Long-time investors who are familiar with this company that produces our beloved Tiger Balm oil. As the world freed itself from Covid 19, the company made a stellar recovery in sales increasing revenue by 39.7% in the 2H of 2023.

Experienced investors would have also known Haw Par has an investment portfolio consisting of shares in UOB and UOL forming an intricate web of holdings by the Wee family in one of Singapore’s largest banks. As of the latest results, UOB shares in Haw Par book are worth $2.13b and its investment portfolio itself adds up to $2.6b exceeding its current market cap of $2.18b.

While one can interpret that buying this debt-free business at the current price is equivalent to buying the investment portfolio and getting the healthcare business for free, there must be a good reason for its undervaluation to exist in the first place.

It turns out that the company’s revenue consists of 3 major components comprising of the Tiger Balm business, Property Rental income as well as dividend income from the investment portfolio. However, dividends paid to shareholders over the years have been much less than the dividend income it has received.

So why does a debt-free company with more than $700m in cash need to retain so much of its profits when its return on equity is merely 6.3%? I think the market is confused too thus pricing it as such.

While I may have no idea why management would like to keep such a big war chest, I do know that this big amount getting more interest than ever before. Further, the headline figure of 6.3% actually musks the true earning power of the gem in the investment portfolio.

UOB return on equity is likely to exceed 10% on average and much of this is not captured in the financial statements. It would mean the dividend will continue to grow at a 10% rate and its true earnings are actually closer to $350m than the reported figure.

As such investors will be buying the company at a PE ratio of 6.2 times true earnings with a tailwind of the healthcare business picking up further steam. As such I have made an initial investment into the company with the SRS Fund which will be reflected in its latest upcoming Feb Statement.

-

The SRS Fund May 2026

Korea, powered by the worldwide shortage and surge in memory demand, was hit directly by the AI wave, with its stock market more than doubling in a matter of 5 months. Taiwan, already the world’s most important advanced chip manufacturing hub has risen to become one of the largest stock market globally.

-

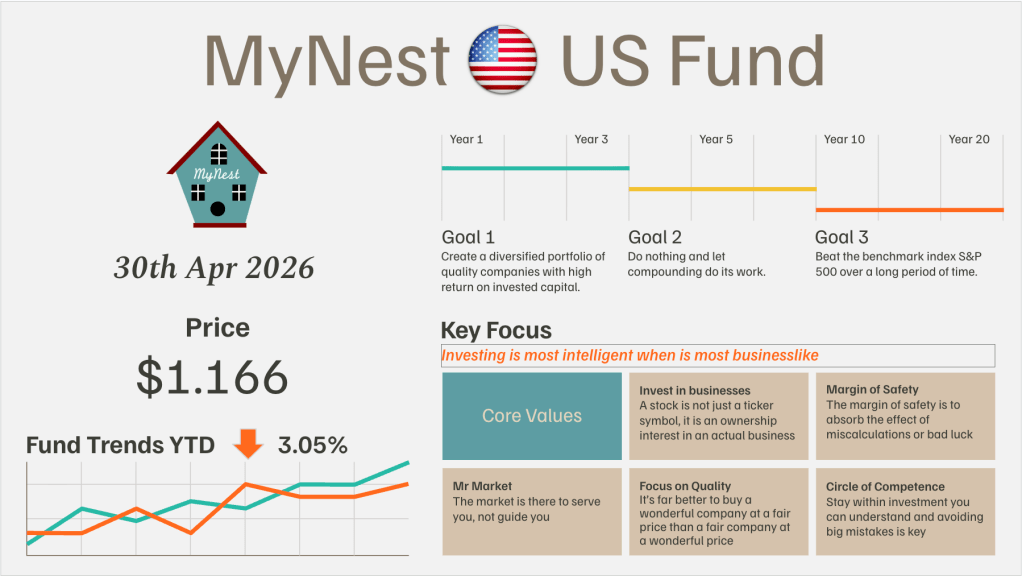

MyNest US Fund May 26

May has been an incredibly illuminating month for the MyNest US Fund. Looking across the broader landscape, the S&P 500 Index has continued its steady leg up, gaining +5.15% in the month of May alone to push its Year-to-Date (YTD) gain to +10.73%.

-

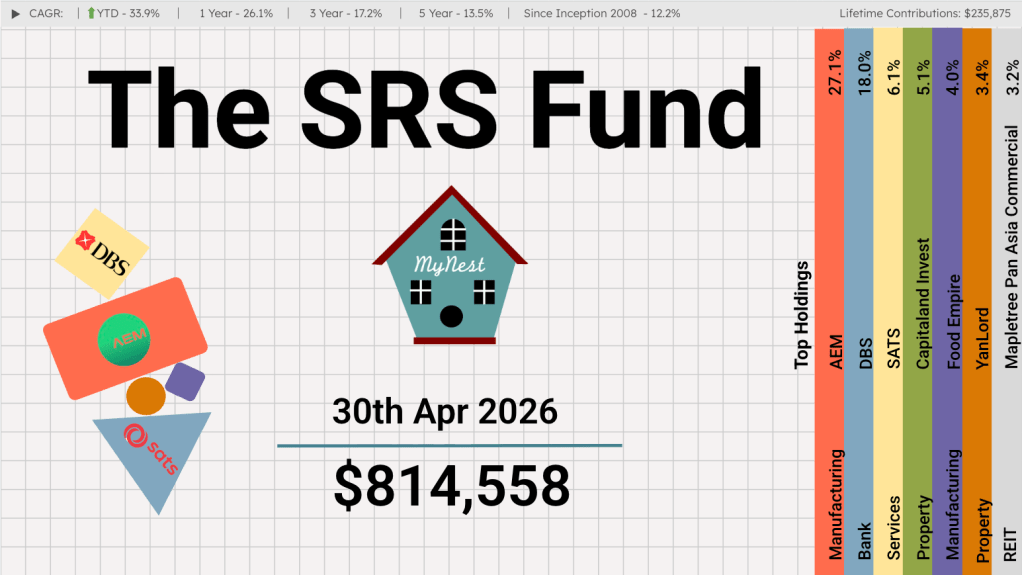

The SRS Fund Apr 2026

In my investment journey, there have been three occasions where I witnessed a company deliver a 10x return.

