Certainty Returns, But Discipline Still Matters

The month of Jun provided an important milestone in the Iran conflict. The agreement between the United States and Iran marked a significant step towards reducing geopolitical tension and reopening a clearer path for global energy flows.

As a result, oil prices retreated from their earlier elevated levels, providing some relief for many economies and businesses that are sensitive to fuel and transport costs.

More importantly, it offered markets something that has been in short supply — certainty.

This development lifted a dark cloud hanging over SATS, our global air cargo handler.

Readers may recall that I added to the SATS position in the SRS Fund towards the end of last month at around the $3.20 level, just before its results announcement. At the time, the market appeared concerned that the Middle East conflictwould hurt air traffic and weigh on SATS’ recovery story. However, SATS’ full-year financial results painted a more nuanced picture.

Conventional wisdom suggests that air traffic and aviation-related businesses should suffer during periods of geopolitical disruption. Yet SATS’ results showed that its global network can also benefit from disruption when cargo flows are diverted and customers require more flexible routing options.

Gateway Services remained resilient, supported by strong cargo demand, market share gains and the scale of the WFS network. This further strengthens the argument that the WFS acquisition was a rational and strategic move.

The market had punished SATS for acquiring a business much larger than itself, but the acquisition has transformed SATS from a Singapore-centric aviation services provider into a global air cargo and gateway services platform. In a fragmented and uncertain world, that global network may prove to be a strength rather than a burden.

Market Front

On the market front, June was a month of consolidation for many counters that had performed strongly in May. Most companies retreated from their recent highs, with the exception of the local banks.

Driven by strong domestic GDP projections, resilient earnings expectations and continued investor confidence in Singapore’s financial sector, DBS, OCBC and UOB continued their upward trajectory and helped push the STI Index to new highs.

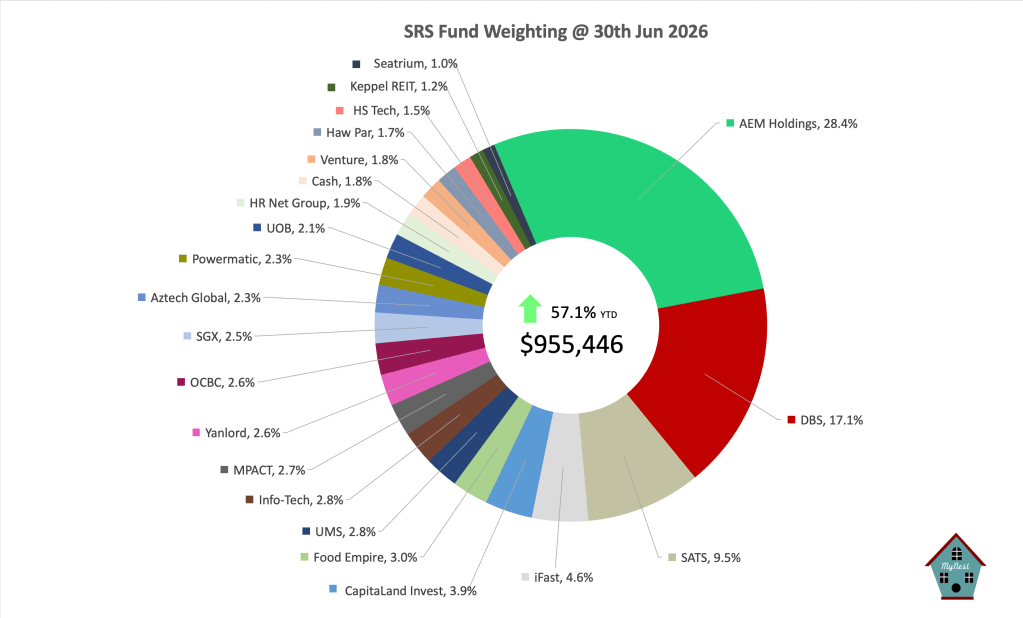

For the SRS Fund, this was helpful because the Finance segment remains a significant part of the portfolio. DBScontinues to be the second-largest individual holding after AEM Holdings, while OCBC, UOB, SGX and iFast also contributed meaningfully to the overall portfolio structure.

