Dear Investors,

June was another remarkable month in the evolution of the global capitalism and the artificial intelligence investment cycle.

The month saw one of the largest capital raises in modern market history. Alphabet, the parent company of Google, announced plans to raise around US$80 billion to fund its expanding AI infrastructure ambitions. As part of this raise, Berkshire Hathaway committed US$10 billion through a private placement – a meaningful vote of confidence from one of the world’s most disciplined allocators of capital.

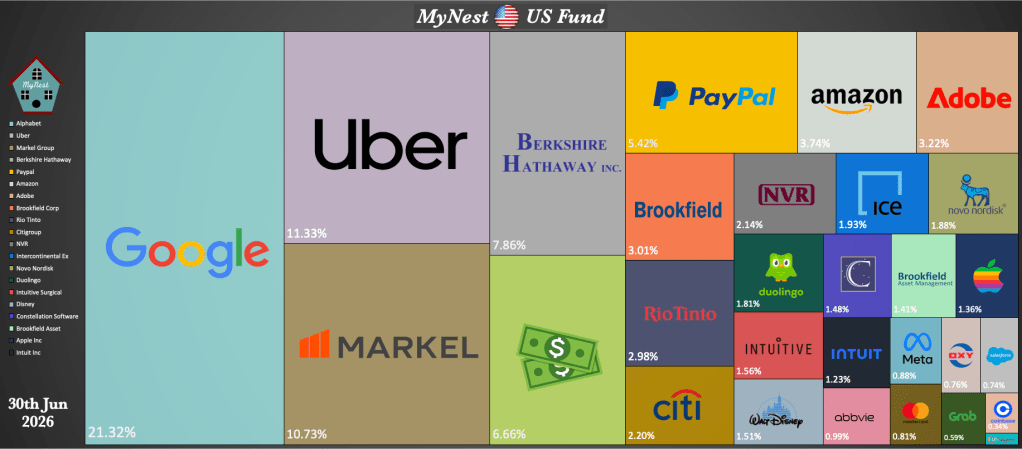

For us, this was especially interesting because Alphabet remain our largest holding at 21.32% of the fund. While many investors continue to debate the eventual profitability of AI, the reality is that the largest technology platforms are now committing capital at a scale that only a handful of companies in the world can afford. Alphabet’s decision reinforces the idea that AI is no longer merely a product feature. It is becoming the next layer of global infrastructure.

Closely following that was the historic IPO of SpaceX, which raised roughly US$75-86 billion depending on the reported structure, making it one of the largest public listings in history. The listing also pushed Elon Musk briefly into trillionaire status, a milestone never before seen in human history.

While life for Elon Musk may not change very much – the mission to Mars continues – this moment is deeply symbolic. It represents society’s willingness to place an extraordinary amount of financial resources behind one individual’s vision. I hope history will look kindly on this act of faith: that by backing such ambition, humanity may one day become an interplanetary species and strengthen the long term survival of the human race.

The AI Wave and Our Underperformance

June also saw a continued surge of investor interest in the semiconductor space. This single category has been one of the main forces pushing the broader index to new highs this year.

Here, I must honestly admit that I did not foresee the magnitude and speed of this semiconductor-led rally. This remains the main reason for our underperformance so far in 2026. The S&P 500 has been increasingly driven by companies directly exposed to AI chips, memory, advanced packaging and semiconductor infrastructure.

Our portfolio, by design, owns more of the downstream software, cloud, marketplace, insurance and capital light compounders rather than the most direct hardware beneficiaries.

