The Ten Baggers

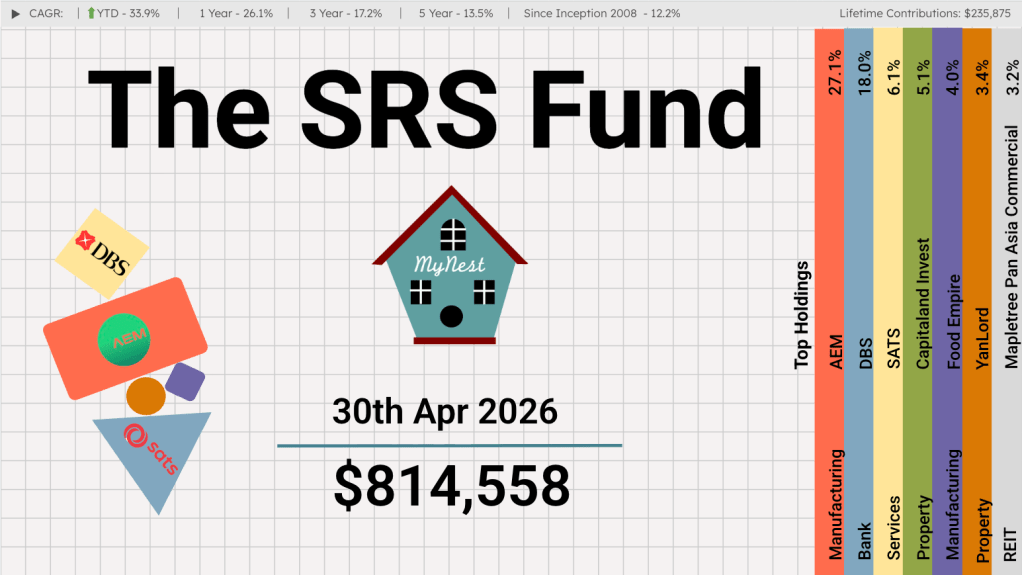

In my investment journey, there have been three occasions where I witnessed a company deliver a 10x return.

The first was SGX during my internship as a stockbroker. The next two were iFAST and PropNex — both of which the SRS Fund had the opportunity to own. Unfortunately, in both cases, I sold too early and captured only a modest profit instead of riding the full journey.

Looking back, the mistake was clear. I did not yet have a deep enough understanding of the true value of those businesses, their long-term earning power, and the size of the opportunity ahead of them. As a result, the SRS Fund missed out on the extraordinary returns created by these two winners.

I hope this time will be third time lucky.

