Has the AI Tsunami Finally Reached Singapore’s Shore?

Across Asia, the impact has been uneven. Korea, powered by the worldwide shortage and surge in memory demand, was hit directly by the AI wave, with its stock market more than doubling in a matter of 5 months. Taiwan, already the world’s most important advanced chip manufacturing hub has risen to become one of the largest stock market globally.

Singapore, however has not been at the centre of the AI storm

Our market’s traditional strength lies in banks, property, REITs and yield driven companies. These sectors have benefited only indirectly from AI. DBS, UOB and OCBC remain strong compounders, but they are not the first names that come to mind when global investors think about AI infratructure

Yet even on this little red dot, there has been an AI aftershock.

A smallgroup of Singapore-listed manufacturers serving the semiconductor and electronics supply chain has been swept up by this wave. For the SRS Fund, the most important of these businesses has been AEM Holdings.

AEM‘s 1Q2026 investor update confirms that the multi-year AI and High Performance Computing (HPC) earnings cycle is no longer a forward looking theory but activitly hitting the income statement. The numbers show a company experiencing structural business dynamics changes.

More importantly, management revised its FY2026 revenue guidance sharply upward to a range of $550m – $600m. This implies an aggressive 38% – 50% YoY revenue expansion signaling that the underlying order book is strengthening.

From a structural standpoint, the most vital development is the strategic partnership with ASE, the world’s largest OSAT commanding a 45% global market share. This partnership elegantly solves AEM’s historical single customer concentration risk by utilising ASE’s massive footprint to unlock direct access to tech hyperscalers that were previously completely out of reach.