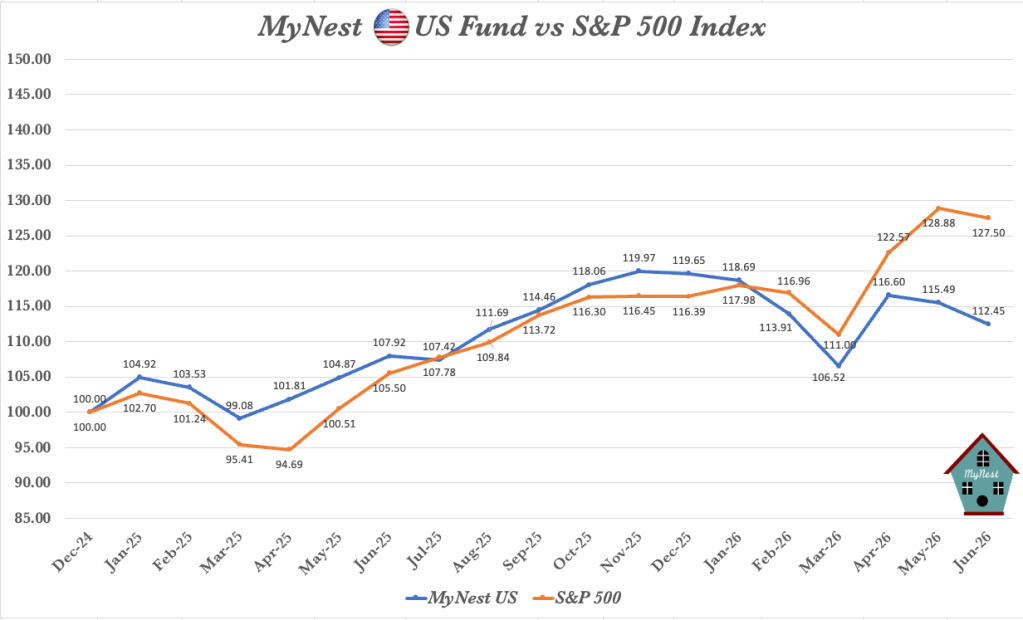

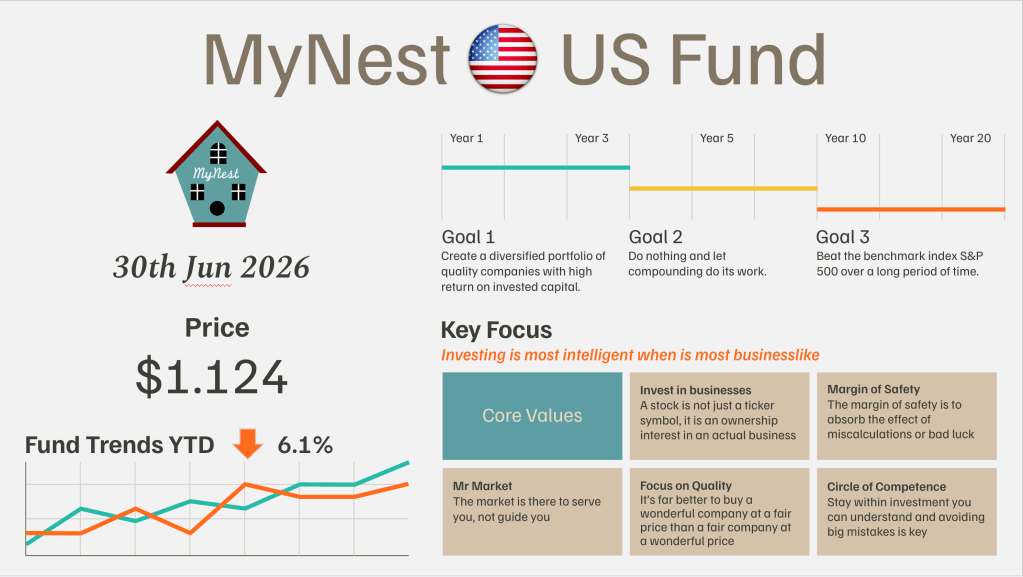

For the month of June, MyNest US Fund declined from $1.154 to $1.124, down -6.1% YTD. In contrast the S&P 500 is up 10.2% including dividend.

This is clearly not a satisfactory short term outcome. However, I continue to believe that the long term quality of the businesses we own remain intact.

Portfolio Activity: Adding to Uber

During the month, I added to our Uber position through the assignment of an option.

Uber is now our second largest holding at 11.33% of the fund. I continue to see Uber as a long term compounder with an increasingly attractive business model. The growth of Uber One is particularly important. What started as a ride hailing and food delivery platform is gradually developing characteristics that resemble a scaled economic sharing model.

