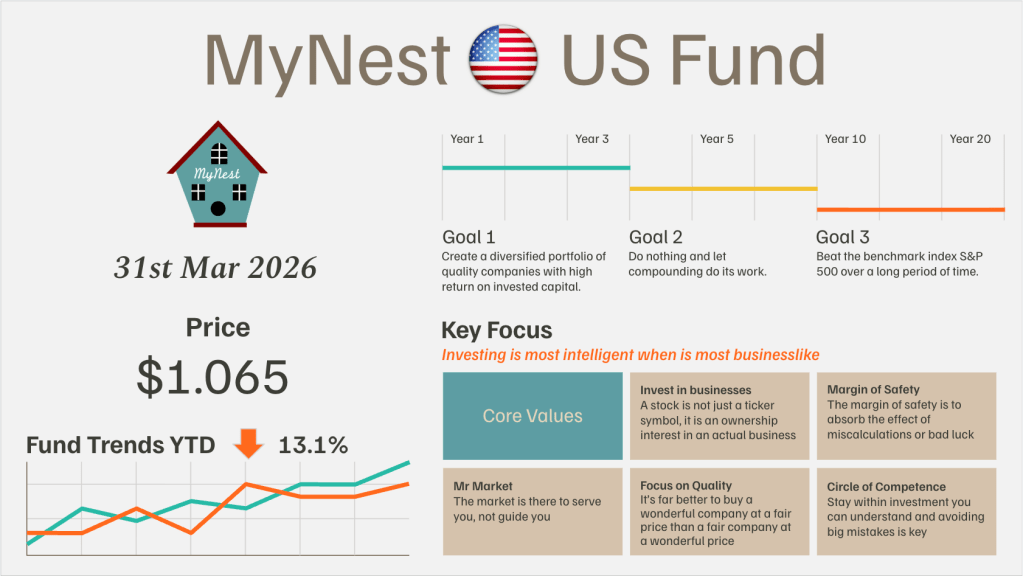

MyNest US Fund Mar 26

March shattered any lingering market complacency, pivoting sharply from the localized damage of the “SaaS-pocalypse” to a systemic shock driven by the war in Iran.

-

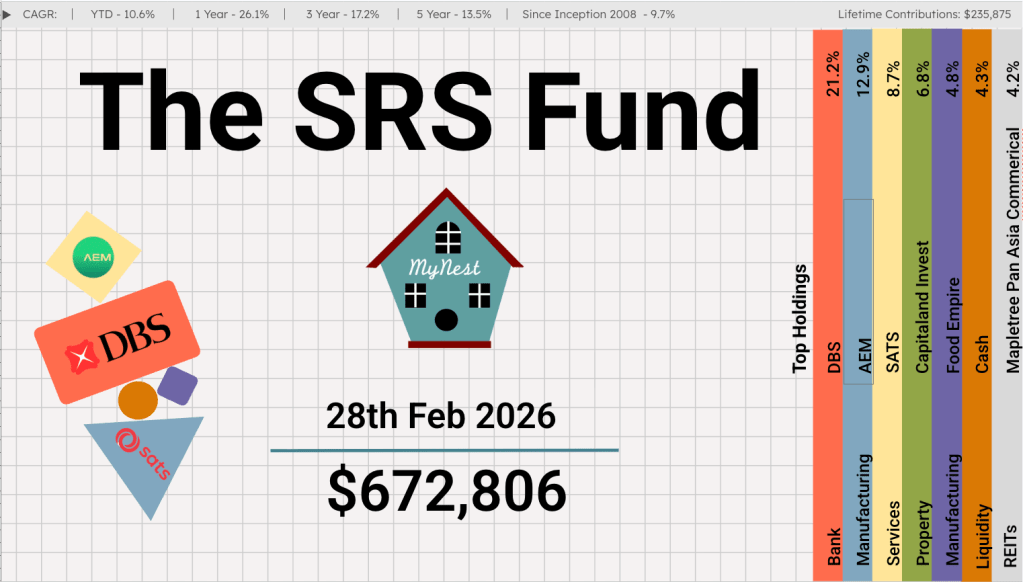

The SRS Fund Feb 2026

The Singapore Budget 2026 has set a robust backdrop for local investors. For the third consecutive year, the government is operating from a position of immense “dry powder,” with an overall fiscal surplus of $8.5 billion projected for FY2026.