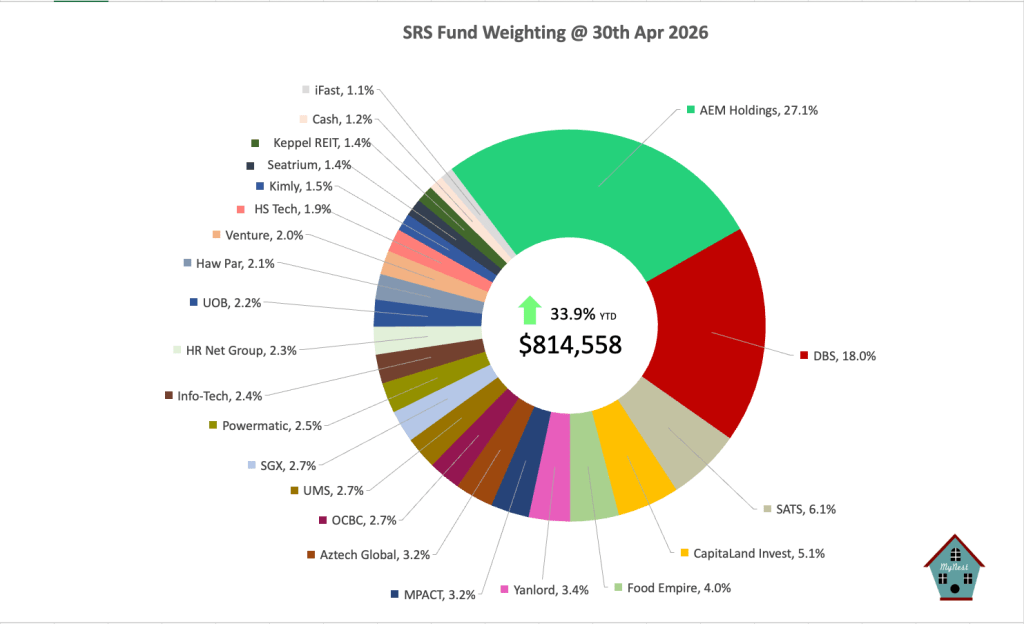

As my investment philosophy has matured, I have become more willing to hold on to businesses where the long-term opportunity may be much larger than what current earnings suggest. AEM Holdings has found itself at the epicentre of a sudden surge in demand for AI-related chips, advanced packaging, and memory testing. In April, AEM’s share price rose sharply and overtook DBS to become the largest holding in the SRS Fund.

At 27.1% of the portfolio, AEM is now a very significant position. This is not without risk, and I remain aware that expectations have moved ahead quickly. However, if AEM can successfully participate in the structural growth of AI chip and memory testing, the company may have entered a much larger addressable market than what investors had previously assumed.

The key lesson from SGX, iFAST and PropNex is not simply to “never sell”. Rather, it is to avoid selling too early when the underlying business quality, industry tailwinds and long-term earnings potential are still improving.