Trimming & Prudent Rebalancing

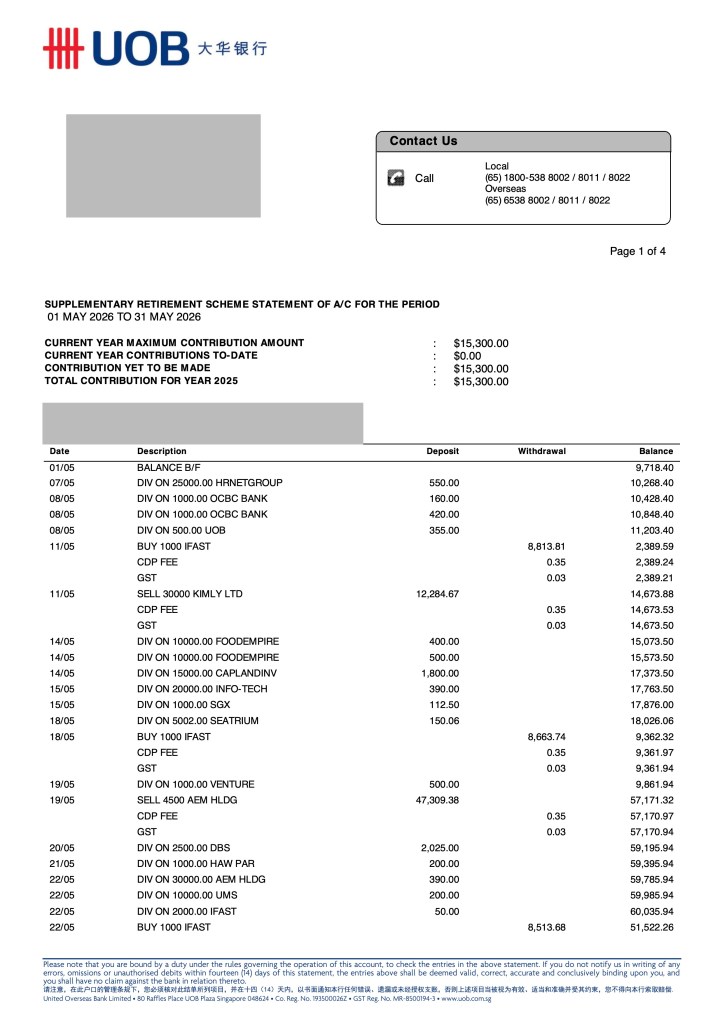

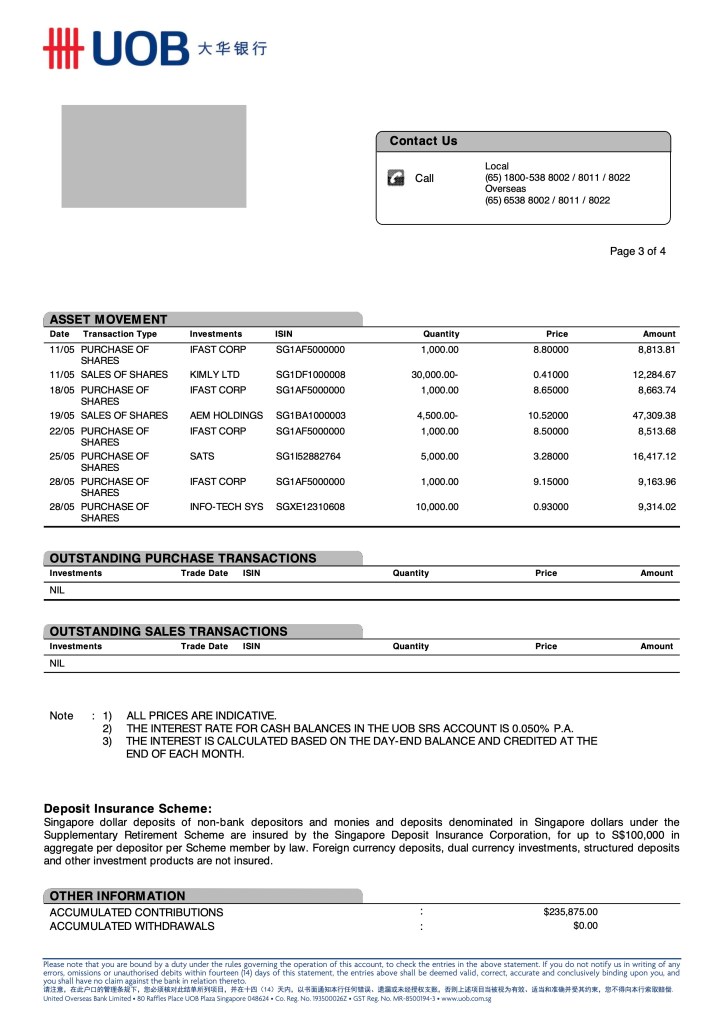

Despite everything going perfectly for AEM Holdings, I have slightly trimmed the position selling 15% of the position at $10.52. By executing this sale, the SRS Fund’s entire initial capital has been clawed back, completely de-risking the position. The emotional burden of loss aversion is entirely eliminated. Knowing that the downside is mathematically zero and the principal is safely preserved will improve the psychological resilience during draw downs and comfortably sit tight for the full multi-year ride.

The proceeds were redeployed into several counters including iFast, SATS as well as Info-Tech.

The SRS Fund also exited completly exited Kimly after a spike in share price following a DBS research report. Overall, I am glad the SRS Fund is now free of F&B businesses.