In some ways, Uber One carries elements of what has worked so well for Costco and Amazon Prime: a membership layer that increases customer frequency, improves retention and deepens the relationship between the platform and the user. As Uber’s ecosystem expands across mobility, delivery, advertising and potentially other local services, the value of this membership base could become increasingly meaningful over time.

While the market may be focused on the immediate AI hardware winners, I remain comfortable owning businesses like Uber where the long term unit economics, network effects and customer behaviour continue to improve.

The Heavy Weights

Our top positions remain highly concentrated in businesses where we have strong long term conviction:

Circle of Competence & Intrinsic Value

- Alphabet – 21.32%

Alphabet remains our largest position. The company is at the centre of advertising, cloud computing, AI infrastructure, and digital distribution. The recent capital raise highlights both the opportunity and the intensity of competition in AI. - Uber – 11.33%

Uber continues to evolve from a transactional platform into a deeper consumer ecosystem. Uber One remains an important part of this thesis. - Markel Group – 10.73%

Markel remains one of our core insurance compounders. It provides underwriting discipline, long-term capital allocation, and exposure to a business model that can compound steadily over time. - Berkshire Hathaway – 7.86%

Berkshire continues to serve as a stabilising anchor in the portfolio. The company’s involvement in Alphabet’s capital raise is also a reminder of its willingness to act when it sees an attractive long-term opportunity.

Segment Chart

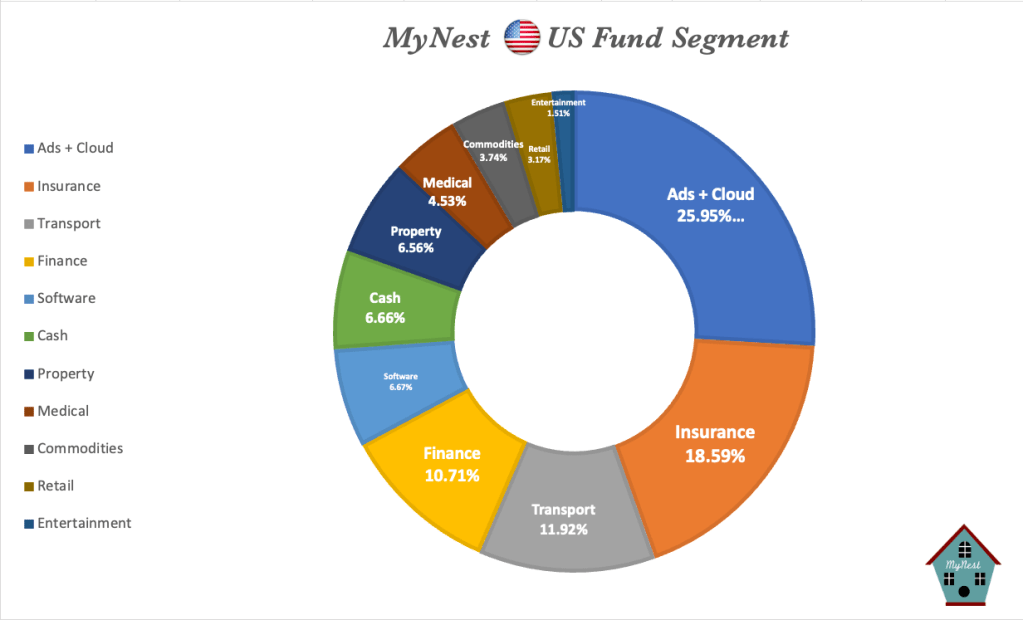

Our portfolio remains intentionally diversified across several core engines of compounding.

The largest segment remains Ads + Cloud at 25.95%, mainly represented by Alphabet, Amazon, Meta, and Salesforce. This remains our key exposure to the digital economy and AI-enabled software infrastructure.

Insurance accounts for 18.59%, mainly through Markel, Berkshire Hathaway, Brookfield, and related holdings. This remains a core part of our long-term compounding engine.