Portfolio Changes

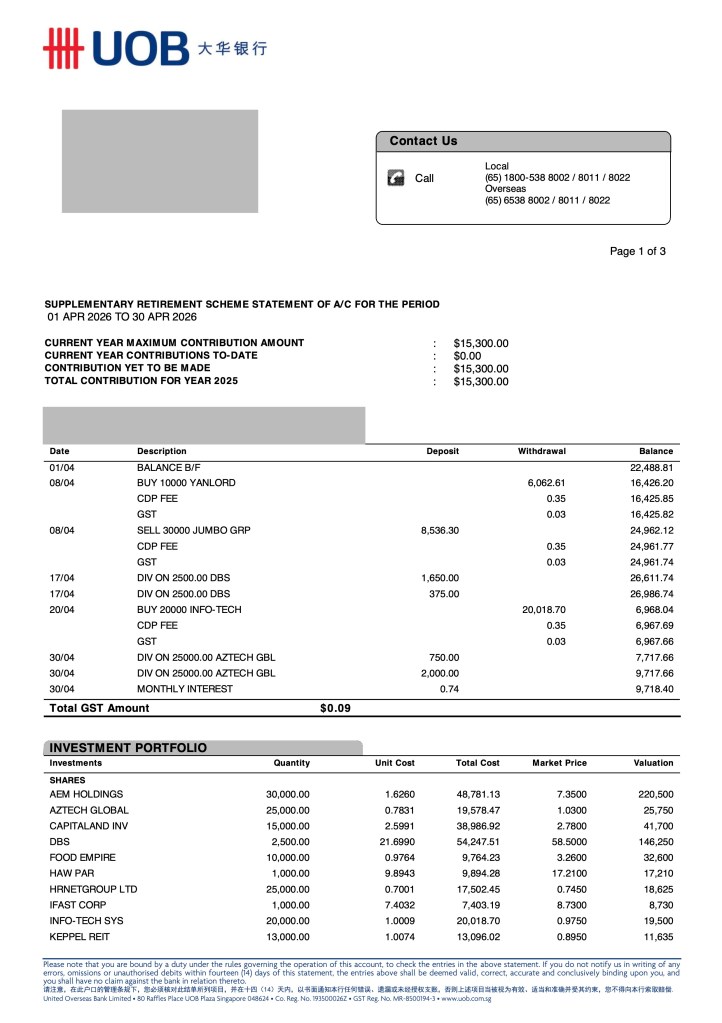

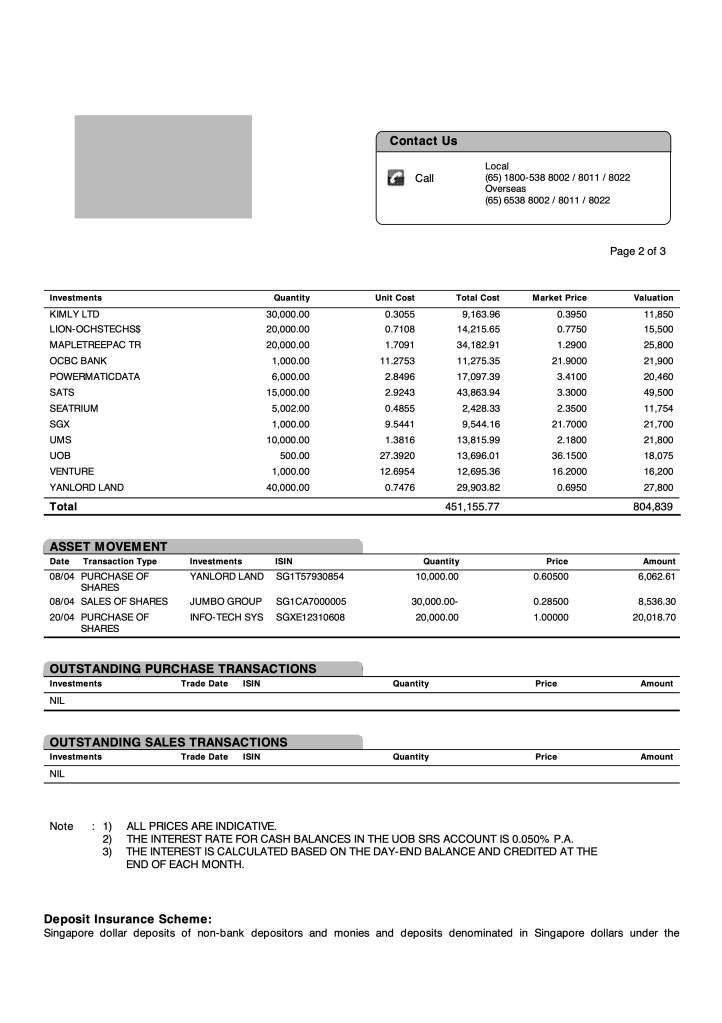

During the month of April, the SRS Fund added Yanlord and Info-Tech.

Info-Tech was also added back into the portfolio. This was partly a recognition of my earlier mistake in selling too early. The business continues to have strong long-term characteristics, supported by recurring revenue, digitalisation demand and a scalable software model.

The SRS Fund also exited Jumbo Group. The F&B sector remains challenging, with pressure from labour costs, rental costs and changing consumer behaviour. While Jumbo is a recognised brand, I prefer to allocate capital towards businesses with more sustainable long-term earning power and stronger scalability.

With these changes, the SRS Fund continues to optimise towards companies with stronger business quality, more durable earnings, and better long-term compounding potential.