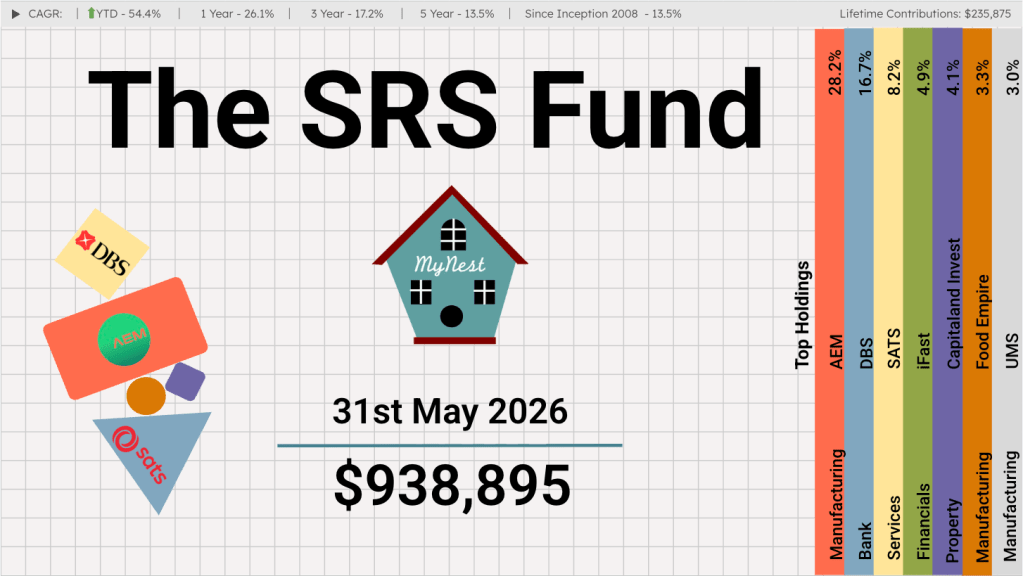

SRS Fund Performance vs. Benchmark

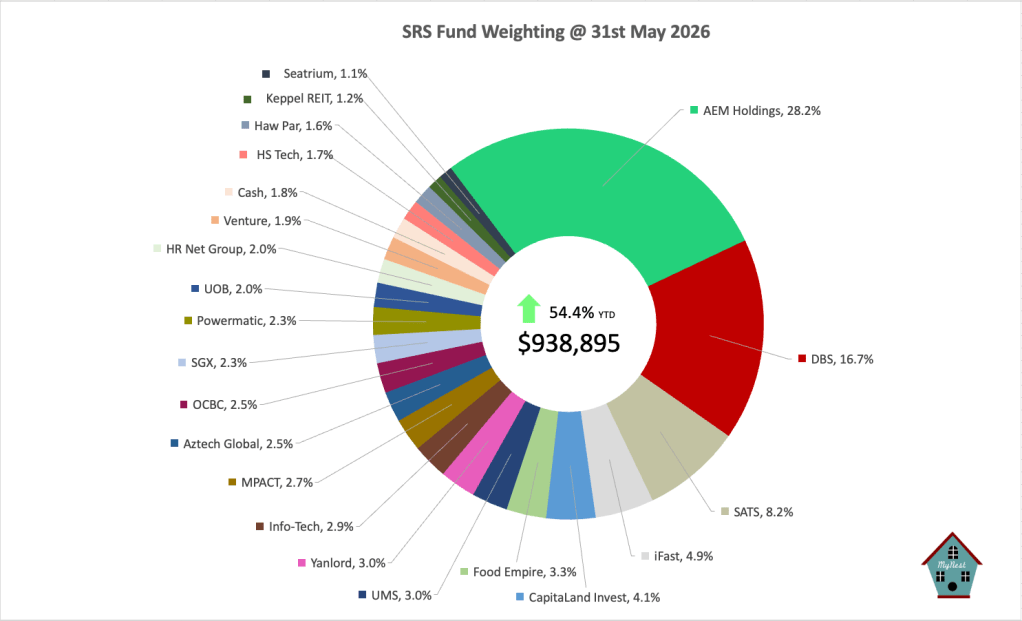

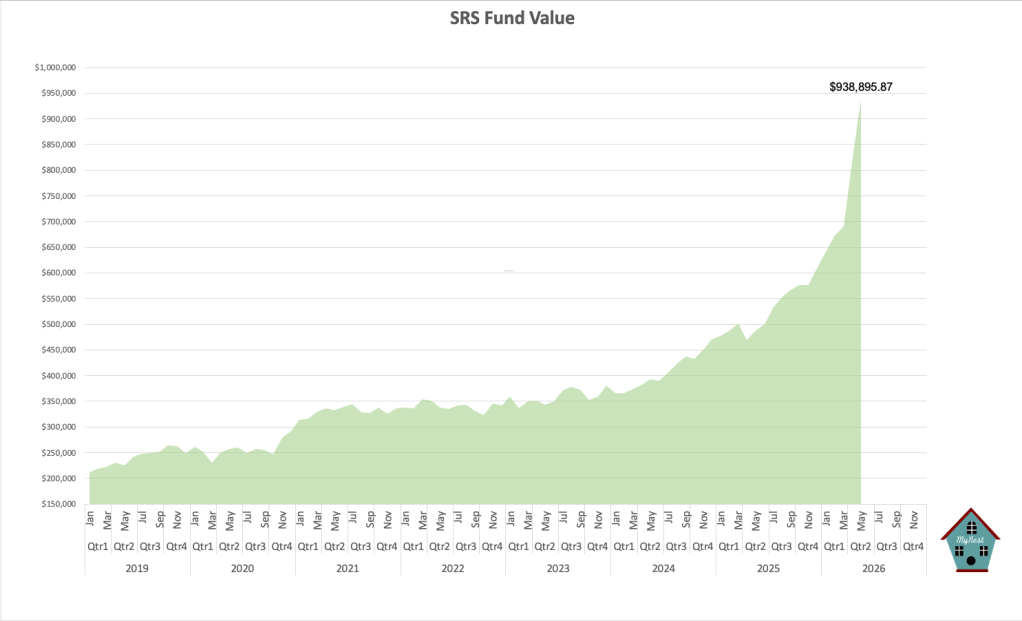

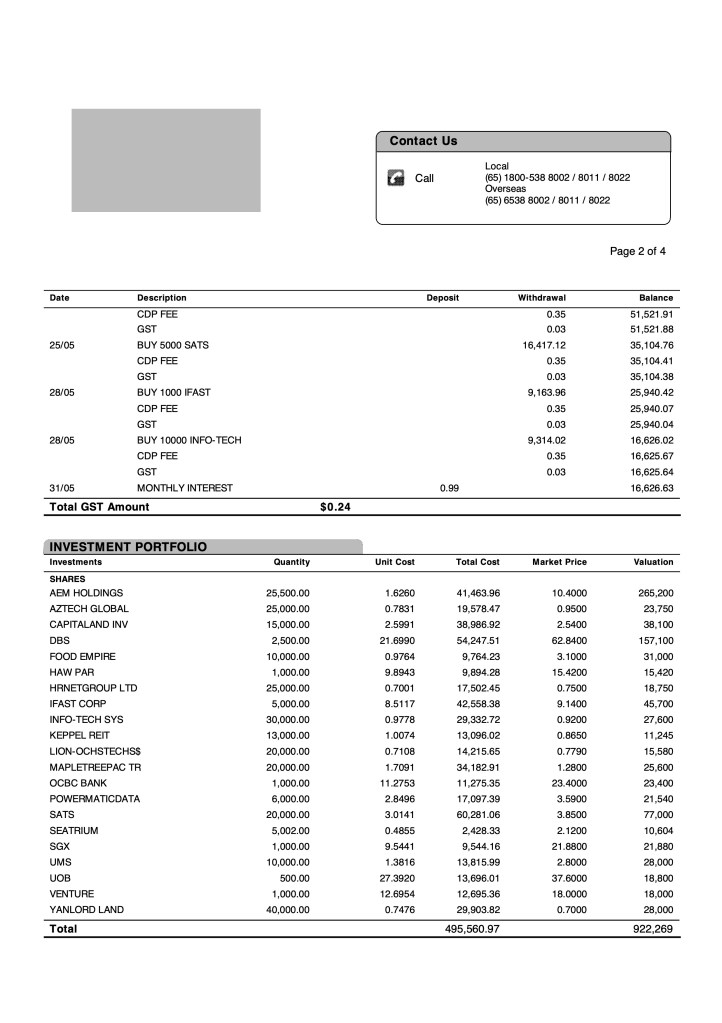

As at 31st May 2026, the SRS Fund value stood at $938,895.87, up 54.4% YTD. AEM Holdings remain the largest position despite our trimming accounting for 28.2% of the SRS Fund. Together with other manufacturing related holdings such as UMS, Aztech Global, Venture and Powermatic.

The recent outperformance was mainly driven by the sharp rise in AEM Holdings, which has become the Fund’s largest position. While this has meaningfully lifted the Fund’s value, it also means that near-term performance is now more sensitive to movements in AEM’s share price.

Performance Comparison

The SRS Fund continue to surge faster than benchmark Straits Times Index (STI) in the month of May. With AI related counters and financials driving much of the SRS Fund’s performance.