Transport accounts for 11.92%, largely driven by Uber. This segment reflects our belief that platform businesses with strong network effects can create durable long-term value.

Finance accounts for 10.71%, followed by Software at 6.67%, Cash at 6.66%, and Property at 6.56%.

Closing Thoughts

The first half of 2026 has been humbling. The market has rewarded a very specific area of the economy: AI hardware and semiconductor infrastructure. We have participated in the broader AI story through Alphabet, Amazon, Adobe, Intuit, Constellation Software, Salesforces and other software and cloud related businesses. However, we have not owned enough of the direct semiconductor winners and that has hurt our relative performance.

As investors, we must be honest about what we miss, but also disciplined about not chasing what we do not fully understand or where valuation no longer provides sufficient margin of safety.

Our approach remain unchanged. We aim to own high quality businesses, run by capable management teams, with durable competitive advantages, strong cash generation and long runways for reinvestment. There will be periods where this approach lags a narrow and speculative market. But over the long term, I believe discipline, patience and rational capital allocation remain our best path forward.

Lastly I would like to thank you for your trust and continued support.

-

MyNest US Fund Jun 26

June was another remarkable month in the evolution of the global capitalism and the artificial intelligence investment cycle.

-

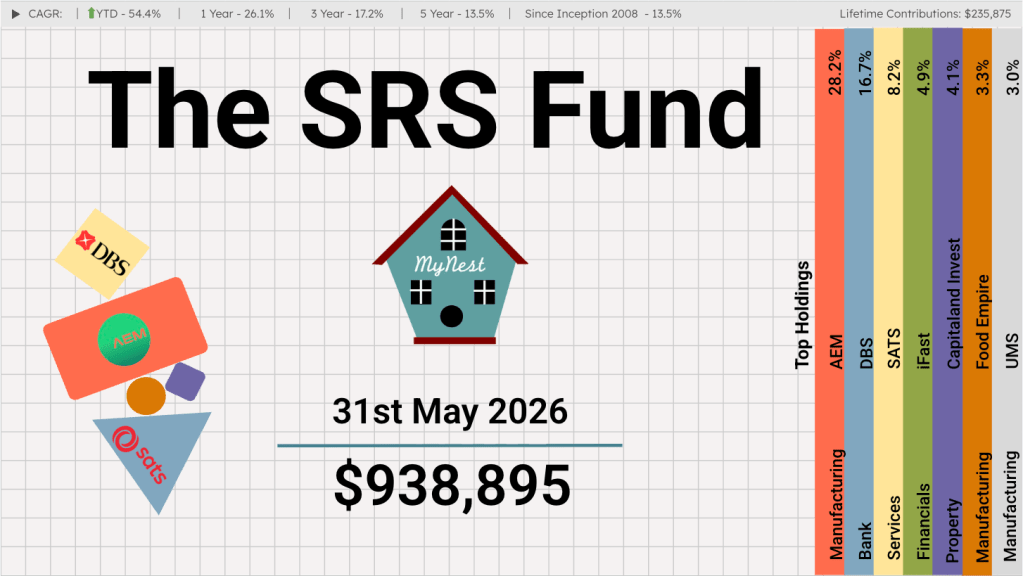

The SRS Fund May 2026

Korea, powered by the worldwide shortage and surge in memory demand, was hit directly by the AI wave, with its stock market more than doubling in a matter of 5 months. Taiwan, already the world’s most important advanced chip manufacturing hub has risen to become one of the largest stock market globally.