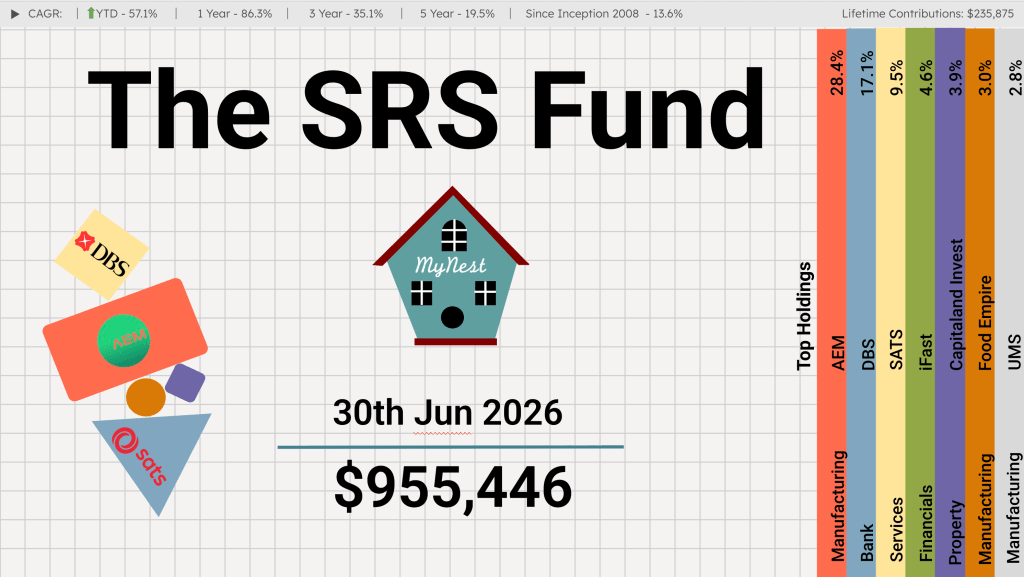

At the same time, the performance of the Fund continues to be strongly influenced by AEM Holdings. While I have already trimmed part of the position and recovered the original capital, AEM remains the Fund’s largest holding at 28.4%.

This concentration has been a major driver of performance, but it also requires continued discipline. A stock can become less risky after the thesis is proven, but more risky if the position size becomes too large relative to the portfolio.