| Metric | The SRS Fund | STI Index (Benchmark) |

| YTD Return (Apr 2026) | +54.4% | ~+10.8% |

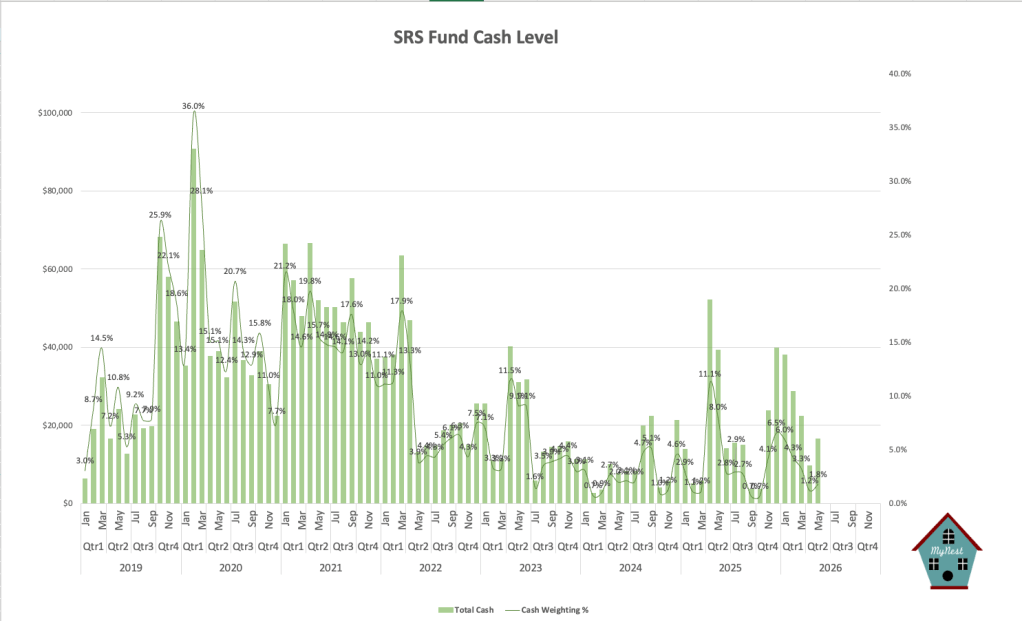

| Cash Weighting | 1.8% | N/A |

| Top Holding | AEM Holdings (28.2%) | DBS (~26.6%) |

Portfolio Segments

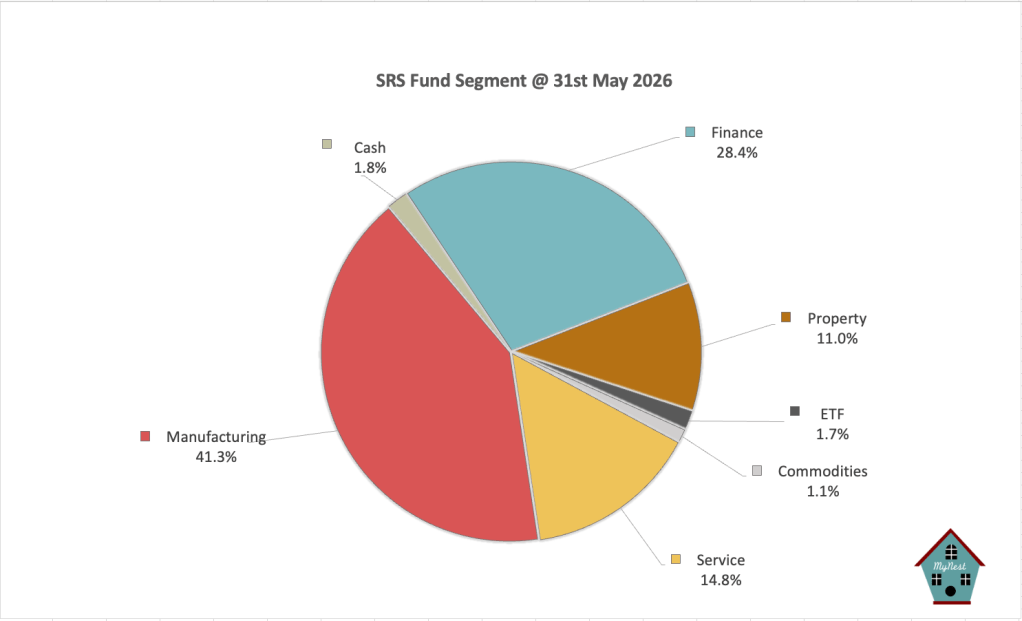

For many years, the SRS Fund was built around Singapore’s classic strengths: banks, REITs, property-related names and steady dividend payers. Those remain important. The Finance segment still represent 28.4% of the portfolio, led mainly by DBS, OCBC, UOB, iFast & SGX.

Property-related holdings account for another 11%, while the Service segment contributes 14.8%, led by SATS and HR Net Group.

The Services segment accounted for 14.3% of the portfolio. This segment provides a mix of recurring revenue, recovery potential and regional growth opportunities. Over time, I hope this segment can contribute more steadily as the underlying businesses continue to scale.

The Property segment made up 13.1% of the portfolio. Within this segment, I continue to look for opportunities where assets are trading below intrinsic value, or where income and capital appreciation can combine to produce attractive long-term returns.

The biggest driver of performance this year has clearly been the semiconductor manufacturing exposure.

Dividends:

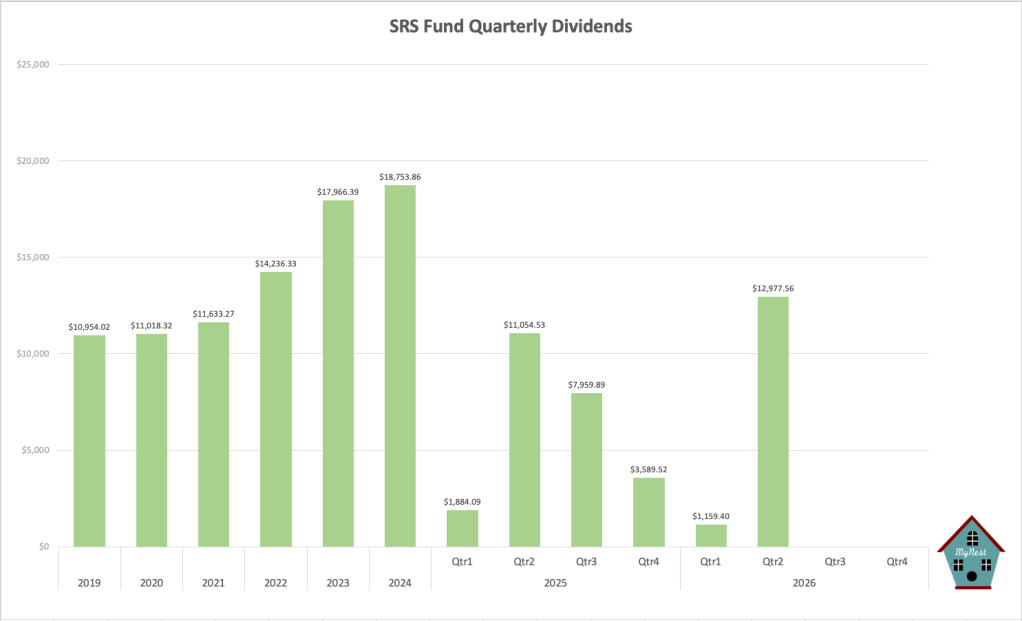

On the income side, dividends remain an important part of the SRS Fund’s foundation. Dividend received in Q2 so far is $12,977.56, following Q1 collection of $1,159.40. While the SRS Fund is not purely an income portfolio, dividends provide psychological comfort and help reinforce the idea that these are real businesses generating real cash returns.

SRS Fund Value

The SRS Fund has come a long way since 2019, when the fund value was just above the $200k mark. Today, at close to $940k the compounding effect is becoming more visible. The recent acceleration has been unusually strong and I do not expect every year to look like 2026. Markets do not move in straight lines and sectors that are loved today can quickly become crowded tomorrow.

Cash Levels

Cash remains low at 1.8%, which shows that the fund is almost fully invested. This has helped performance during the rally, but it also means the SRS Fund has limited dry powder if volatility returns. Historically, the SRS Fund has gone through periods with much higher cash levels. Today’s low cash position reflects the strength of the current opportunity set but it also requires discipline.

The lesson from May is simple: Singapore may not be the centre of the AI boom, but selected Singapore companies can still benefit from the global semiconductor supply chain. The challenge now is not whether the SRS Fund has captured the wave but whether I can manage the concentration, valuation and expectations wisely from here.

-

The SRS Fund May 2026

Korea, powered by the worldwide shortage and surge in memory demand, was hit directly by the AI wave, with its stock market more than doubling in a matter of 5 months. Taiwan, already the world’s most important advanced chip manufacturing hub has risen to become one of the largest stock market globally.

-

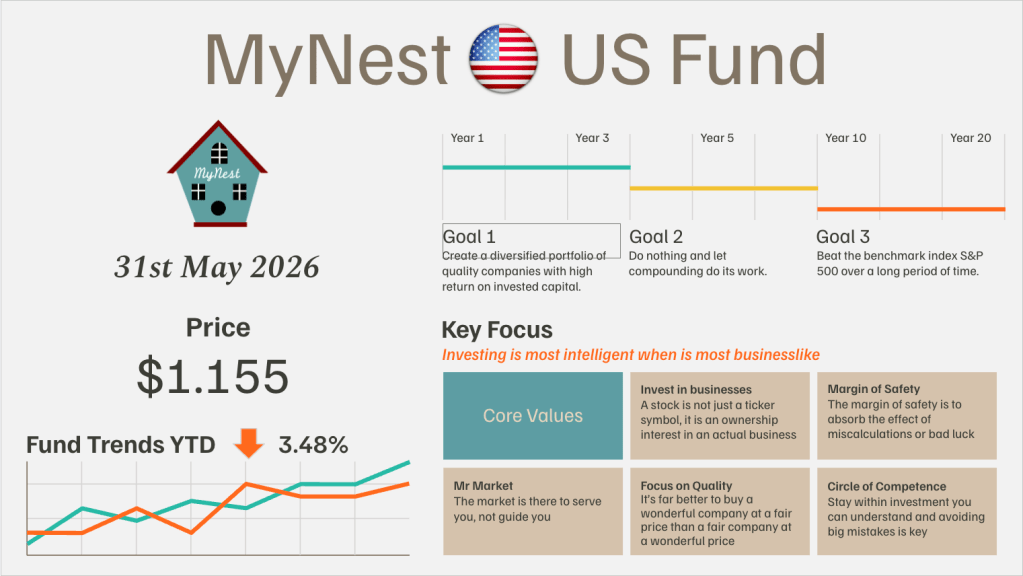

MyNest US Fund May 26

May has been an incredibly illuminating month for the MyNest US Fund. Looking across the broader landscape, the S&P 500 Index has continued its steady leg up, gaining +5.15% in the month of May alone to push its Year-to-Date (YTD) gain to +10.73%.