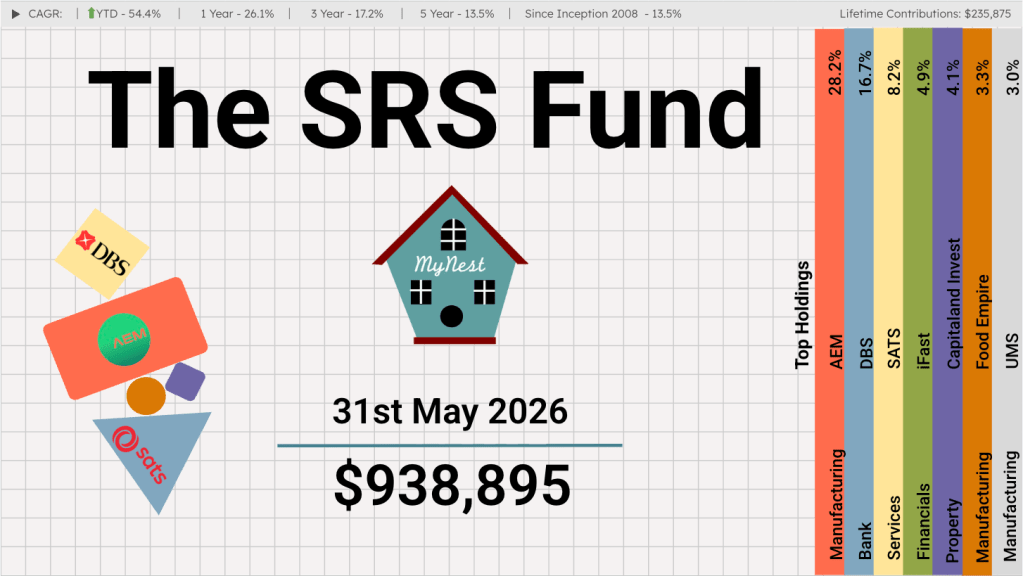

SRS Fund Performance vs. Benchmark

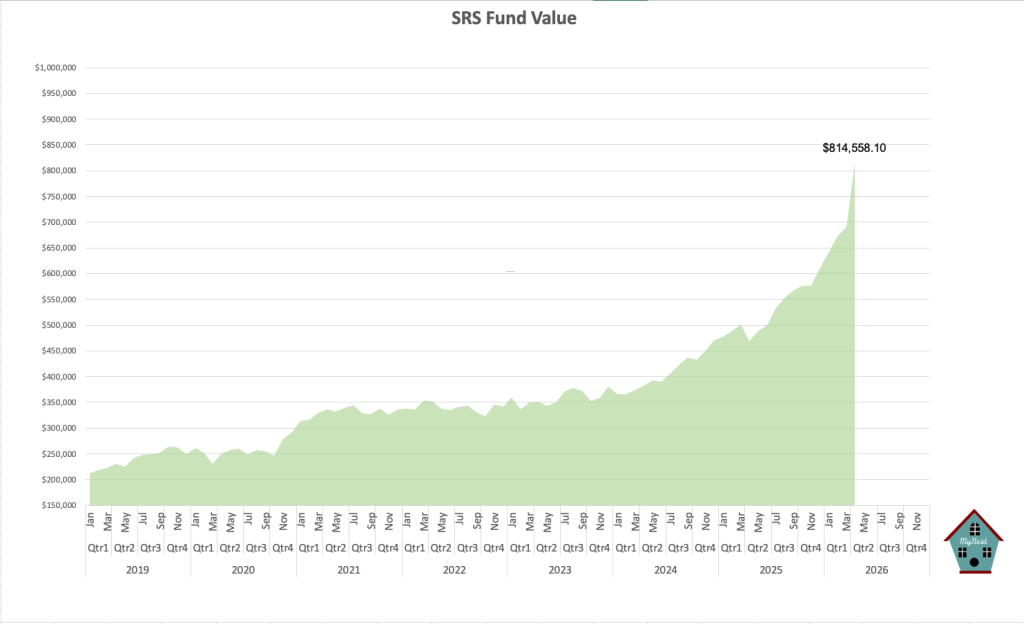

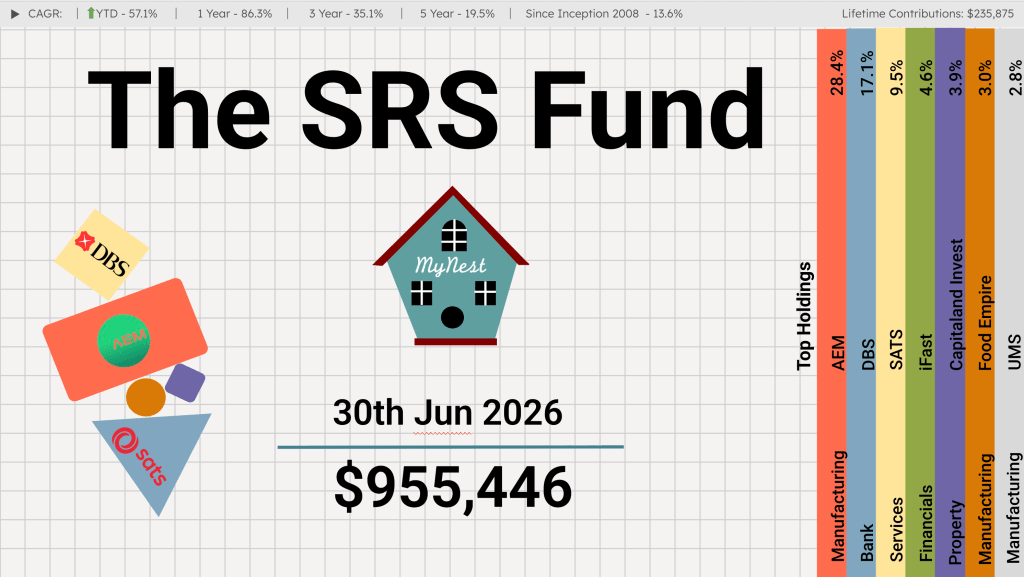

The SRS Fund delivered a strong return of 33.9% year-to-date as at 30 April 2026. Over the longer term, the Fund has compounded at 12.2% per annum since inception in 2008, with a current value of $814,558 against lifetime contributions of $235,875.