SRS Fund Performance vs. Benchmark

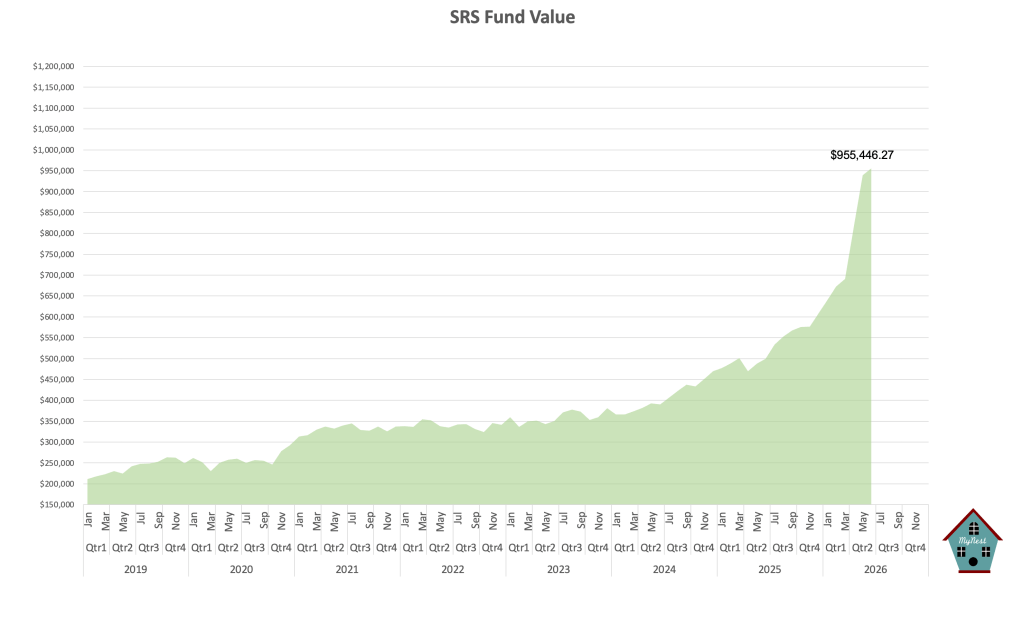

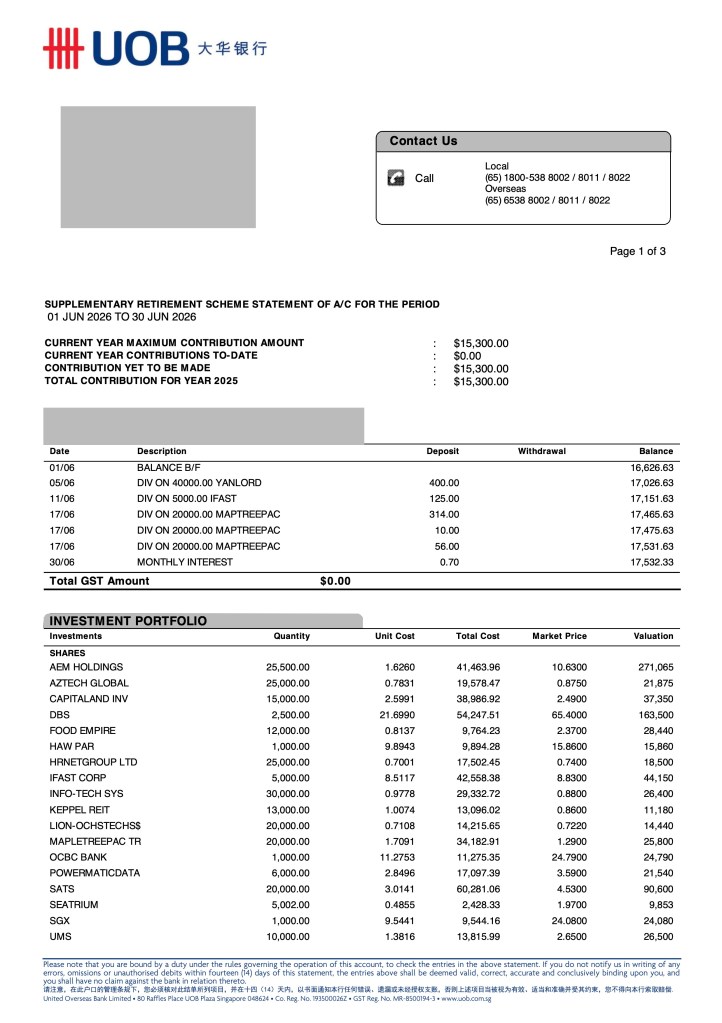

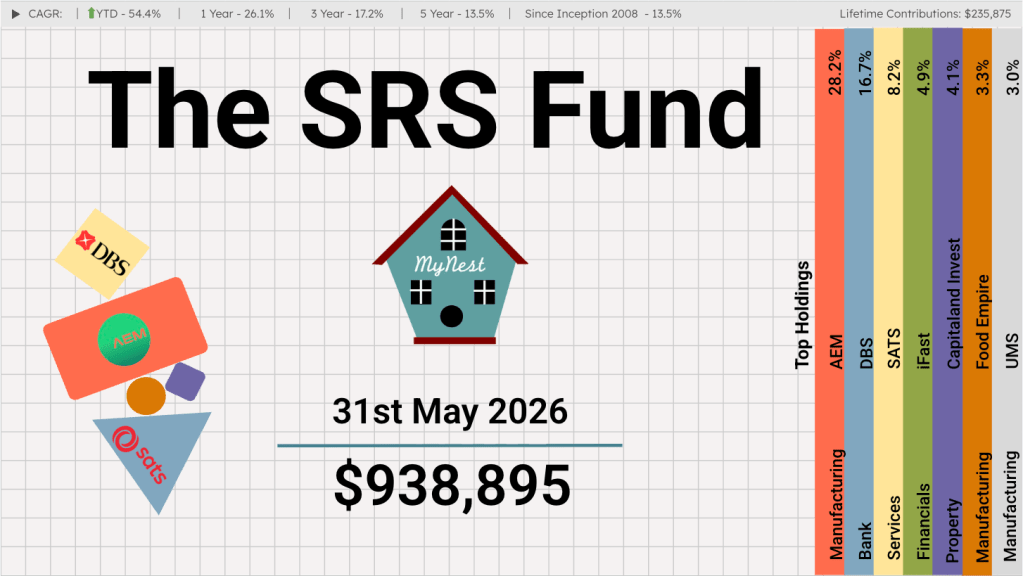

As at 30th Jun 2026, the SRS Fund value stood at $955,446.27, up 57.1% year-to-date.

This is a new high for the SRS Fund and brings the portfolio closer to the $1 million mark. The Fund has now compounded at 13.6% since inception in 2008, with lifetime contributions of $235,875.