-

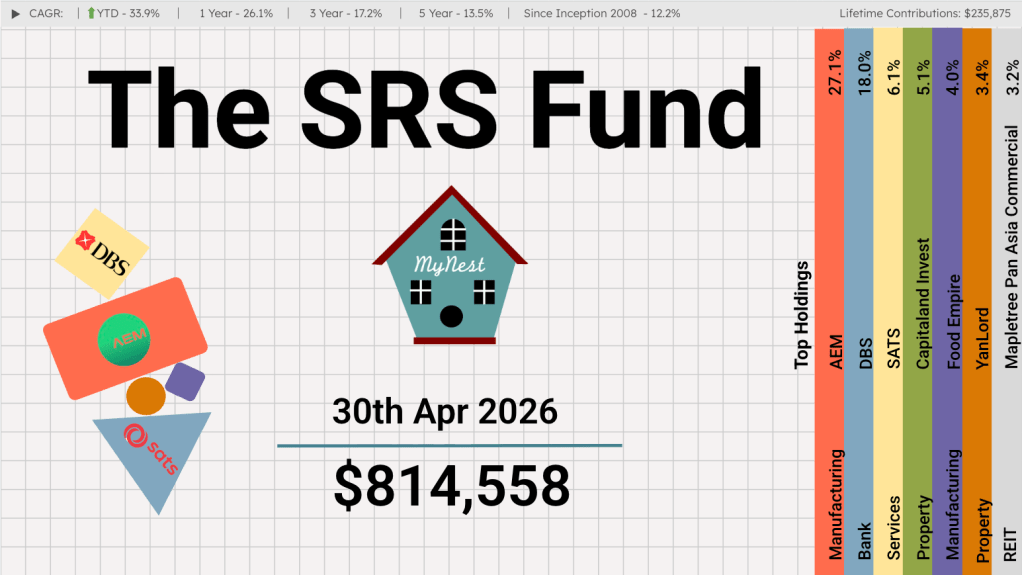

The SRS Fund Apr 2026

In my investment journey, there have been three occasions where I witnessed a company deliver a 10x return.

-

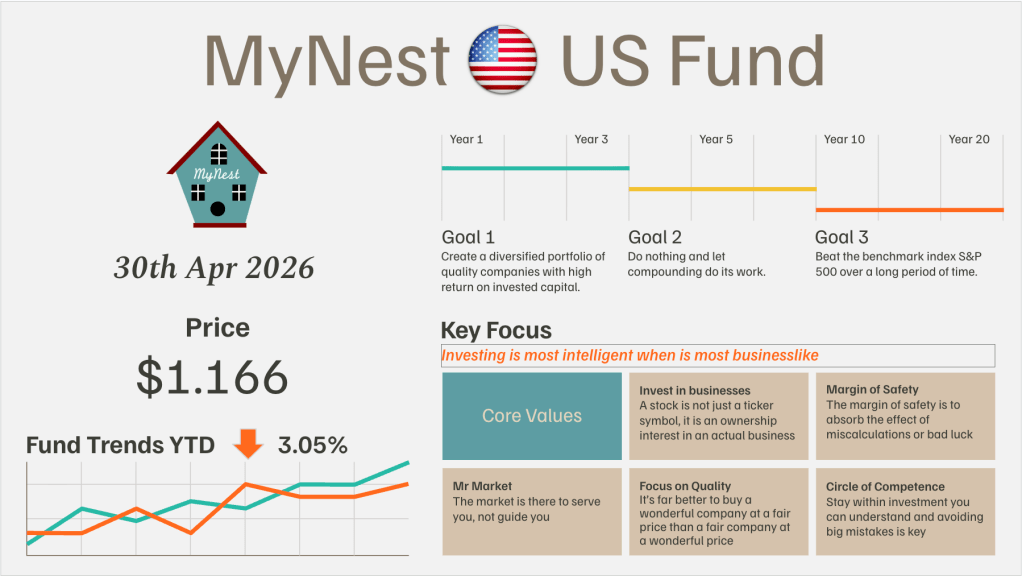

MyNest US Fund Apr 26

The market rebounded strongly in April as investors appeared to look past geopolitical uncertainty and renewed their focus on earnings, artificial intelligence, and the long-term growth prospects of quality businesses.