The recent outperformance was mainly driven by the sharp rise in AEM Holdings, which has become the Fund’s largest position. While this has meaningfully lifted the Fund’s value, it also means that near-term performance is now more sensitive to movements in AEM’s share price.

Performance Comparison

The SRS Fund left the benchmark Straits Times Index (STI) behind in the month of April. With AEM Holdings taking over as the largest component of the SRS Fund validating the intention of diversifying to segments other than finance and property.

| Metric | The SRS Fund | STI Index (Benchmark) |

| YTD Return (Apr 2026) | +33.9% | ~+7.2% |

| Cash Weighting | 1.2% | N/A |

| Top Holding | AEM Holdings (27.1%) | DBS (~25.9%) |

Portfolio Segments

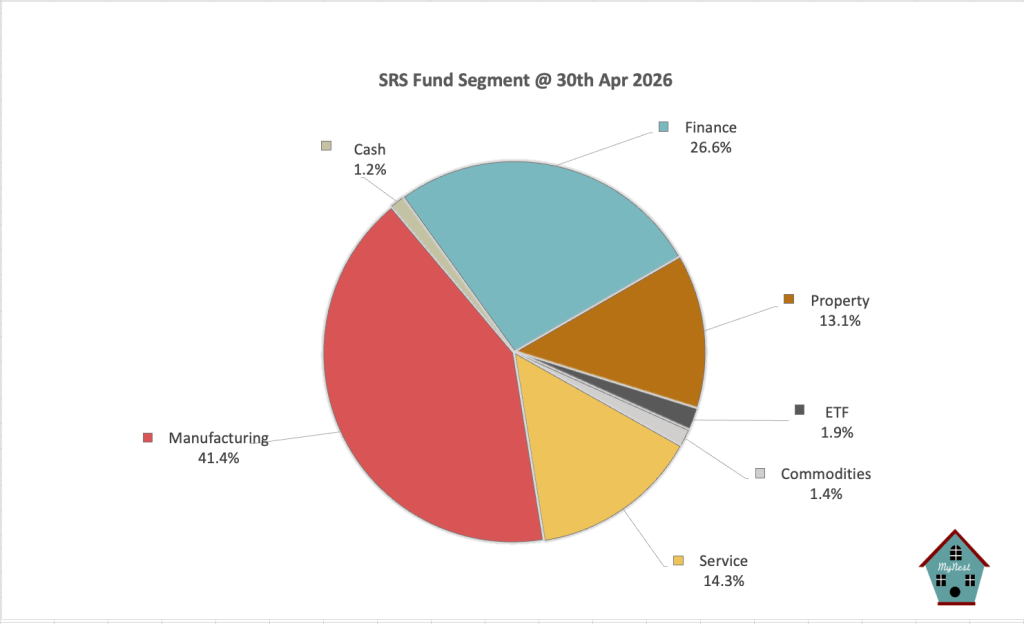

As at 30 April 2026, the largest segment exposure of the SRS Fund was Manufacturing, at 41.4% of the portfolio. This reflects the strong performance of several positions within the segment and the Fund’s exposure to areas such as industrial technology, electronics, testing and precision manufacturing. While the long-term growth potential remains attractive, the increased weighting also means that this segment will need to be monitored carefully.

The second-largest segment was Finance, at 26.6%. This remains an important foundation of the portfolio, providing stability, dividends and exposure to Singapore’s financial ecosystem. Finance also helps balance the more growth-oriented and cyclical parts of the Fund.