-

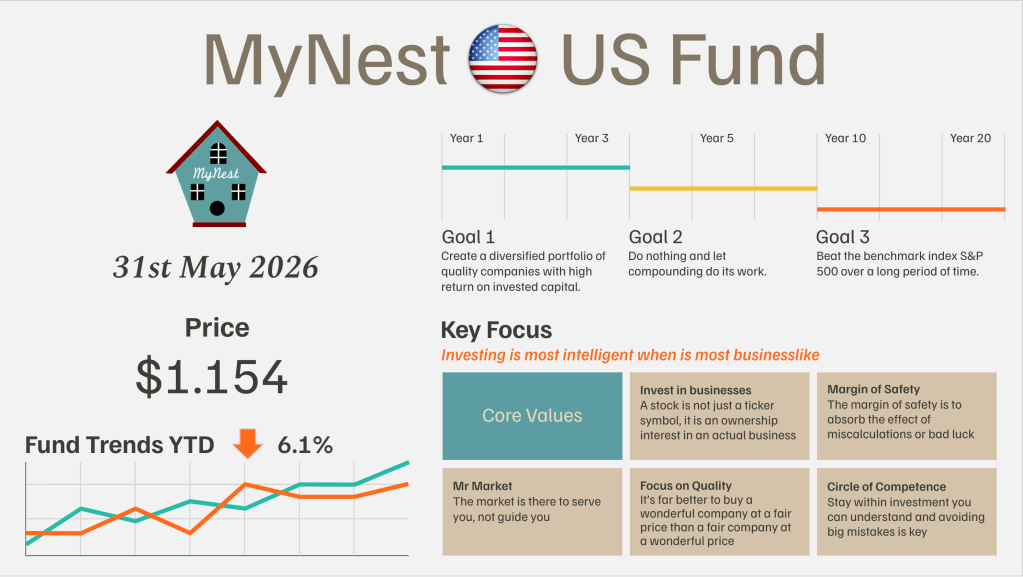

MyNest US Fund May 26

May has been an incredibly illuminating month for the MyNest US Fund. Looking across the broader landscape, the S&P 500 Index has continued its steady leg up, gaining +5.15% in the month of May alone to push its Year-to-Date (YTD) gain to +10.73%.

-

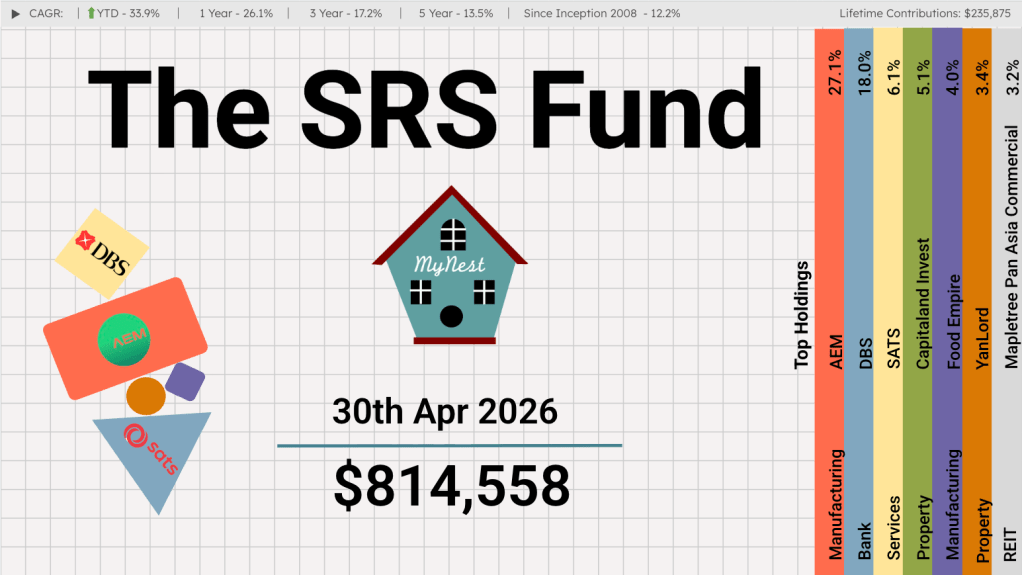

The SRS Fund Apr 2026

In my investment journey, there have been three occasions where I witnessed a company deliver a 10x return.