-

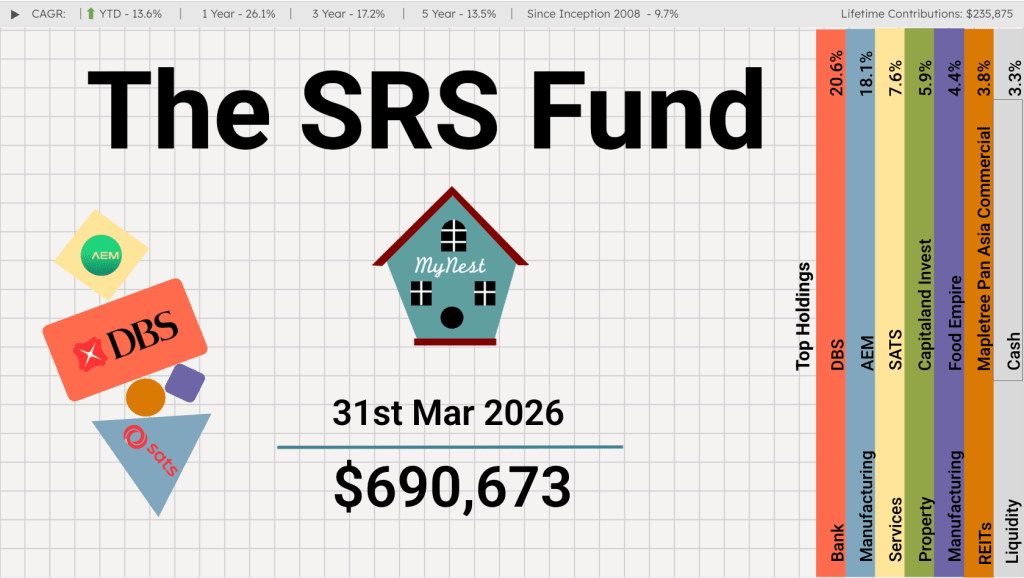

The SRS Fund Mar 2026

It is an enduring market reality that a concentrated minority of holdings drives the vast majority of returns. For years, DBS (currently the largest individual holding at 20.6%) has served as the compounding engine of the SRS Fund.

-

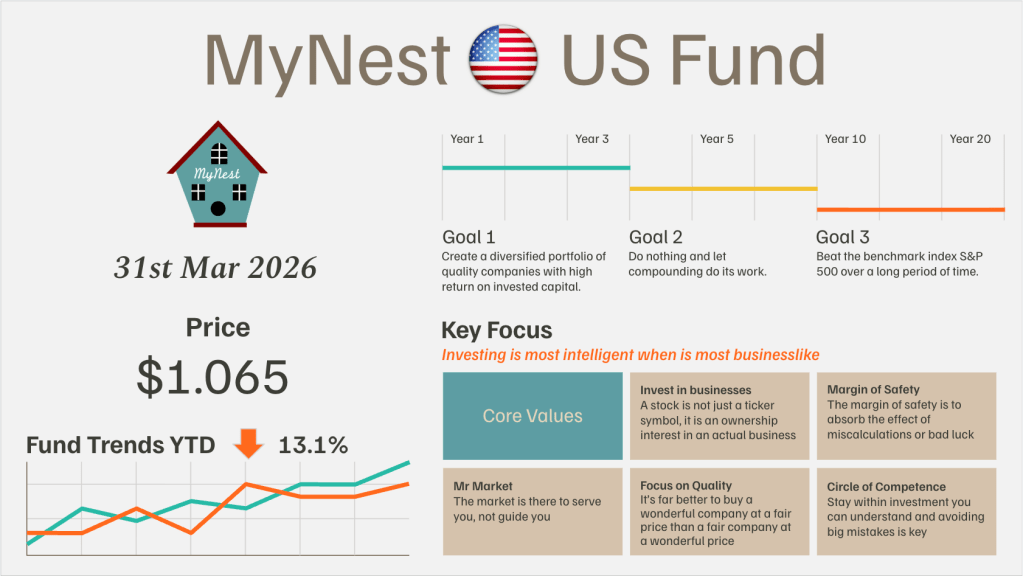

MyNest US Fund Mar 26

March shattered any lingering market complacency, pivoting sharply from the localized damage of the “SaaS-pocalypse” to a systemic shock driven by the war in Iran.