The Services segment accounted for 14.3% of the portfolio. This segment provides a mix of recurring revenue, recovery potential and regional growth opportunities. Over time, I hope this segment can contribute more steadily as the underlying businesses continue to scale.

The Property segment made up 13.1% of the portfolio. Within this segment, I continue to look for opportunities where assets are trading below intrinsic value, or where income and capital appreciation can combine to produce attractive long-term returns.

Dividends:

Dividends remain an important part of the SRS Fund’s long-term compounding engine.

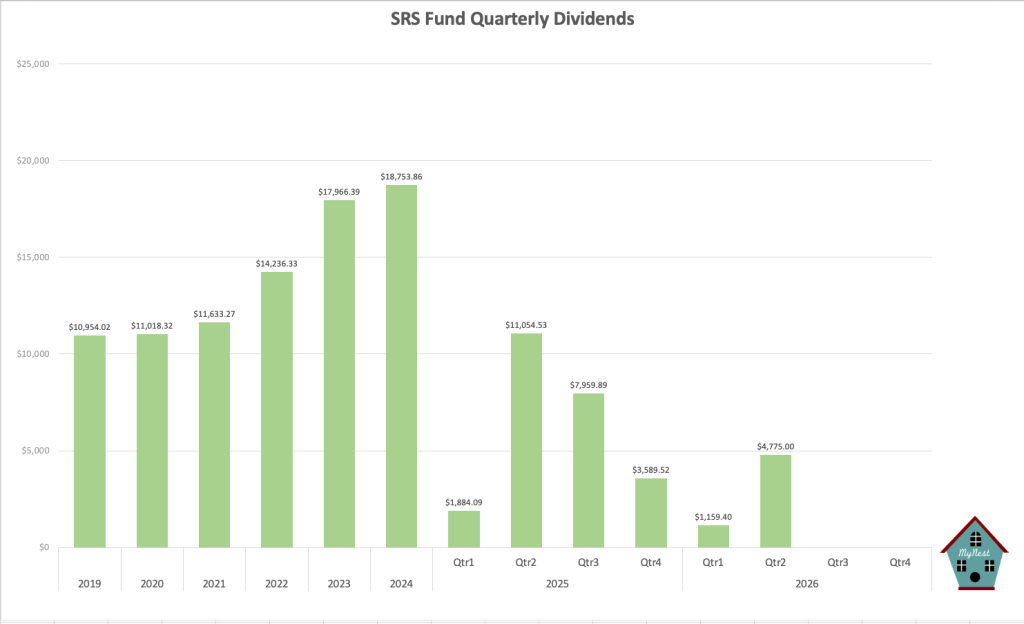

For 2026 year-to-date, the Fund has received $1,159.40 in Q1 dividends and $4,775.00 in Q2 dividends, bringing total dividends received so far to $5,934.40.

This is still early in the year, and the full-year dividend amount will depend on the timing and payout decisions of the portfolio companies. Historically, annual dividends have grown meaningfully, from around $10,954 in 2019 to $24,488.03 in 2025.

While the SRS Fund did not invest purely for dividends, I value dividends as a tangible return of capital and a useful discipline in portfolio construction. A healthy dividend stream provides flexibility, allows reinvestment during market weakness, and helps the SRS Fund compound without relying solely on capital gains.

The aim remains to build a portfolio that can deliver both capital appreciation and a growing stream of cash returns over time. In that sense, dividends are not the main objective, but they remain an important supporting pillar of the SRS Fund’s long-term journey.

SRS Fund Value

The SRS Fund went hyperbolic in April, closing above the $800,000 mark for the first time at $814,558.

For the month of April alone, the Fund added more than $100,000 in value — an exceptional monthly increase in the history of the SRS Fund. This sharp rise was largely driven by the strong performance of AEM Holdings, which has now become the largest position in the portfolio

While this milestone is encouraging, I remain very conscious that such a rate of increase is not sustainable over the long term. A portfolio does not compound in a straight line, and periods of sharp gains are often followed by higher volatility, consolidation, or even meaningful drawdowns.

Going forward, I expect the SRS Fund’s value to fluctuate more widely, especially given the larger exposure to AEM. The key is not to extrapolate April’s performance, but to stay focused on whether the underlying businesses continue to grow their earnings power over time.