-

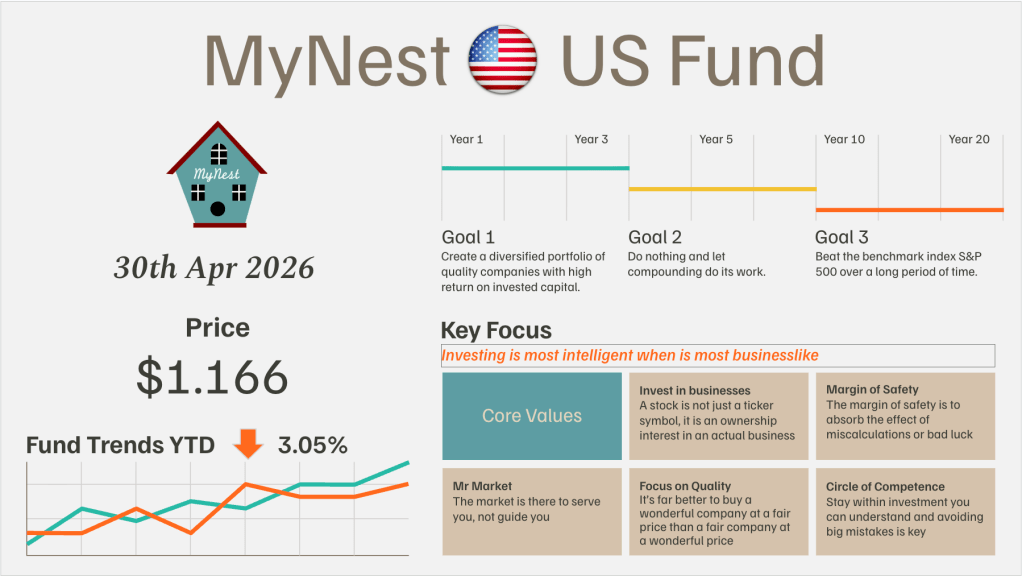

MyNest US Fund Apr 26

The market rebounded strongly in April as investors appeared to look past geopolitical uncertainty and renewed their focus on earnings, artificial intelligence, and the long-term growth prospects of quality businesses.

-

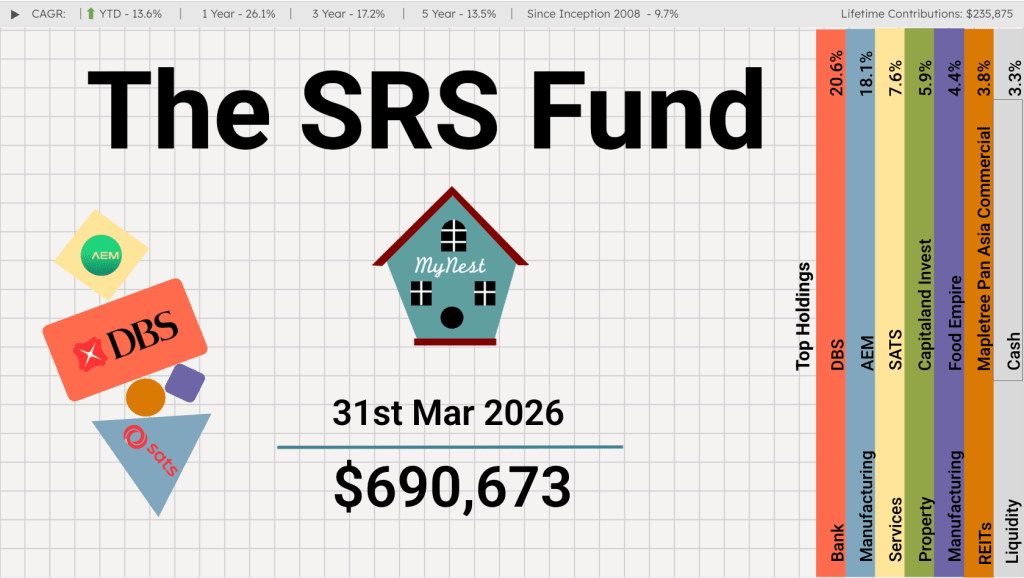

The SRS Fund Mar 2026

It is an enduring market reality that a concentrated minority of holdings drives the vast majority of returns. For years, DBS (currently the largest individual holding at 20.6%) has served as the compounding engine of the SRS Fund.