-

MyNest US Fund Apr 26

The market rebounded strongly in April as investors appeared to look past geopolitical uncertainty and renewed their focus on earnings, artificial intelligence, and the long-term growth prospects of quality businesses.

-

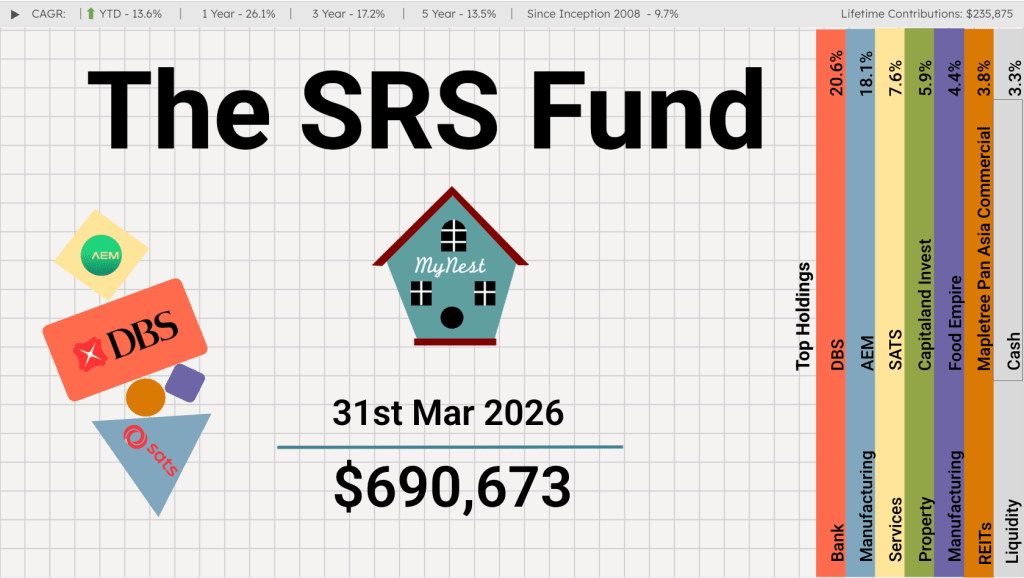

The SRS Fund Mar 2026

It is an enduring market reality that a concentrated minority of holdings drives the vast majority of returns. For years, DBS (currently the largest individual holding at 20.6%) has served as the compounding engine of the SRS Fund.

-

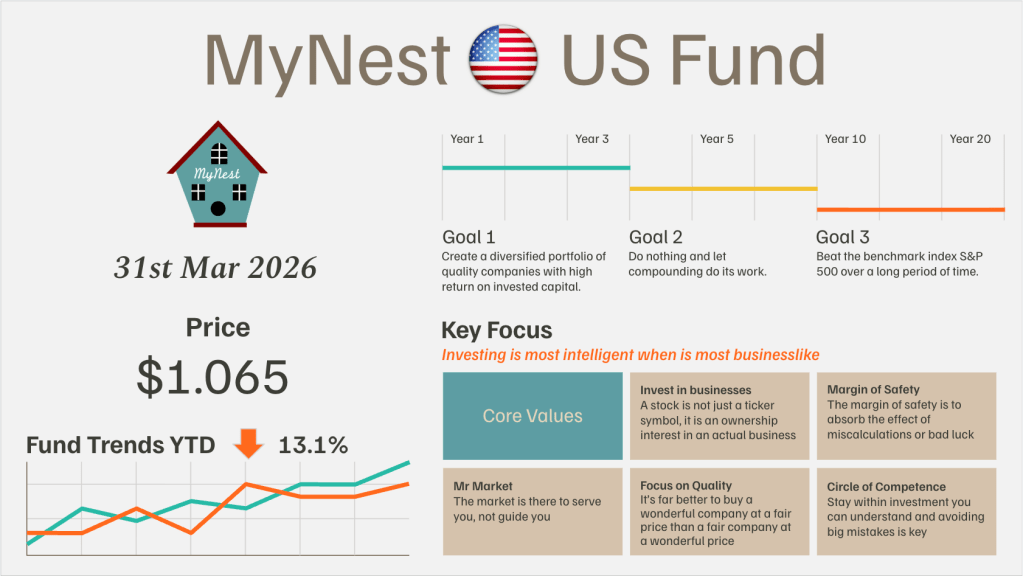

MyNest US Fund Mar 26

March shattered any lingering market complacency, pivoting sharply from the localized damage of the “SaaS-pocalypse” to a systemic shock driven by the war in Iran.

One response to “Haw Par the well know value trap?”

[…] A new addition was made to the SRS Fund in Feb as I invested in Haw Par healthcare business and also UOB indirectly via their investment portfolio. A post written on the investment can be reached at the following link. https://mynest.sg/2024/03/01/haw-par-the-well-know-value-trap/ […]

LikeLike