The recent outperformance remains largely driven by AEM Holdings and the broader recovery in Singapore-listed manufacturing names. However, the strong performance from local banks also provided support, helping to balance the portfolio between growth-oriented manufacturing exposure and stable financial compounders.

Performance Comparison

| Metric | The SRS Fund | STI Index (Benchmark) |

| YTD Return (Apr 2026) | +57.1% | ~+10.8% |

| Cash Weighting | 1.8% | N/A |

| Top Holding | AEM Holdings (28.4%) | DBS (~27.8%) |

The strong YTD performance is pleasing, but I remain mindful that returns of this magnitude are unusual. Markets do not move in straight lines, and a portfolio that rises quickly can also experience sharp corrections.

The aim is not to extrapolate recent gains blindly, but to continue managing the portfolio with patience, humility and risk awareness.

Portfolio Segments

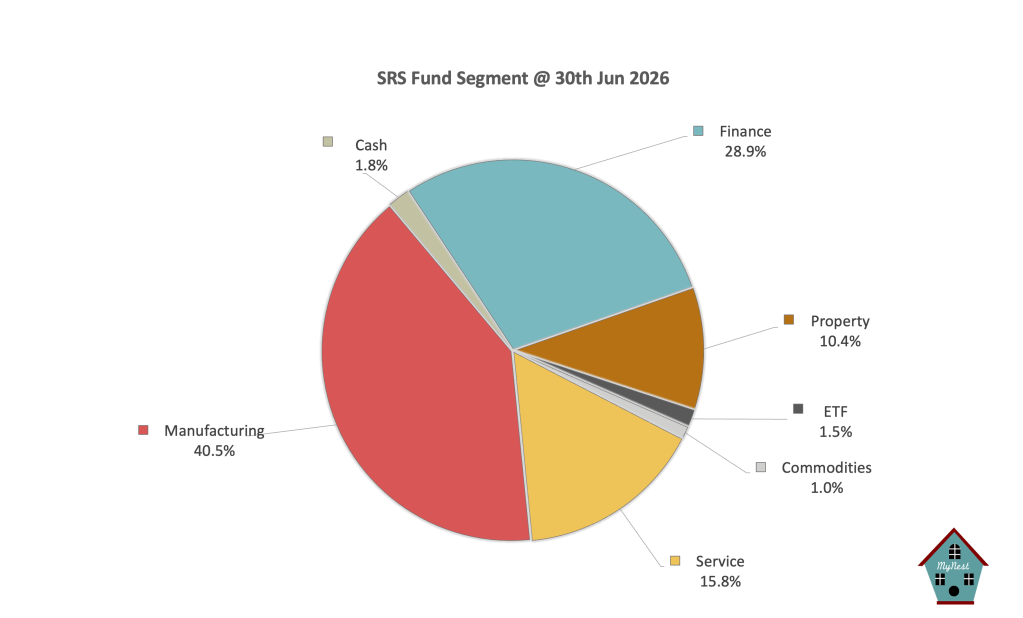

As at 30th June 2026, the SRS Fund remains heavily invested across a few core segments.

Manufacturing is now the largest segment, accounting for 40.5% of the Fund. This is mainly driven by AEM Holdings, together with other manufacturing-related holdings such as UMS, Food Empire, Venture, Aztech Global and Powermatic. The manufacturing exposure has clearly been the key engine of performance in 2026.

Finance remains the second-largest segment at 28.9%. This includes DBS, OCBC, UOB, SGX and iFast. The banks have continued to demonstrate why they remain such important long-term compounders in the Singapore market.

They may not provide the excitement of AI-related manufacturing names, but their earnings quality, dividends and dominant domestic franchises provide a strong foundation for the Fund.

The Service segment accounts for 15.8%, led mainly by SATS and HR Net Group. SATS remains the most important company within this segment. Its WFS acquisition has changed the nature of the business, and I believe the market is still in the process of understanding what SATS can become as a global aviation and cargo services platform.