Crossing $800,000 is an important milestone, but the real objective remains unchanged — to compound capital patiently and rationally over the long run.

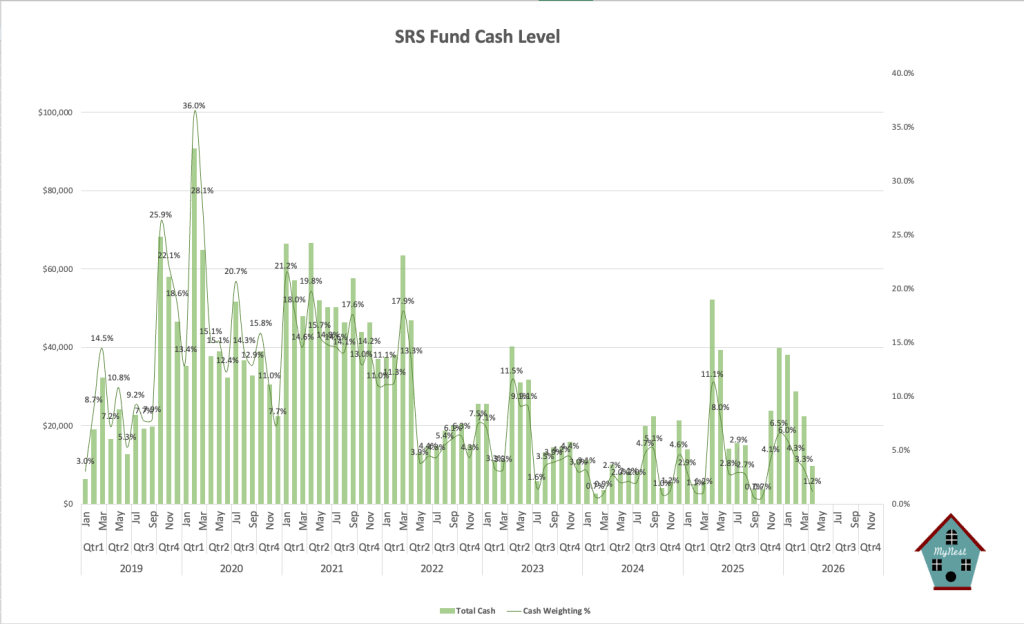

Cash Levels

The SRS Fund ended April with a cash level of 1.2%, which is close to the lower end of its historical range. This reflects the Fund’s more fully invested position after recent portfolio additions and the strong rise in share prices during the month.

While cash is currently low, I expect the cash position to improve gradually in the coming months. There should be a steady stream of dividends coming in during May and June, from companies in the portfolio. These dividends will help rebuild the SRS Fund’s cash buffer without requiring the sale of core holdings.

At the same time, the Manufacturing segment has become a very large part of the portfolio. Some of these positions have also risen sharply, causing valuations to become richer. If prices continue to move ahead of fundamentals, there may be opportunities to trim selected positions and add further to the cash pile.

A stronger cash position allows the SRS Fund to take advantage of future volatility, rebalance the portfolio when concentration becomes excessive, and reinvest patiently when better opportunities appear.

For now, the SRS Fund remains highly invested, but the combination of incoming dividends and possible trimming of richly valued positions should help restore a more comfortable cash level over time.

-

The SRS Fund Jun 2026

The month of Jun provided an important milestone in the Iran conflict. The agreement between the United States and Iran marked a significant step towards reducing geopolitical tension and reopening a clearer path for global energy flows

-

MyNest US Fund Jun 26

June was another remarkable month in the evolution of the global capitalism and the artificial intelligence investment cycle.

-

The SRS Fund May 2026

Korea, powered by the worldwide shortage and surge in memory demand, was hit directly by the AI wave, with its stock market more than doubling in a matter of 5 months. Taiwan, already the world’s most important advanced chip manufacturing hub has risen to become one of the largest stock market globally.