-

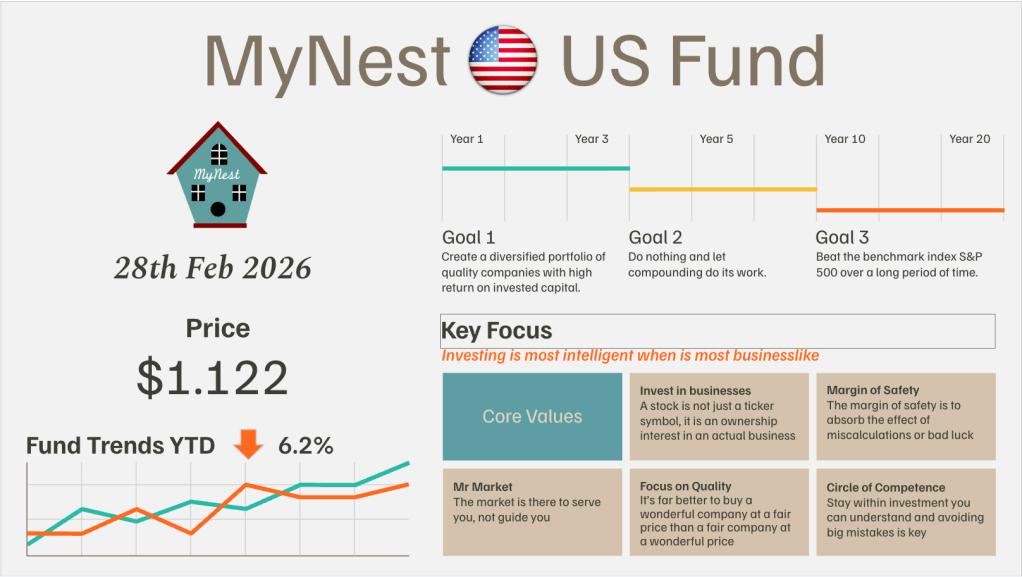

MyNest US Fund Feb 26

February 2026 proved to be one of the most challenging months for our fund since its inception. A wave of “AI anxiety” swept through the Software-as-a-Service (SaaS) sector

-

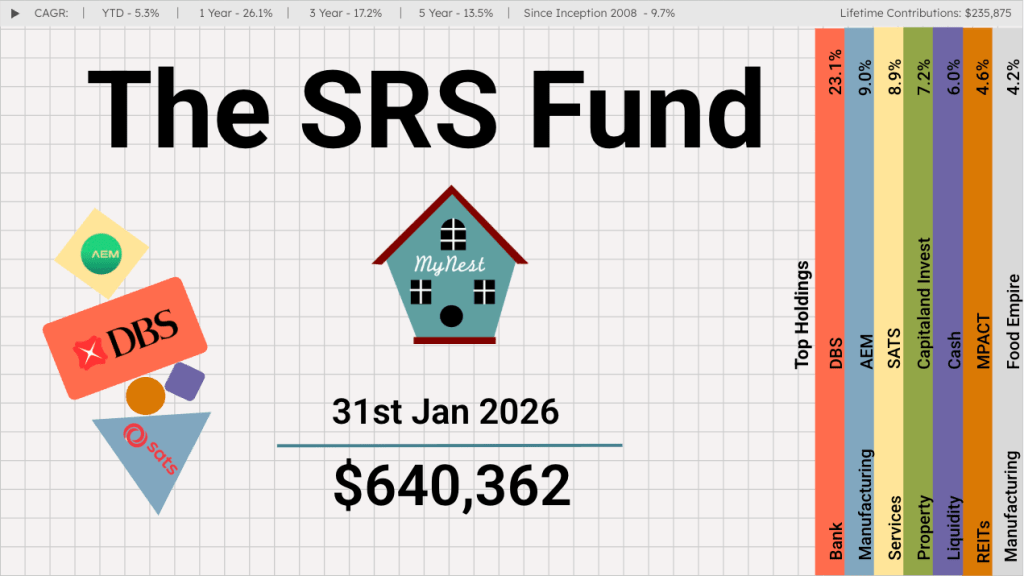

The SRS Fund Jan 2026

After a blockbuster 2025 that saw GDP growth hit a surprise 4.8%, the first month of 2026 has proven that the momentum is far from a fluke. Between record-breaking stock market performance and massive industrial investments, the “Little Red Dot” is making a very big noise.

-

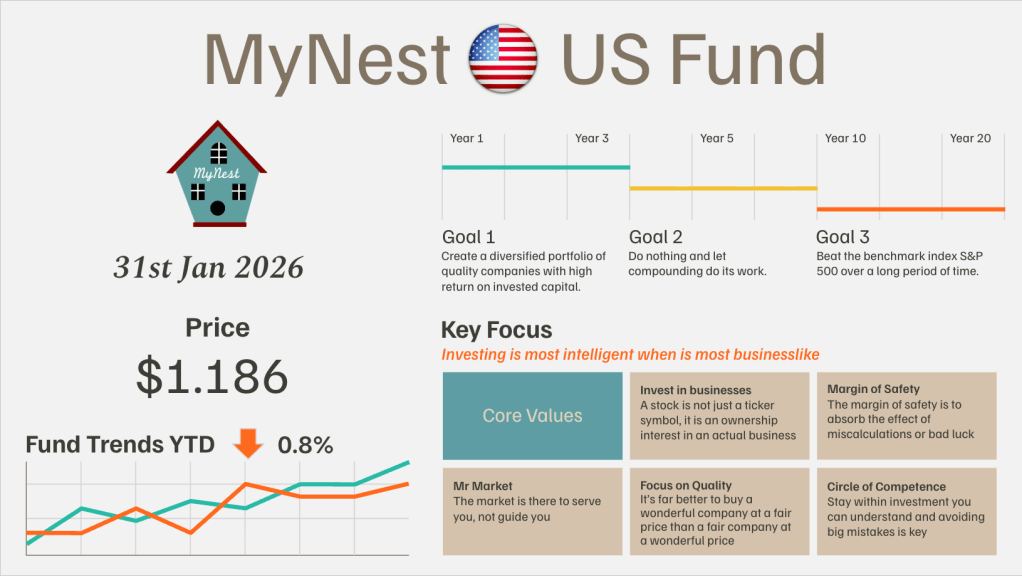

MyNest US Fund Jan 26

I have a confession to make. After reading Chip War at the end of 2022, I fully grasped the strategic importance of TSMC and ASML in the global semiconductor supply chain.