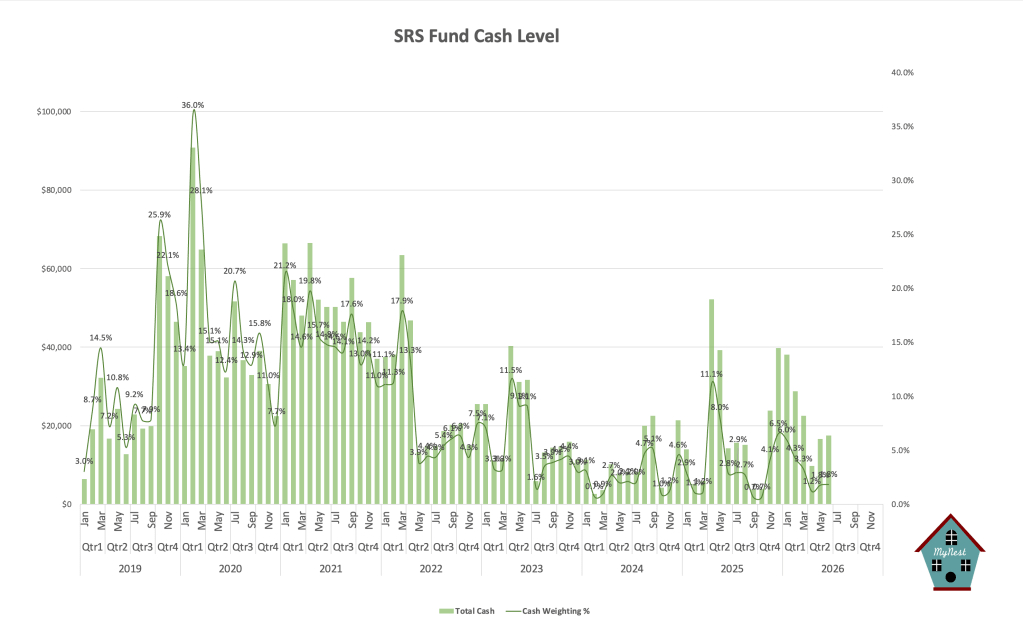

Property-related holdings make up 10.4% of the Fund, while ETF, Commodities and Cash together remain small. Cash stands at only 1.8%, which means the Fund is almost fully invested.

Dividends:

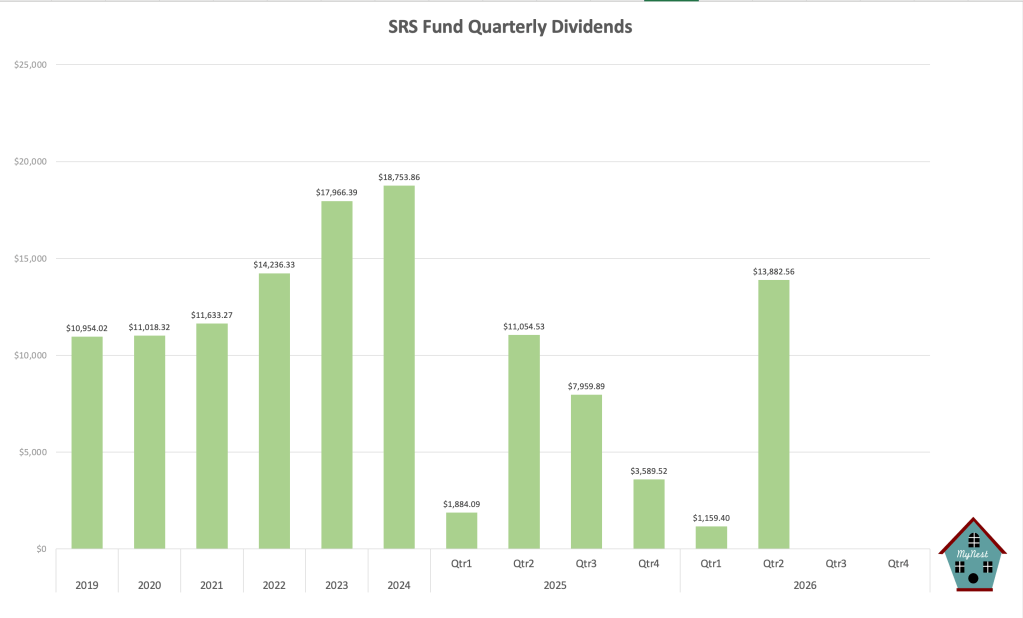

On the income side, dividends continue to provide a steady foundation for the SRS Fund.

The Fund received $13,882.56 in dividends for Q2 2026, following $1,159.40 in Q1. This brings the first-half dividend collection to $15,041.96.

While the SRS Fund is not managed purely as an income portfolio, dividends remain psychologically important. They remind me that behind every stock price is a real business producing cash flows and returning part of those cash flows to shareholders.

The dividend trend over the years has also been encouraging. Annual dividends have grown from around $10,954 in 2019 to $18,753.86 in 2024. Although 2025 was uneven due to portfolio changes and rebalancing, 2026 is shaping up to be a stronger year for income generation.