-

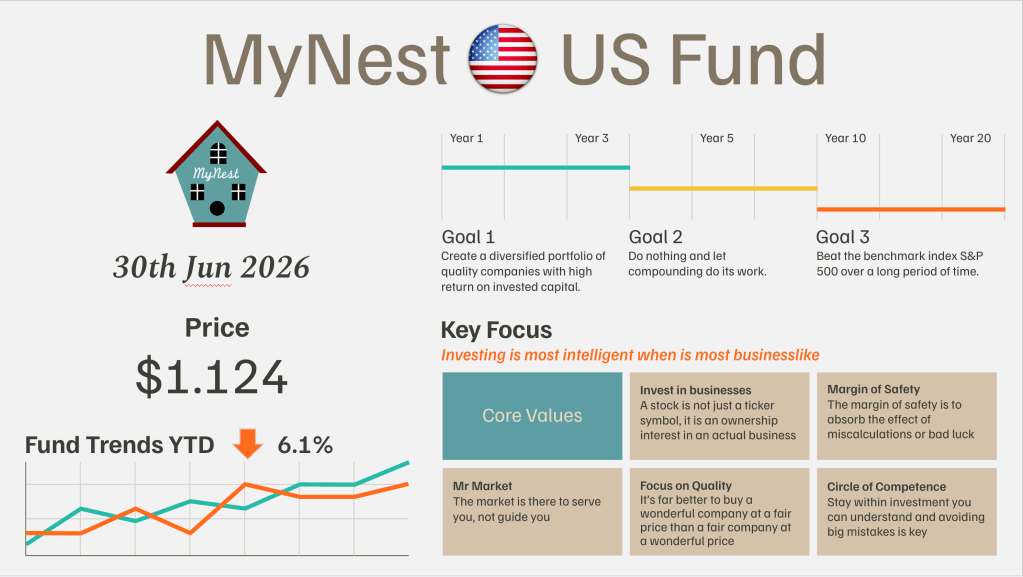

MyNest US Fund May 26

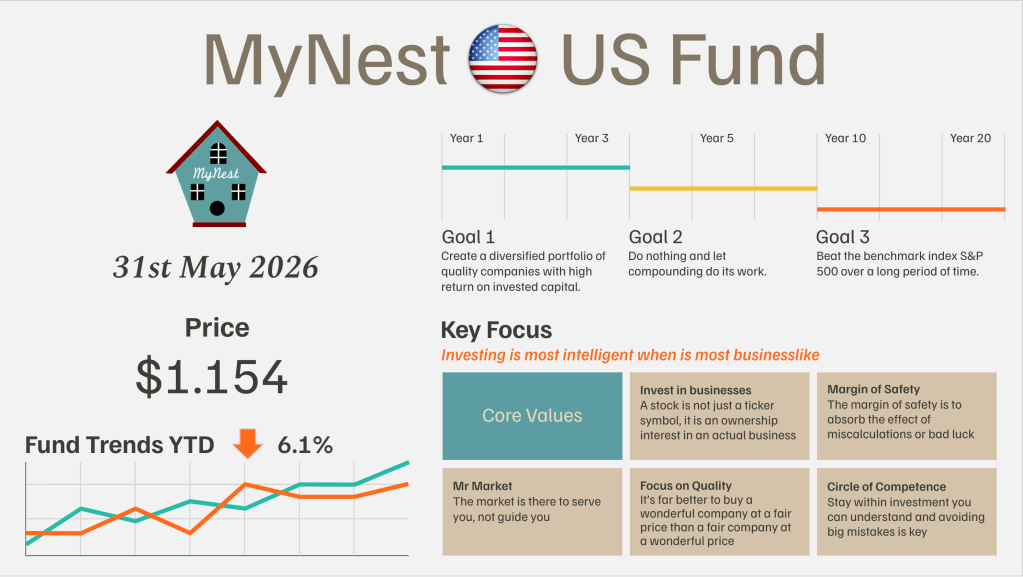

May has been an incredibly illuminating month for the MyNest US Fund. Looking across the broader landscape, the S&P 500 Index has continued its steady leg up, gaining +5.15% in the month of May alone to push its Year-to-Date (YTD) gain to +10.73%.

-

The SRS Fund Apr 2026

In my investment journey, there have been three occasions where I witnessed a company deliver a 10x return.

-

MyNest US Fund Apr 26

The market rebounded strongly in April as investors appeared to look past geopolitical uncertainty and renewed their focus on earnings, artificial intelligence, and the long-term growth prospects of quality businesses.