SRS Fund Value

The SRS Fund value reached $955,446.27 as at 30th June 2026, bringing the Fund to another new high and closer to the $1 million milestone. From just above $200k in 2019, the growth of the Fund shows the quiet power of long-term compounding, supported by patience, reinvested dividends and staying invested through difficult periods.

Cash Levels

Cash remained low at 1.8% as at 30th Jun 2026, reflecting the Fund’s almost fully invested position. This has helped performance during the current rally, especially as key holdings such as AEM, DBS and SATS continued to contribute positively.

However, the low cash level also means the Fund has limited dry powder if market volatility returns. While I am comfortable staying invested in the current holdings, I will remain disciplined and avoid being forced into emotional decisions should the market experience a sharp pullback.

Closing Thoughts

June was a month where uncertainty eased, but discipline remained necessary. The easing of geopolitical tension helped remove one major overhang, while the continued strength in AEM, DBS and SATS pushed the SRS Fund to a new high of $955,446.27. The strong first-half performance is encouraging, but I remain mindful that returns of this nature are unusual and should not lead to complacency.

The journey towards the $1 million milestone is meaningful, but the more important objective remains unchanged — to compound capital patiently and sensibly over the long term. I will continue to focus on managing position size, valuation risk and emotional discipline, while allowing good businesses to grow and compound within the Fund.

-

The SRS Fund Jun 2026

The month of Jun provided an important milestone in the Iran conflict. The agreement between the United States and Iran marked a significant step towards reducing geopolitical tension and reopening a clearer path for global energy flows

-

MyNest US Fund Jun 26

June was another remarkable month in the evolution of the global capitalism and the artificial intelligence investment cycle.

-

The SRS Fund May 2026

Korea, powered by the worldwide shortage and surge in memory demand, was hit directly by the AI wave, with its stock market more than doubling in a matter of 5 months. Taiwan, already the world’s most important advanced chip manufacturing hub has risen to become one of the largest stock market globally.

-

MyNest US Fund May 26

May has been an incredibly illuminating month for the MyNest US Fund. Looking across the broader landscape, the S&P 500 Index has continued its steady leg up, gaining +5.15% in the month of May alone to push its Year-to-Date (YTD) gain to +10.73%.

-

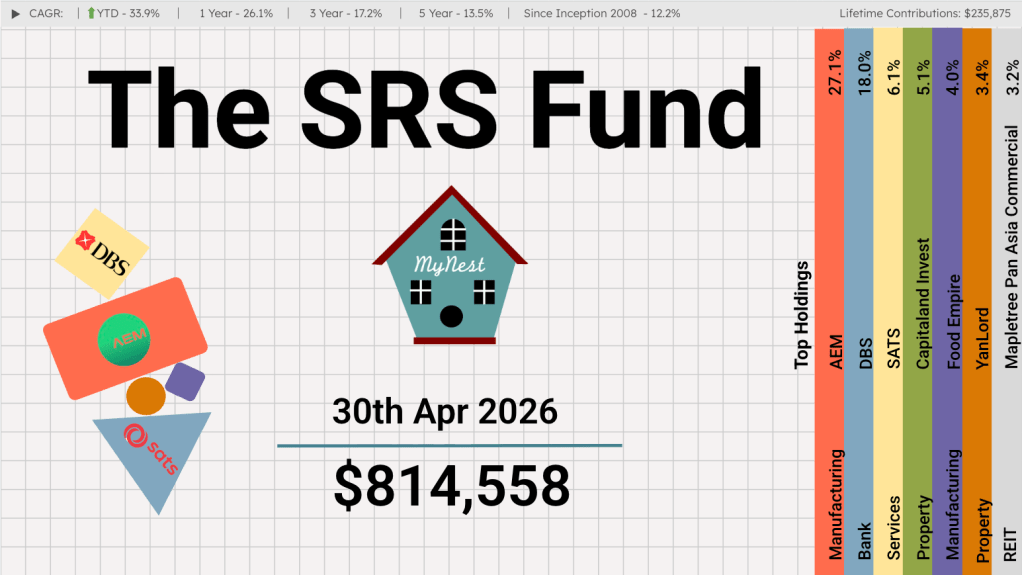

The SRS Fund Apr 2026

In my investment journey, there have been three occasions where I witnessed a company deliver a 10x return.

-

MyNest US Fund Apr 26

The market rebounded strongly in April as investors appeared to look past geopolitical uncertainty and renewed their focus on earnings, artificial intelligence, and the long-term growth prospects of quality businesses.